Potrebbero piacerti anche

- CFASDocumento7 pagineCFASSherica VirayNessuna valutazione finora

- 1st Quiz Intacc5Documento37 pagine1st Quiz Intacc5Mikaela SamonteNessuna valutazione finora

- Cfas Actvity 1-2Documento5 pagineCfas Actvity 1-2Sherica VirayNessuna valutazione finora

- Conceptual Framework (Objective of Financial ReportingDocumento5 pagineConceptual Framework (Objective of Financial ReportingSaeym SegoviaNessuna valutazione finora

- Chapter 2 Conceptual FrameworkDocumento8 pagineChapter 2 Conceptual Frameworkdaniella chynnNessuna valutazione finora

- CFAS 2020 Chapter 1 & 3 and MC ProblemsDocumento6 pagineCFAS 2020 Chapter 1 & 3 and MC Problems4220019Nessuna valutazione finora

- Confram Confram: Accountancy Business (Divine Word University) Accountancy Business (Divine Word University)Documento10 pagineConfram Confram: Accountancy Business (Divine Word University) Accountancy Business (Divine Word University)김유나Nessuna valutazione finora

- (Cpar2016) Far-6182 (Conceptual Framework)Documento3 pagine(Cpar2016) Far-6182 (Conceptual Framework)Irene ArantxaNessuna valutazione finora

- Acc417 - 415 Quiz On Conceptual Framework - Part 1 - AnsweredDocumento6 pagineAcc417 - 415 Quiz On Conceptual Framework - Part 1 - AnsweredJunel Planos100% (2)

- FAR 3MC The Conceptual Framework of Financial ReportingDocumento4 pagineFAR 3MC The Conceptual Framework of Financial ReportingJoy Dhemple LambacoNessuna valutazione finora

- CHAPTER 2 10 PGDocumento10 pagineCHAPTER 2 10 PGgirlyn abadillaNessuna valutazione finora

- Cpa Review School of The Philippines ManilaDocumento6 pagineCpa Review School of The Philippines ManilaKyrie Gwynette OlarveNessuna valutazione finora

- Hand Out#: Far 02 Topic: Revised Conceptual Framework Classification: TheoriesDocumento6 pagineHand Out#: Far 02 Topic: Revised Conceptual Framework Classification: TheoriesJolaica DiocolanoNessuna valutazione finora

- CFAS(!)Documento4 pagineCFAS(!)albertojrmoradoNessuna valutazione finora

- Problem 2-4 Multiple Choice (Ifrs)Documento2 pagineProblem 2-4 Multiple Choice (Ifrs)Jao FloresNessuna valutazione finora

- 6882 - Revised Conceptual FrameworkDocumento6 pagine6882 - Revised Conceptual FrameworkMaximusNessuna valutazione finora

- 00_FAR-Conceptual_FrameworkDocumento10 pagine00_FAR-Conceptual_Frameworkagaceram9090Nessuna valutazione finora

- SM ConceptualFrameworkDocumento4 pagineSM ConceptualFrameworkKISSEY ESTRELLANessuna valutazione finora

- Quiz 1 - Lesson 1Documento2 pagineQuiz 1 - Lesson 1lou-924Nessuna valutazione finora

- Arguments for and against global accounting standardsDocumento5 pagineArguments for and against global accounting standardsNam PhamNessuna valutazione finora

- I - Accounting and Accountancy ProfessionDocumento31 pagineI - Accounting and Accountancy ProfessionAnjell ReyesNessuna valutazione finora

- Quiz 1: Basic ConsiderationsDocumento4 pagineQuiz 1: Basic ConsiderationsMarriah Izzabelle Suarez RamadaNessuna valutazione finora

- FAR 3MC The Conceptual Framework of Financial ReportingDocumento4 pagineFAR 3MC The Conceptual Framework of Financial ReportingHassanhor Guro Bacolod100% (1)

- CPA REVIEW CONCEPTUAL FRAMEWORKDocumento5 pagineCPA REVIEW CONCEPTUAL FRAMEWORKAlliah Mae ArbastoNessuna valutazione finora

- 11-ACC - Theory BaseDocumento3 pagine11-ACC - Theory BaseNaman TiwariNessuna valutazione finora

- Acco 20063 Midterm ExamDocumento7 pagineAcco 20063 Midterm Examyugyeom rojasNessuna valutazione finora

- Toa 1Documento9 pagineToa 1Earl Russell S PaulicanNessuna valutazione finora

- TQ in FARDocumento5 pagineTQ in FARChristine LealNessuna valutazione finora

- 6726 Revised Conceptual FrameworkDocumento7 pagine6726 Revised Conceptual FrameworkJane ValenciaNessuna valutazione finora

- Financial Accounting Standards and the Role of FASBDocumento43 pagineFinancial Accounting Standards and the Role of FASBJodel Paul MartinezNessuna valutazione finora

- Answers Post Test 01 Conceptual Framework 1Documento3 pagineAnswers Post Test 01 Conceptual Framework 1Faith CastroNessuna valutazione finora

- Cpa Review School of The Philippines ManilaDocumento6 pagineCpa Review School of The Philippines ManilaJulius Lester AbieraNessuna valutazione finora

- 6802-Revised-Conceptual-Framework-3-1Documento6 pagine6802-Revised-Conceptual-Framework-3-1axel BNessuna valutazione finora

- Cost MCQDocumento74 pagineCost MCQSimple Abc100% (1)

- Managerial Advisory ServicesOverviewwoanswersDocumento3 pagineManagerial Advisory ServicesOverviewwoanswersJhuneth DominguezNessuna valutazione finora

- DLSU REVDEVT - TOA Revised Reviewer - Answer Key PDFDocumento16 pagineDLSU REVDEVT - TOA Revised Reviewer - Answer Key PDFabbyNessuna valutazione finora

- 01 Acctg 321 A&B Mock Test-1Documento26 pagine01 Acctg 321 A&B Mock Test-1Drayce FerranNessuna valutazione finora

- Accounting overview and key conceptsDocumento7 pagineAccounting overview and key conceptsRomylen De GuzmanNessuna valutazione finora

- Accounting overview and key conceptsDocumento7 pagineAccounting overview and key conceptsRomylen De GuzmanNessuna valutazione finora

- Standard, The Conceptual Framework Overrides That StandardDocumento6 pagineStandard, The Conceptual Framework Overrides That StandardwivadaNessuna valutazione finora

- Practical 1 Compilation of MCDocumento73 paginePractical 1 Compilation of MCTony MorganNessuna valutazione finora

- First ExamDocumento7 pagineFirst ExamAlyana DubloisNessuna valutazione finora

- Review Materials W AnswerDocumento5 pagineReview Materials W Answercute meNessuna valutazione finora

- At - Prelim Rev (875 MCQS) Red Sirug Page 1 of 85Documento85 pagineAt - Prelim Rev (875 MCQS) Red Sirug Page 1 of 85Waleed MustafaNessuna valutazione finora

- AT Answer Key-CombinedDocumento11 pagineAT Answer Key-CombinedA PNessuna valutazione finora

- Aud TheoDocumento4 pagineAud TheoSUBA, Michagail D.Nessuna valutazione finora

- Auditing Theory AuditDocumento77 pagineAuditing Theory AuditAdam Smith0% (1)

- 1st Year QuestionnairesDocumento6 pagine1st Year Questionnaireswivada100% (1)

- MidtermDocumento9 pagineMidtermSohfia Jesse VergaraNessuna valutazione finora

- Conceptual Framework and Accounting Standards Quiz 1Documento8 pagineConceptual Framework and Accounting Standards Quiz 1Andrei GoNessuna valutazione finora

- FAR LT1 Answer KeyDocumento5 pagineFAR LT1 Answer KeypehikNessuna valutazione finora

- MAS ADVISORY SERVICES GUIDEDocumento3 pagineMAS ADVISORY SERVICES GUIDEchowchow123Nessuna valutazione finora

- ch02 TB RankinDocumento7 paginech02 TB RankinSyed Bilal AliNessuna valutazione finora

- CFAS Quiz ADocumento5 pagineCFAS Quiz ADesiree Angelique RebonquinNessuna valutazione finora

- Quiz-Review CfasDocumento5 pagineQuiz-Review CfasMa Louise Ivy RosalesNessuna valutazione finora

- Conceptual Framework: Financial Accounting and ReportingDocumento4 pagineConceptual Framework: Financial Accounting and ReportingDUDUNG dudongNessuna valutazione finora

- Strategic Cost Multiple ChoiceDocumento7 pagineStrategic Cost Multiple ChoiceChristian ZanoriaNessuna valutazione finora

- TRUE-FALSE-Conceptual: CFAS SET 2 and 3 Reviewer Mark Angelo Enriquez, CPADocumento7 pagineTRUE-FALSE-Conceptual: CFAS SET 2 and 3 Reviewer Mark Angelo Enriquez, CPARamsys Attaban100% (1)

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiDa EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNessuna valutazione finora

- IMC, The Next Generation: Five Steps for Delivering Value and Measuring Returns Using Marketing CommunicationDa EverandIMC, The Next Generation: Five Steps for Delivering Value and Measuring Returns Using Marketing CommunicationValutazione: 4.5 su 5 stelle4.5/5 (4)

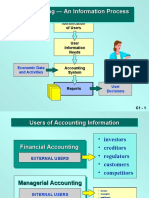

- Accounting - An Information Process Accounting - An Information ProcessDocumento58 pagineAccounting - An Information Process Accounting - An Information ProcessBernadette Cunanan RamosNessuna valutazione finora

- (Amendments To IAS 16 and IAS 41), Which Applies To: Summary of IAS 41 ObjectiveDocumento2 pagine(Amendments To IAS 16 and IAS 41), Which Applies To: Summary of IAS 41 ObjectiveBernadette Cunanan RamosNessuna valutazione finora

- Cash Flow Statement TemplateDocumento5 pagineCash Flow Statement Templatewaqas001Nessuna valutazione finora

- Ias 1Documento7 pagineIas 1Bernadette Cunanan RamosNessuna valutazione finora

- IFRS 9 RECOGNITION AND MEASUREMENT OF FINANCIAL INSTRUMENTSDocumento12 pagineIFRS 9 RECOGNITION AND MEASUREMENT OF FINANCIAL INSTRUMENTSBernadette Cunanan RamosNessuna valutazione finora

- Financial Reporting in The Mining Industry PDFDocumento192 pagineFinancial Reporting in The Mining Industry PDFISRAEL TOLANONessuna valutazione finora

- Business ValuesDocumento51 pagineBusiness ValuesLois Palero AbulNessuna valutazione finora

- Stuart Matthews ResumeDocumento6 pagineStuart Matthews Resumeapi-231151364Nessuna valutazione finora

- IFRS For Small and Medium-Sized Entities (IFRS PDFDocumento34 pagineIFRS For Small and Medium-Sized Entities (IFRS PDFAhmed HussainNessuna valutazione finora

- Statement of Cash FlowsDocumento11 pagineStatement of Cash FlowsBri CorpuzNessuna valutazione finora

- Session11 - Bond Analysis Structure and ContentsDocumento18 pagineSession11 - Bond Analysis Structure and ContentsJoe Garcia100% (1)

- PPP Pub Nga-Guidebook 2018decDocumento72 paginePPP Pub Nga-Guidebook 2018decliboaninoNessuna valutazione finora

- Employer Branding at TcsDocumento10 pagineEmployer Branding at Tcsagrawalrohit_228384100% (3)

- DELL Computer CorporationDocumento8 pagineDELL Computer CorporationCrystal100% (1)

- Economic Order Quantity EOQDocumento8 pagineEconomic Order Quantity EOQAngelo CruzNessuna valutazione finora

- Job Description Grant CoordinatorDocumento2 pagineJob Description Grant Coordinatorapi-134134588Nessuna valutazione finora

- Chapter 8 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Documento47 pagineChapter 8 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarNessuna valutazione finora

- Macroeconomics 10th Edition Parkin Test BankDocumento23 pagineMacroeconomics 10th Edition Parkin Test Banklouisbeatrixzk9u100% (30)

- Social Media Marketing Case Study: Bajaj Allianz Child PlanDocumento28 pagineSocial Media Marketing Case Study: Bajaj Allianz Child PlanDheeraj SinglaNessuna valutazione finora

- Labor Law Review Midterms Exam Dean PoquizDocumento3 pagineLabor Law Review Midterms Exam Dean PoquizAtty. Kristina de VeraNessuna valutazione finora

- List of Valid CertificationsDocumento14 pagineList of Valid CertificationskaramananNessuna valutazione finora

- How Accounting Works: Key TakeawaysDocumento3 pagineHow Accounting Works: Key TakeawaysKendrew SujideNessuna valutazione finora

- Nabard PDFDocumento302 pagineNabard PDFnagaraj_nNessuna valutazione finora

- Bank Officer Resume SampleDocumento8 pagineBank Officer Resume Sampleafdlxeqbk100% (1)

- Auditing in CIS Environment - Topic 1 - Developing and Implementing A Risk-Based IT Audit StrategyDocumento35 pagineAuditing in CIS Environment - Topic 1 - Developing and Implementing A Risk-Based IT Audit StrategyLuisitoNessuna valutazione finora

- Cindy and Jack Have Always Practiced Good Financial Habits inDocumento1 paginaCindy and Jack Have Always Practiced Good Financial Habits inAmit PandeyNessuna valutazione finora

- Accounting, Anatomy, Anthropology and Archaeology paper codesDocumento288 pagineAccounting, Anatomy, Anthropology and Archaeology paper codesmanesh1740% (1)

- Bajaj DistributionDocumento10 pagineBajaj Distributionparulgupta05100% (1)

- Job Description Tower LeadDocumento3 pagineJob Description Tower Leadpune1faultsNessuna valutazione finora

- MCS - May 19 - StructuringDocumento17 pagineMCS - May 19 - StructuringsangNessuna valutazione finora

- Revision5 Variance2Documento4 pagineRevision5 Variance2adamNessuna valutazione finora

- PDF Masa Amended PPP Moa Lgu Malapatan MTCDC 101723 Word 2Documento14 paginePDF Masa Amended PPP Moa Lgu Malapatan MTCDC 101723 Word 2dexterbautistadecember161985Nessuna valutazione finora

- Customer SatisfactionDocumento4 pagineCustomer SatisfactionrolandNessuna valutazione finora

- Impact of Venture Capital On Indian EconomyDocumento5 pagineImpact of Venture Capital On Indian EconomylenovoNessuna valutazione finora

- Online E-commerce Platform Proposal for TeztagDocumento24 pagineOnline E-commerce Platform Proposal for TeztagMohammed NizamNessuna valutazione finora