Potrebbero piacerti anche

- Company Purchase:: Business Organization Goods ServicesDocumento14 pagineCompany Purchase:: Business Organization Goods ServicesNoman KhanNessuna valutazione finora

- Purchase ManagementDocumento32 paginePurchase ManagementManjula Ashok100% (1)

- PurchasingmanagementDocumento20 paginePurchasingmanagementlalitha kandikaNessuna valutazione finora

- Purchase ManagementDocumento34 paginePurchase Managementshweta_4666475% (8)

- Men - Machines - Methods - Money - MaterialsDocumento42 pagineMen - Machines - Methods - Money - MaterialsAbhirup MukherjeeNessuna valutazione finora

- WPPDC-QMD-001-Material Control and Werehousing ProcedureDocumento5 pagineWPPDC-QMD-001-Material Control and Werehousing ProcedureSimbu ArasanNessuna valutazione finora

- Stores ManagementDocumento28 pagineStores ManagementDilip YadavNessuna valutazione finora

- Warehouse SupervisorDocumento2 pagineWarehouse SupervisorJethro Stanly100% (1)

- ProcurementDocumento99 pagineProcurementMoiez AliNessuna valutazione finora

- Procurement ProcedureDocumento10 pagineProcurement ProcedureAshraf ELsherbeney100% (3)

- Documents Used in Purchase and Stores ProcedureDocumento2 pagineDocuments Used in Purchase and Stores Procedurelayyah201388% (8)

- Procedure For ProcurementDocumento9 pagineProcedure For ProcurementTrust EmmaNessuna valutazione finora

- Purchasing, Receipt & Inspection of MaterialDocumento11 paginePurchasing, Receipt & Inspection of MaterialDr. Rakshit SolankiNessuna valutazione finora

- Warehouse Procedure of Project ConsumablesDocumento28 pagineWarehouse Procedure of Project ConsumablesAlmario Sagun100% (4)

- Induction TrainingDocumento6 pagineInduction Trainingsowmiya245Nessuna valutazione finora

- Purchasing ManagementDocumento21 paginePurchasing ManagementJiju Justin100% (3)

- SopDocumento12 pagineSopKamran NaqviNessuna valutazione finora

- Material ManagementDocumento30 pagineMaterial Managementmaulikpanchal100% (1)

- Material Management & ControlDocumento146 pagineMaterial Management & Controlmatrixworld20Nessuna valutazione finora

- Purchasing and Materials Management PDFDocumento210 paginePurchasing and Materials Management PDFShueab Mujawar100% (1)

- Contingency Plan RDocumento6 pagineContingency Plan RtrikjohNessuna valutazione finora

- Stock Keeping and Annual Stock VerificationDocumento3 pagineStock Keeping and Annual Stock VerificationSharnbasappa WaleNessuna valutazione finora

- Purpose: Prepared By: - Mustafa Khan & Co. Controlled By:-Effective DateDocumento20 paginePurpose: Prepared By: - Mustafa Khan & Co. Controlled By:-Effective DateUsman TirmiziNessuna valutazione finora

- Procedure For StoresDocumento25 pagineProcedure For StoresSanthosh Kumar Ch100% (5)

- Procurement PolicyDocumento7 pagineProcurement Policytess100% (2)

- Procurement FlowchartDocumento3 pagineProcurement FlowchartAhmed Mustafa AlabadlehNessuna valutazione finora

- Ch12 - WarehousingDocumento20 pagineCh12 - WarehousingSwarnadevi GanesanNessuna valutazione finora

- Purchasing ProcessDocumento54 paginePurchasing Processraks_mechnadNessuna valutazione finora

- Inventory PDFDocumento7 pagineInventory PDFJose De CuentasNessuna valutazione finora

- Equipment Training Policy and ProcedureDocumento13 pagineEquipment Training Policy and Proceduremonir61100% (1)

- Flow Chart For Store ActivityDocumento1 paginaFlow Chart For Store ActivitySachin KumbharNessuna valutazione finora

- SOP Material ManagementDocumento7 pagineSOP Material Managementwasee99Nessuna valutazione finora

- Material Logistics PlanDocumento21 pagineMaterial Logistics PlanMoniksssNessuna valutazione finora

- Pre-Qualification Form FinalDocumento20 paginePre-Qualification Form FinalImran Qadir100% (2)

- Purchasing & Material Management 1Documento103 paginePurchasing & Material Management 1khndlwlNessuna valutazione finora

- SOP of IndentingDocumento2 pagineSOP of Indentinganoushia alvi0% (1)

- SOP 05 (Procurement)Documento12 pagineSOP 05 (Procurement)Farhan100% (1)

- Inventory ControlDocumento25 pagineInventory ControlSuja Pillai100% (1)

- Fulltext01 PDFDocumento121 pagineFulltext01 PDFVikas SuryawanshiNessuna valutazione finora

- Procurement Management: Presented By: - Muhammad Anas - Hammad Ahmad - Akif AbrarDocumento21 pagineProcurement Management: Presented By: - Muhammad Anas - Hammad Ahmad - Akif AbrarAnas Jameel0% (1)

- Stocks - Physical Verification Guidance NoteDocumento2 pagineStocks - Physical Verification Guidance NoteJoão Henrique Machado100% (1)

- 5.45 Inventory Management ProcedureDocumento4 pagine5.45 Inventory Management ProcedureRhozeiah LeiahNessuna valutazione finora

- SOP - Purchase DeptDocumento42 pagineSOP - Purchase DeptJayant Kumar Jha100% (2)

- Material ManagementDocumento39 pagineMaterial ManagementkkkktNessuna valutazione finora

- Routing - PPT by Gopal K. DixitDocumento38 pagineRouting - PPT by Gopal K. DixitkaashniNessuna valutazione finora

- QMS Inspection ProcedureDocumento5 pagineQMS Inspection ProcedureSang Hà100% (1)

- Shipping ProcedureDocumento3 pagineShipping ProcedurematrixmazeNessuna valutazione finora

- Flow Chart For General PurchasingDocumento1 paginaFlow Chart For General PurchasingSachin KumbharNessuna valutazione finora

- Procurement ManualDocumento14 pagineProcurement ManualHussein Taofeek OlalekanNessuna valutazione finora

- Purchase Policy and Procedure by Puruhutjit SurjitDocumento2 paginePurchase Policy and Procedure by Puruhutjit SurjitSurjit PuruhutjitNessuna valutazione finora

- Material ManagementDocumento20 pagineMaterial Managementgkataria110100% (1)

- Stock Management PolicyDocumento7 pagineStock Management PolicySatish Pareek100% (1)

- QAP-07 Material Control Procedure PDFDocumento22 pagineQAP-07 Material Control Procedure PDFnaseema1100% (9)

- Faculty: Intro: Author S. A. ChunawallaDocumento30 pagineFaculty: Intro: Author S. A. Chunawallaswapnilharal100% (1)

- Managing Products and Services OperationsDocumento11 pagineManaging Products and Services OperationsAnne PecadizoNessuna valutazione finora

- PPM FinalDocumento49 paginePPM FinalTadele DandenaNessuna valutazione finora

- Новый документ в форматеDocumento8 pagineНовый документ в форматеКристи АбдушаNessuna valutazione finora

- UNIT-2 (Control On Purchased Product)Documento12 pagineUNIT-2 (Control On Purchased Product)monishasingh088Nessuna valutazione finora

- Supply Chain Management ConceptsDocumento6 pagineSupply Chain Management ConceptsKelvin MutetiNessuna valutazione finora

- Types of Purchases in A Purchasing ProcessDocumento3 pagineTypes of Purchases in A Purchasing ProcessJonnah Fernandez Dalogdog100% (1)

- 2 Copies PDFDocumento2 pagine2 Copies PDFNitesh BhuraNessuna valutazione finora

- A Project Report On "Project Topic" Name Abhishek Rath Class:-Xii Roll No.: - ACADEMIC SESSION: - 2015-2016Documento12 pagineA Project Report On "Project Topic" Name Abhishek Rath Class:-Xii Roll No.: - ACADEMIC SESSION: - 2015-2016Nitesh BhuraNessuna valutazione finora

- 2 CopiesDocumento2 pagine2 CopiesNitesh BhuraNessuna valutazione finora

- A Project ReportDocumento14 pagineA Project ReportNitesh BhuraNessuna valutazione finora

- Excel 2 PDFDocumento1 paginaExcel 2 PDFNitesh BhuraNessuna valutazione finora

- Sakshi Mishra Library Management SystemDocumento62 pagineSakshi Mishra Library Management SystemNitesh BhuraNessuna valutazione finora

- A Project Report On "Tic Tac Toe Game"Documento13 pagineA Project Report On "Tic Tac Toe Game"Nitesh BhuraNessuna valutazione finora

- A Project Report On "Tic Tac Toe Game" Name:-Shivangi Sahu Class: - Xii C' Roll No.: - ACADEMIC SESSION: - 2016-2017Documento14 pagineA Project Report On "Tic Tac Toe Game" Name:-Shivangi Sahu Class: - Xii C' Roll No.: - ACADEMIC SESSION: - 2016-2017Nitesh BhuraNessuna valutazione finora

- A Project Report On "Tic Tac Toe Game" Name:-Sanjana Jha Class: - Xii C' Roll No.: - ACADEMIC SESSION: - 2016-2017Documento14 pagineA Project Report On "Tic Tac Toe Game" Name:-Sanjana Jha Class: - Xii C' Roll No.: - ACADEMIC SESSION: - 2016-2017Nitesh BhuraNessuna valutazione finora

- Library Management System - RudrahariDocumento62 pagineLibrary Management System - RudrahariNitesh Bhura100% (4)

- Body Mass IndexDocumento8 pagineBody Mass IndexNitesh BhuraNessuna valutazione finora

- Adeshwar Nursing Institute Khamhargaon, Jagdalpur: Community Health Nursing Lesson Plan ON Wound DressingDocumento8 pagineAdeshwar Nursing Institute Khamhargaon, Jagdalpur: Community Health Nursing Lesson Plan ON Wound DressingNitesh BhuraNessuna valutazione finora

- Nithin U Library Management SystemDocumento62 pagineNithin U Library Management SystemNitesh BhuraNessuna valutazione finora

- A Powerpoin Presentation On CircleDocumento26 pagineA Powerpoin Presentation On CircleNitesh BhuraNessuna valutazione finora

- TubercolosisDocumento8 pagineTubercolosisNitesh Bhura100% (1)

- MalariaDocumento9 pagineMalariaNitesh Bhura100% (5)

- Material ManagementDocumento10 pagineMaterial ManagementNitesh BhuraNessuna valutazione finora

- Cyber Crime PDFDocumento13 pagineCyber Crime PDFNitesh BhuraNessuna valutazione finora

- To Study The Quantity of Casein in Different Samples of Milk.Documento11 pagineTo Study The Quantity of Casein in Different Samples of Milk.Nitesh Bhura100% (3)

- Session 2018-2019 Nirmal Hr. Sec. School, JagdalpurDocumento15 pagineSession 2018-2019 Nirmal Hr. Sec. School, JagdalpurNitesh BhuraNessuna valutazione finora

- Stem Cell - HindiDocumento20 pagineStem Cell - HindiNitesh BhuraNessuna valutazione finora

- Sociological Basis and CurriculumDocumento10 pagineSociological Basis and CurriculumNitesh Bhura100% (1)

- 3 Major Landforms of The Earth SulekhaDocumento10 pagine3 Major Landforms of The Earth SulekhaNitesh BhuraNessuna valutazione finora

- 4 The Vedic AgeDocumento11 pagine4 The Vedic AgeNitesh BhuraNessuna valutazione finora

- 1 Solar SystemDocumento19 pagine1 Solar SystemNitesh BhuraNessuna valutazione finora

- 2 Major DomainsDocumento11 pagine2 Major DomainsNitesh BhuraNessuna valutazione finora

- Billing Generation IssueDocumento4 pagineBilling Generation IssueJasmine ScnNessuna valutazione finora

- Bonifacio Water vs. CIRDocumento13 pagineBonifacio Water vs. CIRAngelo CastilloNessuna valutazione finora

- Project Report: Enrollment No. - 10721 Course - B.E CSE World College of Technology & ManagementDocumento52 pagineProject Report: Enrollment No. - 10721 Course - B.E CSE World College of Technology & ManagementVishant Sharma100% (1)

- Internal Control ChecklistDocumento26 pagineInternal Control ChecklistJade Ballado-TanNessuna valutazione finora

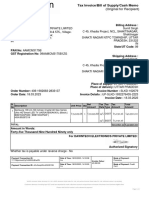

- Tax Invoice: Scan To ReturnDocumento1 paginaTax Invoice: Scan To ReturnMadhurNessuna valutazione finora

- Adm Guidelines Cov 19 LevyDocumento12 pagineAdm Guidelines Cov 19 LevyFuaad DodooNessuna valutazione finora

- DOF-RO Form 91Documento6 pagineDOF-RO Form 91Bobby Olavides SebastianNessuna valutazione finora

- Pharmacy Management SystemDocumento5 paginePharmacy Management SystemRabia ShahzadiNessuna valutazione finora

- CAIIB - 2 BFM MCQs BOOK PDFDocumento172 pagineCAIIB - 2 BFM MCQs BOOK PDFArijit Sahu20% (5)

- Techinfo56 DatadictionaryDocumento264 pagineTechinfo56 DatadictionaryPhanithStar Triple HNessuna valutazione finora

- Flowchart Hotel ReservationDocumento1 paginaFlowchart Hotel ReservationGrace Tacla0% (3)

- 22Z S4hana2020 BPD en UsDocumento153 pagine22Z S4hana2020 BPD en UsMAYANK JAINNessuna valutazione finora

- Sap Customer and Vendor IntegrationDocumento27 pagineSap Customer and Vendor IntegrationmayuraNessuna valutazione finora

- UntitledhshdDocumento1 paginaUntitledhshdSumit SinghNessuna valutazione finora

- 69679716181019595Documento32 pagine69679716181019595logicinsideNessuna valutazione finora

- InvoiceDocumento2 pagineInvoiceFantania BerryNessuna valutazione finora

- Gast Solar Mechanics P.L.C: Performa InvoiceDocumento19 pagineGast Solar Mechanics P.L.C: Performa Invoicekali highNessuna valutazione finora

- Revenue and Expenditure AuditDocumento38 pagineRevenue and Expenditure AuditPavitra MohanNessuna valutazione finora

- A20 BasicDocumento8 pagineA20 BasicAguilan, Alondra JaneNessuna valutazione finora

- Remittance AdviceDocumento30 pagineRemittance AdviceSureshNessuna valutazione finora

- Transportation Module: Business Consulting ServicesDocumento68 pagineTransportation Module: Business Consulting ServicesBettyNessuna valutazione finora

- Purchasing ProcessDocumento15 paginePurchasing Processannedanyle acabadoNessuna valutazione finora

- BlueprinttestDocumento68 pagineBlueprinttestVeera Mani100% (1)

- 2011 Revenue and Cash Receipts Cycle Internal ControlDocumento11 pagine2011 Revenue and Cash Receipts Cycle Internal ControlTheQUICKbrownFOXNessuna valutazione finora

- What Is Cancer? What Causes Cancer?: Signs and Symptoms of Cancer What Are Signs and Symptoms?Documento3 pagineWhat Is Cancer? What Causes Cancer?: Signs and Symptoms of Cancer What Are Signs and Symptoms?Paul Santos NonatNessuna valutazione finora

- Food Regulation BangladeshDocumento22 pagineFood Regulation BangladeshAnonymous ExHdC8Nessuna valutazione finora

- SAP CIN VAT PresentationDocumento13 pagineSAP CIN VAT PresentationSrinivasa KirankumarNessuna valutazione finora

- Prithvi Information Solutions LTD - Invoices Five Customers RecivabelsDocumento10 paginePrithvi Information Solutions LTD - Invoices Five Customers RecivabelsMegan FinleyNessuna valutazione finora

- E-Way Bill SystemDocumento1 paginaE-Way Bill SystemamruthamalleshNessuna valutazione finora

- Bus Order SummaryDocumento3 pagineBus Order Summarykian hongNessuna valutazione finora