Potrebbero piacerti anche

- Anne Aylor Planning Materiality CaseDocumento8 pagineAnne Aylor Planning Materiality CaseJoey Ding100% (6)

- Dane Rudhyar - Lunar NodesDocumento26 pagineDane Rudhyar - Lunar Nodescoser92% (12)

- Blank Horoscope WheelDocumento2 pagineBlank Horoscope WheelKristina Sip100% (1)

- Auditing in Computer Environment System, Chapter 1 by James HallDocumento22 pagineAuditing in Computer Environment System, Chapter 1 by James HallRobert Castillo100% (6)

- Manning Agency AuditDocumento22 pagineManning Agency AuditMichael Potts100% (2)

- Materi - Roni Sadrah - ISO SNI 27037 - Posisi Ahli Forensik Digital - RevisiDocumento23 pagineMateri - Roni Sadrah - ISO SNI 27037 - Posisi Ahli Forensik Digital - RevisiLKPD Pessel 2020100% (1)

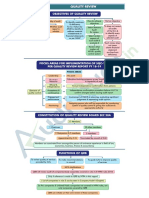

- Objectives of Quality ReviewDocumento6 pagineObjectives of Quality ReviewVijay Kumar KollaNessuna valutazione finora

- Session 4 - QAR Audit Methodology Manual - Pre-Engagement, Planning and Test of ControlsDocumento55 pagineSession 4 - QAR Audit Methodology Manual - Pre-Engagement, Planning and Test of ControlsRheneir Mora100% (1)

- PPE Headquarters - NPPE Sample ChapterDocumento18 paginePPE Headquarters - NPPE Sample ChapterM G83% (6)

- IBC May 19 Arpita MamDocumento58 pagineIBC May 19 Arpita Mamvishnuverma100% (8)

- Standards Full by Prof. Khushboo SanghaviDocumento76 pagineStandards Full by Prof. Khushboo Sanghavivishnuverma100% (4)

- (Gordon Bing) Due Diligence Planning, Questions, (BookFi)Documento220 pagine(Gordon Bing) Due Diligence Planning, Questions, (BookFi)howasa6081100% (1)

- (Sapp) Slide f3 AccaDocumento212 pagine(Sapp) Slide f3 AccaHàn HươngNessuna valutazione finora

- Iso 19011 2018Documento56 pagineIso 19011 2018JoelNessuna valutazione finora

- Internship Report at UNILEC KollamDocumento47 pagineInternship Report at UNILEC KollamSebin Thampi75% (4)

- Auditing: The Ultimate ShotDocumento31 pagineAuditing: The Ultimate ShotManogna P100% (1)

- AuditingDocumento179 pagineAuditingCahyo CyoNessuna valutazione finora

- Analisis Penerapan Digitalisasi Online Arsip (Doa) Pegawai Pada Pengelolaan Tata Naskah Aparatur Sipil Negara Badan Kepegawaian Dan Pengembangan Sumber Daya Manusia (BKPSDM) Kabupaten BoneDocumento8 pagineAnalisis Penerapan Digitalisasi Online Arsip (Doa) Pegawai Pada Pengelolaan Tata Naskah Aparatur Sipil Negara Badan Kepegawaian Dan Pengembangan Sumber Daya Manusia (BKPSDM) Kabupaten Boneramadi ramNessuna valutazione finora

- 2020 Body Worn Camera Evaluation Report: ISC: Protected ADocumento45 pagine2020 Body Worn Camera Evaluation Report: ISC: Protected ACTV CalgaryNessuna valutazione finora

- Audit para Monitoring System (Apms) (A Web Based Portal) For Submission of Atns To Lok Sabha SecretariatDocumento55 pagineAudit para Monitoring System (Apms) (A Web Based Portal) For Submission of Atns To Lok Sabha SecretariatArchna ChughNessuna valutazione finora

- Notes CA Inter Audit CA HimanshuDocumento259 pagineNotes CA Inter Audit CA HimanshuAwesome AngelNessuna valutazione finora

- OrbitStarLite R0126 Cat4 SPEC Standard 20201216 1Documento2 pagineOrbitStarLite R0126 Cat4 SPEC Standard 20201216 1Omline TVNessuna valutazione finora

- Training ISO 27001 TerbaruDocumento3 pagineTraining ISO 27001 TerbaruPanji GunerNessuna valutazione finora

- Documentacion GestioIP 30 enDocumento102 pagineDocumentacion GestioIP 30 enhunterpyNessuna valutazione finora

- Environmental Cost Accounting and AuditingDocumento7 pagineEnvironmental Cost Accounting and AuditingMohd HafizuddinNessuna valutazione finora

- Pre Test Revision QuizDocumento4 paginePre Test Revision QuizAnkur DhirNessuna valutazione finora

- ICDV Evaluation Final ReportDocumento17 pagineICDV Evaluation Final ReportCTV CalgaryNessuna valutazione finora

- The Effect of Emotional Intelligence in The Relationship Between Auditor's Characteristics and Work Pressure On Auditor's Ability To Detect FraudDocumento12 pagineThe Effect of Emotional Intelligence in The Relationship Between Auditor's Characteristics and Work Pressure On Auditor's Ability To Detect FraudInternational Journal of Innovative Science and Research TechnologyNessuna valutazione finora

- Soal SecretarisDocumento13 pagineSoal SecretarisNelliNessuna valutazione finora

- Study CaseDocumento13 pagineStudy CaseMutiara WahyuniNessuna valutazione finora

- Auditing Lecture Slides Introduction.Documento30 pagineAuditing Lecture Slides Introduction.MoniqueNessuna valutazione finora

- Chapter 7 EvidenceDocumento6 pagineChapter 7 Evidencerishi kareliaNessuna valutazione finora

- 2022 Topic 1-4 OverviewDocumento10 pagine2022 Topic 1-4 OverviewIma AdakaNessuna valutazione finora

- Summary of PSADocumento66 pagineSummary of PSAKeno OcampoNessuna valutazione finora

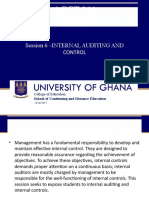

- ACCT 044 Auditing: Session 6 - Internal Auditing and ControlDocumento20 pagineACCT 044 Auditing: Session 6 - Internal Auditing and ControlElikem KokorokoNessuna valutazione finora

- B3 - Audit EvidenceDocumento8 pagineB3 - Audit EvidenceFrank AlexanderNessuna valutazione finora

- Professional Judgment A Key Requirement in The Conduct of An AuditDocumento28 pagineProfessional Judgment A Key Requirement in The Conduct of An AuditsajedulNessuna valutazione finora

- Internal Audit STNDDocumento44 pagineInternal Audit STNDvmmalviyaNessuna valutazione finora

- Accounting and Assurance Principles Notes - Sir PerlasDocumento7 pagineAccounting and Assurance Principles Notes - Sir PerlasScarlet DragonNessuna valutazione finora

- Internal ControlDocumento28 pagineInternal ControlpnsbajinganNessuna valutazione finora

- Apd 3 NotesDocumento6 pagineApd 3 NotesHelios HexNessuna valutazione finora

- Discussion Wit DeanDocumento13 pagineDiscussion Wit DeanMary Elisha PinedaNessuna valutazione finora

- AUA3751 Lecture Slide 05 An CH 5 General Principles of Auditingv2Documento35 pagineAUA3751 Lecture Slide 05 An CH 5 General Principles of Auditingv2MoniqueNessuna valutazione finora

- Summary of Isa For f8Documento64 pagineSummary of Isa For f8Fuad HassanNessuna valutazione finora

- IntCtrlTrngupdate-January 2017-New2 0Documento30 pagineIntCtrlTrngupdate-January 2017-New2 0cooleenjziNessuna valutazione finora

- Lecture 1 (Ii) - Regulatory EnvironmentDocumento25 pagineLecture 1 (Ii) - Regulatory EnvironmentkhooNessuna valutazione finora

- Topic 3 Audit Planning (Slide No.2) - Materiality - Audit RiskDocumento57 pagineTopic 3 Audit Planning (Slide No.2) - Materiality - Audit RiskWAN NUR SYAZANA AHMAD YARANINessuna valutazione finora

- Caf 8 Mi Vol 2Documento204 pagineCaf 8 Mi Vol 2Taha SiddiquiNessuna valutazione finora

- AuditDocumento45 pagineAuditHuzaifa Waseem AwanNessuna valutazione finora

- Notes InformaionSecurityDocumento2 pagineNotes InformaionSecuritySridharan SriNessuna valutazione finora

- The Risk-Based Audit ProcessDocumento16 pagineThe Risk-Based Audit ProcessCarlo manejaNessuna valutazione finora

- Lesson 5 - Audit Planning PDFDocumento4 pagineLesson 5 - Audit Planning PDFAllaina Uy BerbanoNessuna valutazione finora

- COAUA2 - Weeks 1 Class 2 - APA Updated JVDocumento19 pagineCOAUA2 - Weeks 1 Class 2 - APA Updated JVfs5kxrcn2gNessuna valutazione finora

- Job Profile Role and Responsibilties Expected From CandidatesDocumento5 pagineJob Profile Role and Responsibilties Expected From CandidatesRudraksha PatelNessuna valutazione finora

- Chapter-6 Peer ReviewDocumento6 pagineChapter-6 Peer ReviewAyushi BindalNessuna valutazione finora

- Atcae Audit Updates - 1Documento8 pagineAtcae Audit Updates - 1sidthefreak809Nessuna valutazione finora

- CSI Blackbelt in SEATA - Internal Audit Master Class (Malaysia), Featuring Mr. TOMMY SEAHDocumento4 pagineCSI Blackbelt in SEATA - Internal Audit Master Class (Malaysia), Featuring Mr. TOMMY SEAHCFE International Consultancy GroupNessuna valutazione finora

- Lecture 2 - ARM 2022-23Documento54 pagineLecture 2 - ARM 2022-23Francisca PereiraNessuna valutazione finora

- RKPL 2019 - Smart Requirements (Pert. 7) PDFDocumento28 pagineRKPL 2019 - Smart Requirements (Pert. 7) PDFFaza RashifNessuna valutazione finora

- Root Cause Analysis PresentationDocumento37 pagineRoot Cause Analysis PresentationucheonixNessuna valutazione finora

- م9Documento17 pagineم9raed.hamad raed.hamadNessuna valutazione finora

- Audit Evidence An IntroductionDocumento20 pagineAudit Evidence An IntroductionAlissaNessuna valutazione finora

- ISAs For F8 As of December 2013Documento66 pagineISAs For F8 As of December 2013Tolo MassotNessuna valutazione finora

- Purchasing Audit Work ProgramDocumento10 paginePurchasing Audit Work Programmr auditorNessuna valutazione finora

- Risk-Based Auditing - To SendDocumento67 pagineRisk-Based Auditing - To SendThùy GiangNessuna valutazione finora

- Summary NotesDocumento183 pagineSummary Noteschet2019budhaNessuna valutazione finora

- Audit 1 Chapter 2Documento37 pagineAudit 1 Chapter 2Meseret Asefa100% (1)

- Introduction Forensic Audit ReportingDocumento16 pagineIntroduction Forensic Audit ReportingChristen CastilloNessuna valutazione finora

- .archivetempIGC1 Element 5Documento24 pagine.archivetempIGC1 Element 5aqib.aliNessuna valutazione finora

- P7 Summary of ISADocumento76 pagineP7 Summary of ISAAlina Tariq100% (1)

- Smart Investment English (E-Copy)Documento48 pagineSmart Investment English (E-Copy)vishnuvermaNessuna valutazione finora

- Harshad Jaju Vouching For IpccDocumento80 pagineHarshad Jaju Vouching For IpccvishnuvermaNessuna valutazione finora

- Chapter 6 - Company AuditDocumento15 pagineChapter 6 - Company AuditShubham agrawalNessuna valutazione finora

- EIS MRN Inter CADocumento82 pagineEIS MRN Inter CAvishnuvermaNessuna valutazione finora

- Brief History of The Sikh GurusDocumento81 pagineBrief History of The Sikh GurusvishnuvermaNessuna valutazione finora

- Audit Question BankDocumento116 pagineAudit Question Bankhardu rajpalNessuna valutazione finora

- 19 9 2 Bloomberg Businessweek UsDocumento89 pagine19 9 2 Bloomberg Businessweek Usvishnuverma100% (1)

- Bloomberg Business Week AsiaDocumento73 pagineBloomberg Business Week Asiavishnuverma100% (1)

- Accounts & Adv Account BookDocumento308 pagineAccounts & Adv Account Bookvishnuverma100% (1)

- Bloomberg Businessweek UsDocumento73 pagineBloomberg Businessweek UsvishnuvermaNessuna valutazione finora

- CA Ipcc Inter It BookDocumento306 pagineCA Ipcc Inter It BookvishnuvermaNessuna valutazione finora

- Inter SA Compact BookDocumento46 pagineInter SA Compact Bookvishnuverma0% (1)

- CA Final SA Concept by Siddharth AgarwalDocumento54 pagineCA Final SA Concept by Siddharth Agarwalvishnuverma100% (1)

- DT Memory BookDocumento30 pagineDT Memory Bookvishnuverma100% (1)

- CA Inter Audit JKSCDocumento358 pagineCA Inter Audit JKSCvishnuverma50% (2)

- Vol 2. SampleDocumento23 pagineVol 2. SamplevishnuvermaNessuna valutazione finora

- Sbilife Q2fy19 Jbwa 261018Documento7 pagineSbilife Q2fy19 Jbwa 261018vishnuvermaNessuna valutazione finora

- Vol 1. SampleDocumento41 pagineVol 1. SamplevishnuvermaNessuna valutazione finora

- GST Scanner by DG SirDocumento41 pagineGST Scanner by DG SirvishnuvermaNessuna valutazione finora

- Law Board MeetingsDocumento4 pagineLaw Board MeetingsvishnuvermaNessuna valutazione finora

- Ind As ChartsDocumento20 pagineInd As ChartsvishnuvermaNessuna valutazione finora

- SFM Theory BookDocumento33 pagineSFM Theory BookvishnuvermaNessuna valutazione finora

- Law Sebi MCQDocumento6 pagineLaw Sebi MCQvishnuvermaNessuna valutazione finora

- Ind AS: An Overview (Simplified)Documento28 pagineInd AS: An Overview (Simplified)Mehran AvNessuna valutazione finora

- EOI Vol-1 500 Bedded Cardiac Hospital For Arch ConslDocumento23 pagineEOI Vol-1 500 Bedded Cardiac Hospital For Arch ConslAditya SriramNessuna valutazione finora

- Cera 2017Documento93 pagineCera 2017Jupe JonesNessuna valutazione finora

- APC Group Inc. and Subsidiaries - PSE - RedactedDocumento59 pagineAPC Group Inc. and Subsidiaries - PSE - Redacteddawijawof awofnafawNessuna valutazione finora

- Strategic Management For SMEDocumento3 pagineStrategic Management For SMEvernarose bayaNessuna valutazione finora

- Preliminary Discussion Assurance Engagements 5 Elements of Assurance EngagementDocumento3 paginePreliminary Discussion Assurance Engagements 5 Elements of Assurance EngagementChristine NionesNessuna valutazione finora

- How Coso Has Improved Imternal Control in The United StatesDocumento3 pagineHow Coso Has Improved Imternal Control in The United StatesJuni TambunanNessuna valutazione finora

- Account Research Work 2Documento71 pagineAccount Research Work 2Jayeoba Roseline OlawanleNessuna valutazione finora

- 3rd Reminder Letter - Exentrix Network Sdn. Bhd.Documento2 pagine3rd Reminder Letter - Exentrix Network Sdn. Bhd.afifdzia978Nessuna valutazione finora

- Lecture 1 - History and Development of AccountingDocumento58 pagineLecture 1 - History and Development of AccountingIzaac PovanesNessuna valutazione finora

- FM Model Test PaperDocumento59 pagineFM Model Test PaperMOHAMMAD NADEEMNessuna valutazione finora

- Caldera Ivo ResumeDocumento2 pagineCaldera Ivo Resumeapi-308255590Nessuna valutazione finora

- Cce 2Documento2 pagineCce 2Charish Jane Antonio CarreonNessuna valutazione finora

- Ais CH 3Documento49 pagineAis CH 3Dr. Messele GetachewNessuna valutazione finora

- WNS BFS Capabilities Presentation - Jan - 2013Documento30 pagineWNS BFS Capabilities Presentation - Jan - 2013VikasNessuna valutazione finora

- Test 1 15 April 2020 Questions and AnswersDocumento4 pagineTest 1 15 April 2020 Questions and AnswersJona FranciscoNessuna valutazione finora

- RFJPIA10CARAGA1819 IRR RMYC-Academic-League PDFDocumento27 pagineRFJPIA10CARAGA1819 IRR RMYC-Academic-League PDFSiaJLordeNessuna valutazione finora

- Job Pending CutiDocumento2 pagineJob Pending CutiRestiNessuna valutazione finora

- Gaia Iar 2020Documento114 pagineGaia Iar 2020m_edas4262Nessuna valutazione finora

- Introduction To Accounting Data Analytics and Visualization Module 1Documento55 pagineIntroduction To Accounting Data Analytics and Visualization Module 1Tareq AzizNessuna valutazione finora

- MazzellaCatalog13 Services LRDocumento22 pagineMazzellaCatalog13 Services LREricNessuna valutazione finora

- DACAAR FInance Policy11Documento69 pagineDACAAR FInance Policy11abdulhaiahmadzaiNessuna valutazione finora

- Cement Industry SAP PDFDocumento62 pagineCement Industry SAP PDFJaved AhamedNessuna valutazione finora

- Godfrey Phillips India Limited Annual Report 2018 19Documento214 pagineGodfrey Phillips India Limited Annual Report 2018 19sanchit khemkaNessuna valutazione finora

- COSRECI Annual Account 2019Documento21 pagineCOSRECI Annual Account 2019Tony OrtegaNessuna valutazione finora