Potrebbero piacerti anche

- United States Census Figures Back to 1630Da EverandUnited States Census Figures Back to 1630Nessuna valutazione finora

- Econometrics Assignment 3Documento16 pagineEconometrics Assignment 3Palak SharmaNessuna valutazione finora

- Base - Práctica 1Documento19 pagineBase - Práctica 1Josue Cajacuri YarascaNessuna valutazione finora

- BGMEA Trade InformationDocumento5 pagineBGMEA Trade InformationArjan ⎝╰⏝╯⎠ KuntalNessuna valutazione finora

- Tradeinformation: MembershipDocumento11 pagineTradeinformation: Membershipmobarok2613Nessuna valutazione finora

- Data GDP Eco 545Documento56 pagineData GDP Eco 545SITI MADHIHAH OTHMANNessuna valutazione finora

- Finolex Cables LimitedDocumento55 pagineFinolex Cables Limitedshivam vermaNessuna valutazione finora

- Company Name Last Historical Year CurrencyDocumento51 pagineCompany Name Last Historical Year Currencyshivam vermaNessuna valutazione finora

- Indices: Sensex For The Period: From Year 1991 To Year 2008Documento5 pagineIndices: Sensex For The Period: From Year 1991 To Year 2008mak_max11Nessuna valutazione finora

- Table 1: Macro-Economic Aggregates (At Current Prices) Table 1: Macro-Economic Aggregates (At Current Prices) (Contd.)Documento3 pagineTable 1: Macro-Economic Aggregates (At Current Prices) Table 1: Macro-Economic Aggregates (At Current Prices) (Contd.)greyistariNessuna valutazione finora

- Table 104: Major Heads of Developmental and Non-Developmental Expenditure of The Central GovernmentDocumento1 paginaTable 104: Major Heads of Developmental and Non-Developmental Expenditure of The Central GovernmentretrogadeNessuna valutazione finora

- PC Device Sales FinishedDocumento6 paginePC Device Sales FinishedSeemaNessuna valutazione finora

- Table 155: Foreign Investment Inflows: TotalDocumento1 paginaTable 155: Foreign Investment Inflows: TotalSiddharth Singh TomarNessuna valutazione finora

- Company Name Last Historical Year CurrencyDocumento55 pagineCompany Name Last Historical Year Currencyshivam vermaNessuna valutazione finora

- Year Wise ProfileDocumento1 paginaYear Wise ProfilemukeshtodiNessuna valutazione finora

- Assignment On "Trends, Obstacles & Remedies of Foreign Investment"Documento18 pagineAssignment On "Trends, Obstacles & Remedies of Foreign Investment"RonyNessuna valutazione finora

- ACC Ltd.Documento59 pagineACC Ltd.shivam vermaNessuna valutazione finora

- DCF and PirDocumento2 pagineDCF and PirVamsi HashmiNessuna valutazione finora

- FOPE Ass 04Documento2 pagineFOPE Ass 04Vamsi HashmiNessuna valutazione finora

- US - India ToT AnalysisDocumento13 pagineUS - India ToT AnalysisKartik ChopraNessuna valutazione finora

- Price Index PDFDocumento4 paginePrice Index PDFAfif Taufiiqul HakimNessuna valutazione finora

- Self-Help Group-Bank Linkage ProgrammeDocumento1 paginaSelf-Help Group-Bank Linkage ProgrammeKajal ChaudharyNessuna valutazione finora

- White BoardDocumento135 pagineWhite Boardwilsy1978Nessuna valutazione finora

- NMDC AnalysisDocumento59 pagineNMDC Analysisshivani guptaNessuna valutazione finora

- Gni (Usd) : Regression StatisticsDocumento4 pagineGni (Usd) : Regression Statisticstp077535Nessuna valutazione finora

- Data FormattingDocumento2 pagineData FormattingRutvik MaheshwariNessuna valutazione finora

- Applied Compre S'22Documento3 pagineApplied Compre S'22Hafiz Saddique MalikNessuna valutazione finora

- ECON1192 - Group11 - Asm2 - 2022A - SGS (DI 72.5%)Documento39 pagineECON1192 - Group11 - Asm2 - 2022A - SGS (DI 72.5%)Quyên LươngNessuna valutazione finora

- Jai Kumar OgdcDocumento29 pagineJai Kumar OgdcVinod VaswaniNessuna valutazione finora

- Pr8 GraficosDocumento21 paginePr8 GraficosManuel Palenzuela HerreroNessuna valutazione finora

- Difference in Tax Rate in Micro FinanceDocumento2 pagineDifference in Tax Rate in Micro FinanceManisha AgarwalNessuna valutazione finora

- ChartDocumento1 paginaChartPuneet MaggoNessuna valutazione finora

- Detailed Income Statement Template Landscaping Irrigation Lighting CompanyDocumento4 pagineDetailed Income Statement Template Landscaping Irrigation Lighting Companymichael odiemboNessuna valutazione finora

- MacroEco Assignment-2Documento8 pagineMacroEco Assignment-2shashank sonalNessuna valutazione finora

- SR No. Year Face Value No. of Shares Dividend Per Share EPSDocumento10 pagineSR No. Year Face Value No. of Shares Dividend Per Share EPSPraharsha ChowdaryNessuna valutazione finora

- Assignment2 Dhairya - ShahDocumento7 pagineAssignment2 Dhairya - ShahAvani PatilNessuna valutazione finora

- Yearwise Comparative Up To 2017 18Documento1 paginaYearwise Comparative Up To 2017 18પ્રતિક પટેલNessuna valutazione finora

- Cir LTR 180.28 Da 43 Slabs MoreDocumento2 pagineCir LTR 180.28 Da 43 Slabs MorePiyush BajpaiNessuna valutazione finora

- Standalone Balance Sheet (Tata Motors) : AssetsDocumento43 pagineStandalone Balance Sheet (Tata Motors) : AssetsAniketNessuna valutazione finora

- COBADocumento4 pagineCOBA121890920Nessuna valutazione finora

- Demand PRICE (Percapita Income) LDEMAND Year Lprice LpcincDocumento5 pagineDemand PRICE (Percapita Income) LDEMAND Year Lprice LpcincRohit KumarNessuna valutazione finora

- Group 5Documento28 pagineGroup 5Kapil JainNessuna valutazione finora

- Ministry Write Up-2019Documento6 pagineMinistry Write Up-2019Md SolaimanNessuna valutazione finora

- Table 159: Foreign Investment Inflows: Total (A+B) Rs. Crore US $ MillionDocumento1 paginaTable 159: Foreign Investment Inflows: Total (A+B) Rs. Crore US $ MillionAbhimanyu Suresh KumarNessuna valutazione finora

- Valuation Model - CiplaDocumento37 pagineValuation Model - Ciplat2021basw010Nessuna valutazione finora

- Excel CalculationsDocumento146 pagineExcel CalculationsVaibhav RaulkarNessuna valutazione finora

- All India Bank Employees' Association: Happy News AIBEA's Unit in Bank of BarodaDocumento2 pagineAll India Bank Employees' Association: Happy News AIBEA's Unit in Bank of BarodaDevdutt MishraNessuna valutazione finora

- Case Study in Finman Final1Documento43 pagineCase Study in Finman Final1Jason CuregNessuna valutazione finora

- Reliance Data RevisedDocumento4 pagineReliance Data RevisedPhalangmiki NohriangNessuna valutazione finora

- Diffusion Data 4.10Documento12 pagineDiffusion Data 4.10Manan GuptaNessuna valutazione finora

- Table 116: Direct and Indirect Tax Revenues of Central and State GovernmentsDocumento1 paginaTable 116: Direct and Indirect Tax Revenues of Central and State Governmentsjena_01Nessuna valutazione finora

- BV Gorup 5Documento39 pagineBV Gorup 5Kapil JainNessuna valutazione finora

- Consolidated Breakout 2 Lac Se 20 CrorDocumento15 pagineConsolidated Breakout 2 Lac Se 20 CrorManoj Kumar TanwarNessuna valutazione finora

- Age Residual Plot Education Residual Plot: Regression StatisticsDocumento23 pagineAge Residual Plot Education Residual Plot: Regression Statisticsshubhanjali kesharwaniNessuna valutazione finora

- 2.3 Energy Consumption: 1. Gas (MM CFT) Transport CNG TotalDocumento8 pagine2.3 Energy Consumption: 1. Gas (MM CFT) Transport CNG TotalSamiullah QureshiNessuna valutazione finora

- PRC Ready ReckonerDocumento2 paginePRC Ready Reckonersparthan300Nessuna valutazione finora

- Cocal Hisotrical DataDocumento2 pagineCocal Hisotrical DatajoNessuna valutazione finora

- Income Statement-2014Quarterly - in MillionsDocumento6 pagineIncome Statement-2014Quarterly - in MillionsHKS TKSNessuna valutazione finora

- Progress ReportDocumento2 pagineProgress ReportSharath Kumar B.MNessuna valutazione finora

- R134a Thermo Prop Si NoRestrictionDocumento2 pagineR134a Thermo Prop Si NoRestrictionMahmoud AlFarajNessuna valutazione finora

- Excell File (Thompson Asset Management)Documento78 pagineExcell File (Thompson Asset Management)Shaubhik Das0% (1)

- Co Living Reshaping Rental Housing IndiaDocumento17 pagineCo Living Reshaping Rental Housing IndiaShaubhik DasNessuna valutazione finora

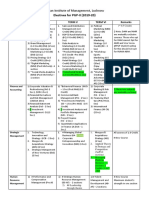

- Indian Institute of Management, Lucknow: Electives For PGP-II (2019-20)Documento7 pagineIndian Institute of Management, Lucknow: Electives For PGP-II (2019-20)Shaubhik DasNessuna valutazione finora

- Case - TISSDocumento3 pagineCase - TISSShaubhik DasNessuna valutazione finora

- Swachh BharatDocumento14 pagineSwachh BharatShaubhik DasNessuna valutazione finora

- Case Solution Liquid Chemical CompanyDocumento2 pagineCase Solution Liquid Chemical CompanyShaubhik DasNessuna valutazione finora

- 04 Trenovski Tashevska 2015 1 PDFDocumento21 pagine04 Trenovski Tashevska 2015 1 PDFArmin ČehićNessuna valutazione finora

- Economic Development Democratization and Environmental ProtectiDocumento33 pagineEconomic Development Democratization and Environmental Protectihaimi708Nessuna valutazione finora

- Ongoing Renewable Projects GeorgiaDocumento4 pagineOngoing Renewable Projects GeorgiamokarcanNessuna valutazione finora

- Public GoodDocumento48 paginePublic GoodPutri IndahSariNessuna valutazione finora

- Group 9 Design by Kate Case Analysis PDFDocumento7 pagineGroup 9 Design by Kate Case Analysis PDFSIMRANNessuna valutazione finora

- Housing Architecture: Literature Case StudiesDocumento4 pagineHousing Architecture: Literature Case StudiesJennifer PaulNessuna valutazione finora

- Low Cost CarriersDocumento24 pagineLow Cost CarriersMuhsin Azhar ShahNessuna valutazione finora

- EY Tax Alert Madras HC Rules Income Under Time Charter Arrangement For Ships As RoyaltyDocumento6 pagineEY Tax Alert Madras HC Rules Income Under Time Charter Arrangement For Ships As Royaltyace kingNessuna valutazione finora

- VJEPADocumento6 pagineVJEPATrang ThuNessuna valutazione finora

- Anta Tirta Kirana 1Documento1 paginaAnta Tirta Kirana 1yosi widianaNessuna valutazione finora

- Controlling The Global EconomyDocumento22 pagineControlling The Global EconomyCetkinNessuna valutazione finora

- Class Activity - Bus685Documento7 pagineClass Activity - Bus685bonna1234567890Nessuna valutazione finora

- Chapter 2 Activity 2 1Documento3 pagineChapter 2 Activity 2 1Wild RiftNessuna valutazione finora

- John Carroll University Magazine Fall 2009Documento84 pagineJohn Carroll University Magazine Fall 2009johncarrolluniversity100% (1)

- Asg1 - Nagakin Capsule TowerDocumento14 pagineAsg1 - Nagakin Capsule TowerSatyam GuptaNessuna valutazione finora

- Why Blue-Collar Workers Quit Their JobDocumento4 pagineWhy Blue-Collar Workers Quit Their Jobsiva csNessuna valutazione finora

- 7 - General Equilibrium Under UncertaintyDocumento5 pagine7 - General Equilibrium Under UncertaintyLuis Aragonés FerriNessuna valutazione finora

- The True Impact of TRIDDocumento2 pagineThe True Impact of TRIDDanRanckNessuna valutazione finora

- InvoicehhhhDocumento1 paginaInvoicehhhhAravind RNessuna valutazione finora

- Strategic Options For Building CompetitivenessDocumento53 pagineStrategic Options For Building Competitivenessjeet_singh_deepNessuna valutazione finora

- Business Plan of Budaya KopiDocumento12 pagineBusiness Plan of Budaya KopiDeccy Shi-Shi100% (1)

- VipulDocumento14 pagineVipulmhpatel4581Nessuna valutazione finora

- Income Tax Declaration Form - 2014-15Documento2 pagineIncome Tax Declaration Form - 2014-15Ketan Tiwari0% (1)

- LA - Who Is Behind The Pelican InstituteDocumento1 paginaLA - Who Is Behind The Pelican InstituteprogressnowNessuna valutazione finora

- Layman's Guide To Pair TradingDocumento9 pagineLayman's Guide To Pair TradingaporatNessuna valutazione finora

- Conversations in Colombia, S. Gudeman and A. RiveraDocumento217 pagineConversations in Colombia, S. Gudeman and A. RiveraAnonymous OeCloZYzNessuna valutazione finora

- GTU Question BankDocumento3 pagineGTU Question Bankamit raningaNessuna valutazione finora

- Chapter 15 Test BankDocumento24 pagineChapter 15 Test BankMarc GaoNessuna valutazione finora

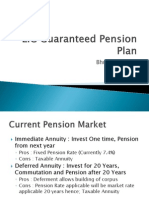

- LIC Guaranteed HNI Pension PlanDocumento9 pagineLIC Guaranteed HNI Pension PlanBhushan ShethNessuna valutazione finora

- Universal Remote SUPERIOR AIRCO 1000 in 1 For AirCoDocumento2 pagineUniversal Remote SUPERIOR AIRCO 1000 in 1 For AirCoceteganNessuna valutazione finora