Potrebbero piacerti anche

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Da EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Valutazione: 5 su 5 stelle5/5 (1)

- A. Receivable 350.000.000 (DR) Real Estate 350.000.000 (CR)Documento3 pagineA. Receivable 350.000.000 (DR) Real Estate 350.000.000 (CR)Diki SetiyawanNessuna valutazione finora

- Multiple Choice Questions: Chapter 8 Consolidations - Changes in Ownership InterestsDocumento36 pagineMultiple Choice Questions: Chapter 8 Consolidations - Changes in Ownership InterestsHamza JalalNessuna valutazione finora

- Lets Analyze Bvps and Eps ParconDocumento9 pagineLets Analyze Bvps and Eps ParconJeric TorionNessuna valutazione finora

- Accounting for Notes Payable, Contingent Liabilities, and Stock IssuancesDocumento5 pagineAccounting for Notes Payable, Contingent Liabilities, and Stock IssuancesEzy Tri TANessuna valutazione finora

- Partnership Capital Balances After Admitting New PartnerDocumento3 paginePartnership Capital Balances After Admitting New PartnerNurul AryaniNessuna valutazione finora

- Course Audit Partnership PART 2Documento6 pagineCourse Audit Partnership PART 2Jennifer VergaraNessuna valutazione finora

- Bsc. Sem - Corporate Finance - Final Exam: Question 1Documento4 pagineBsc. Sem - Corporate Finance - Final Exam: Question 1Derek LowNessuna valutazione finora

- Soal Indirect N MutualDocumento9 pagineSoal Indirect N MutualarifNessuna valutazione finora

- Revision Questions - Q&ADocumento3 pagineRevision Questions - Q&Arosario correiaNessuna valutazione finora

- Payback Period Calculation for $400K Machine InvestmentDocumento1 paginaPayback Period Calculation for $400K Machine InvestmentMagsaysay SouthNessuna valutazione finora

- Reviewer For Midterm XFINMAR A224and A225Documento5 pagineReviewer For Midterm XFINMAR A224and A225ralph11240308Nessuna valutazione finora

- Self-Assessment 02 - Retained Earnings quiz solutionsDocumento12 pagineSelf-Assessment 02 - Retained Earnings quiz solutionsKarl ExacNessuna valutazione finora

- Calculate Conversion Prices, Ratios and Values for Convertible BondsDocumento4 pagineCalculate Conversion Prices, Ratios and Values for Convertible BondsGailee VinNessuna valutazione finora

- Solution of Assignment Eco-04 Case: Mike (The Plumber) - A True StoryDocumento5 pagineSolution of Assignment Eco-04 Case: Mike (The Plumber) - A True StoryYusuf HusseinNessuna valutazione finora

- Revision Sheet Dr. SaraDocumento17 pagineRevision Sheet Dr. SaraSeif HishamNessuna valutazione finora

- CH 15Documento8 pagineCH 15Ansley0% (1)

- Finance 8174787Documento2 pagineFinance 8174787erikyryangNessuna valutazione finora

- Liabilities PDFDocumento3 pagineLiabilities PDFJessie jorgeNessuna valutazione finora

- 109_2_____________________________.pdfDocumento3 pagine109_2_____________________________.pdf112205013Nessuna valutazione finora

- CR Par Value PC $ 1,000 $ 40: 25 SharesDocumento4 pagineCR Par Value PC $ 1,000 $ 40: 25 SharesBought By UsNessuna valutazione finora

- Phantasies, Incorporation: Debt Versus Equity Financing FM-135 (MWF-9:00 Am To 10:00 Am)Documento8 paginePhantasies, Incorporation: Debt Versus Equity Financing FM-135 (MWF-9:00 Am To 10:00 Am)dianaNessuna valutazione finora

- CHAPTER 3 - PracticeExerciseDocumento5 pagineCHAPTER 3 - PracticeExerciseSerenity CarlyeNessuna valutazione finora

- Final RevisionDocumento13 pagineFinal Revisionaabdelnasser014Nessuna valutazione finora

- Tugas Minggu Ke 5Documento4 pagineTugas Minggu Ke 5Devenda Kartika RoffandiNessuna valutazione finora

- BSA2BQuiz 3Documento19 pagineBSA2BQuiz 3Monica Enrico0% (1)

- Tugas AKL 1 TM 9Documento8 pagineTugas AKL 1 TM 9Dila PujiNessuna valutazione finora

- Answers To Reviewer in Acctg 2Documento3 pagineAnswers To Reviewer in Acctg 2Fatima AsprerNessuna valutazione finora

- Quiz 1 Answers and Solutions (Partnership Formation and Operation)Documento6 pagineQuiz 1 Answers and Solutions (Partnership Formation and Operation)cpacpacpaNessuna valutazione finora

- Soal Indirect N MutualDocumento6 pagineSoal Indirect N MutualGerry Neka KantakiNessuna valutazione finora

- Kuis - Financial Lab ModelingDocumento2 pagineKuis - Financial Lab Modelingalexandersur9Nessuna valutazione finora

- ACT1106-Midterm Quiz No. 3 With AnswerDocumento6 pagineACT1106-Midterm Quiz No. 3 With AnswerPj Dela VegaNessuna valutazione finora

- GROUP_6.pdfDocumento14 pagineGROUP_6.pdframuxeNessuna valutazione finora

- Chap16 ProblemsDocumento20 pagineChap16 ProblemsYen YenNessuna valutazione finora

- Principles of FinanceDocumento7 paginePrinciples of FinanceAslam Abdullah MarufNessuna valutazione finora

- Problems Partnership Dissolution and LiquidationDocumento5 pagineProblems Partnership Dissolution and LiquidationNick ivan AlvaresNessuna valutazione finora

- Test 1 W AnswersDocumento8 pagineTest 1 W AnswersVaniamarie VasquezNessuna valutazione finora

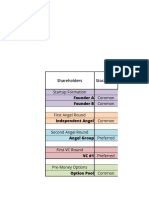

- Cloud Solutions, Inc. Capitalization Table: at Formation: Security $/share Date $ PaidDocumento7 pagineCloud Solutions, Inc. Capitalization Table: at Formation: Security $/share Date $ PaidSteve MedhurstNessuna valutazione finora

- Chapter 8-10 Test BankDocumento80 pagineChapter 8-10 Test BankELSA SYAFIRA ANANTANessuna valutazione finora

- Drill No.1 To No.4 - ACF101Documento3 pagineDrill No.1 To No.4 - ACF101Fermalan, Gabriel P.Nessuna valutazione finora

- ACCT4010 Group Assignment SolutionsDocumento3 pagineACCT4010 Group Assignment SolutionsSin TungNessuna valutazione finora

- Calculate Valuation and Ownership Changes at Funding StagesDocumento8 pagineCalculate Valuation and Ownership Changes at Funding StagesToto ヅ GarmontoNessuna valutazione finora

- (Corporate Finance) SUMMARY OF EXERCISES PDFDocumento9 pagine(Corporate Finance) SUMMARY OF EXERCISES PDFneda ajaminNessuna valutazione finora

- Assignment 10 Partnership DissolutionDocumento8 pagineAssignment 10 Partnership DissolutionSova ShockdartNessuna valutazione finora

- Final Exam CorporateDocumento4 pagineFinal Exam CorporateCiptawan CenNessuna valutazione finora

- Dewi Nabilah Anwar - Akl1 Week 2Documento3 pagineDewi Nabilah Anwar - Akl1 Week 2Soe BagyoNessuna valutazione finora

- ABC Acquires DEF Company Assets and Liabilities Business CombinationDocumento15 pagineABC Acquires DEF Company Assets and Liabilities Business CombinationJonas Avanzado TianiaNessuna valutazione finora

- Corporation: D. Effective Yield or Market Rate. Use The Following Information For Questions 2 and 3Documento8 pagineCorporation: D. Effective Yield or Market Rate. Use The Following Information For Questions 2 and 3ibrahim mohamedNessuna valutazione finora

- RMK Akl Hal 544-549Documento5 pagineRMK Akl Hal 544-549Dizzy nindyaNessuna valutazione finora

- Founders Pocket Guide Cap TableDocumento10 pagineFounders Pocket Guide Cap TableVenkatesh Mahalingam100% (1)

- Total Excess of Cost Over Book Value Acquired $4,000,000Documento5 pagineTotal Excess of Cost Over Book Value Acquired $4,000,000SAHRINDA YUNIAWATINessuna valutazione finora

- 2009-02-27 005030 SharpeDocumento6 pagine2009-02-27 005030 SharpeAndrea RobinsonNessuna valutazione finora

- Problems 14-5, 14-9, 14-20 cash flow analysisDocumento4 pagineProblems 14-5, 14-9, 14-20 cash flow analysisNicol Escobar HerreraNessuna valutazione finora

- Total Excess of Cost Over Book Value Acquired $4,000,000Documento5 pagineTotal Excess of Cost Over Book Value Acquired $4,000,000SAHRINDA YUNIAWATINessuna valutazione finora

- Paki Check BiDocumento5 paginePaki Check BiAusan AbdullahNessuna valutazione finora

- Acc 550 Week 4 HomeworkDocumento7 pagineAcc 550 Week 4 Homeworkjoannapsmith33Nessuna valutazione finora

- Company Accounts Practice Questions - Nov 2, 2020Documento8 pagineCompany Accounts Practice Questions - Nov 2, 2020tahreemNessuna valutazione finora

- BE - Stockholders' Equity ADocumento5 pagineBE - Stockholders' Equity ALuis JoseNessuna valutazione finora

- Far Finals Practice ReviewerDocumento4 pagineFar Finals Practice ReviewerflatunocutieNessuna valutazione finora

- Assignment 2 1Documento12 pagineAssignment 2 1ThomasNessuna valutazione finora

- LVMH Consolidated Statements PDFDocumento74 pagineLVMH Consolidated Statements PDFThomasNessuna valutazione finora

- Relationship Between Hedge Profit and Jet Fuel PriceDocumento4 pagineRelationship Between Hedge Profit and Jet Fuel PriceThomasNessuna valutazione finora

- Assignment 2Documento9 pagineAssignment 2ThomasNessuna valutazione finora

- CV - Abhay Kumar SahooDocumento1 paginaCV - Abhay Kumar SahootatsatNessuna valutazione finora

- Abrams CaseDocumento11 pagineAbrams CaseFahmi A. MubarokNessuna valutazione finora

- Dividend Decision and Valuation of FirmDocumento24 pagineDividend Decision and Valuation of FirmAnkita MukherjeeNessuna valutazione finora

- Risk Aversion, Neutrality, and PreferencesDocumento2 pagineRisk Aversion, Neutrality, and PreferencesAryaman JunejaNessuna valutazione finora

- Rejda Ch02Documento22 pagineRejda Ch02Saiful IslamNessuna valutazione finora

- A Comparative Financial Analysis of Soft Drink IndustryDocumento41 pagineA Comparative Financial Analysis of Soft Drink Industryvs1513100% (1)

- Jzanzig - Acc 512 - Chapter 12Documento27 pagineJzanzig - Acc 512 - Chapter 12lehvrhon100% (1)

- Oliva - Sales Incentive Design Best PracticesDocumento36 pagineOliva - Sales Incentive Design Best PracticesMonica EscribaNessuna valutazione finora

- Financial Statements of HSYDocumento16 pagineFinancial Statements of HSYAqsa Umer0% (2)

- Disini StartUpGuide InteractiveDocumento19 pagineDisini StartUpGuide InteractiveDammy VegaNessuna valutazione finora

- Quiz No. 1Documento2 pagineQuiz No. 1rex tanongNessuna valutazione finora

- Team Member Details and Company OverviewDocumento28 pagineTeam Member Details and Company OverviewMuhammad Mubashir0% (1)

- Ratio AnalysisDocumento15 pagineRatio AnalysisChandana DasNessuna valutazione finora

- Loan Life CycleDocumento7 pagineLoan Life CyclePushpraj Singh Baghel100% (1)

- About Company: World, Processing Sophisticated UHP (Ultra High Power)Documento24 pagineAbout Company: World, Processing Sophisticated UHP (Ultra High Power)RJ Rishabh TyagiNessuna valutazione finora

- BitRoyal Exchange Ltd. Is Globally Launching A New Crypto Trading PlatformDocumento2 pagineBitRoyal Exchange Ltd. Is Globally Launching A New Crypto Trading PlatformPR.comNessuna valutazione finora

- The Black-Scholes-Merton Model ExplainedDocumento49 pagineThe Black-Scholes-Merton Model ExplainedLaxus DreyerNessuna valutazione finora

- Financial Service: III SemDocumento3 pagineFinancial Service: III SemSundarachselvan Subramanian0% (1)

- High Rock Industries CaseDocumento19 pagineHigh Rock Industries CaseRohan Raj MishraNessuna valutazione finora

- Computer Simulation With Crystal Ball Solution To Solved ProblemsDocumento3 pagineComputer Simulation With Crystal Ball Solution To Solved Problemsprashantgargindia_93Nessuna valutazione finora

- The Common-Sense Path To Financial FreedomDocumento20 pagineThe Common-Sense Path To Financial Freedomclarkpd6100% (3)

- Fin1 Eq2 BsatDocumento1 paginaFin1 Eq2 BsatYu BabylanNessuna valutazione finora

- Igor Iankovskyi: at The Intersection of Professions: How To Reinvent The Innovative Potential of UkrainiansDocumento2 pagineIgor Iankovskyi: at The Intersection of Professions: How To Reinvent The Innovative Potential of UkrainiansInitiative for the FutureNessuna valutazione finora

- Assignment 9 - QuestionsDocumento3 pagineAssignment 9 - QuestionstasleemfcaNessuna valutazione finora

- Deloitte Doing Business Guide KSA 2017Documento32 pagineDeloitte Doing Business Guide KSA 2017HunterNessuna valutazione finora

- Project On Capital Market ReformsDocumento99 pagineProject On Capital Market Reformsthorat82100% (3)

- Chapter 02Documento50 pagineChapter 02Huy HoangNessuna valutazione finora

- Cost of CapitalDocumento62 pagineCost of CapitalJustin RenovatedNessuna valutazione finora

- 2.historical Evolution of ManagementDocumento8 pagine2.historical Evolution of Managementreduan ferdousNessuna valutazione finora

- Hashoo Foundation's Credit and Enterprise Development (CED) For Social Entrepreneurship Program (UST SEP)Documento28 pagineHashoo Foundation's Credit and Enterprise Development (CED) For Social Entrepreneurship Program (UST SEP)Cristal MontanezNessuna valutazione finora