Potrebbero piacerti anche

- Jo 1Documento615 pagineJo 1BRENDAFUENZALIDA2011Nessuna valutazione finora

- Modem Support TP-link MR3220Documento7 pagineModem Support TP-link MR3220Timotius Ivan CaseyNessuna valutazione finora

- Nokia PCB IC ListDocumento4 pagineNokia PCB IC Listdsrinath912Nessuna valutazione finora

- TDocumento38 pagineTgauravsharmacl2007Nessuna valutazione finora

- ATM List PDFDocumento76 pagineATM List PDFMidhun PGNessuna valutazione finora

- Checkra - in Compatibility Sheet (Iphone, Ipod - Ipad) - All Tested Tweaks - Iphone - IpodDocumento5 pagineCheckra - in Compatibility Sheet (Iphone, Ipod - Ipad) - All Tested Tweaks - Iphone - IpodAcho SaguNessuna valutazione finora

- IMEI NumbersDocumento11 pagineIMEI Numberslolzzz100% (1)

- Kode TK KPJ Nomor Identitas Nama LengkapDocumento10 pagineKode TK KPJ Nomor Identitas Nama LengkapHari ApriNessuna valutazione finora

- Motorola Moto G 2nd Generation User GuideDocumento68 pagineMotorola Moto G 2nd Generation User GuideJoel QuezadaNessuna valutazione finora

- SniffingDocumento120 pagineSniffingWoyNessuna valutazione finora

- Lecture 22-Lecture 23 PDFDocumento51 pagineLecture 22-Lecture 23 PDFSopnil Golay TamangNessuna valutazione finora

- Whats NewerzezrezDocumento45 pagineWhats NewerzezrezAbdellatif HabbazNessuna valutazione finora

- Ramdump Modem 2023-02-20 04-47-27 PropsDocumento20 pagineRamdump Modem 2023-02-20 04-47-27 PropsdavNessuna valutazione finora

- History 11 Mei 2022Documento16 pagineHistory 11 Mei 2022ERANessuna valutazione finora

- Verizon-Bnc - RFC FullDocumento36 pagineVerizon-Bnc - RFC FullValerio BitontiNessuna valutazione finora

- Id BSCDocumento190 pagineId BSCBucek BuddyNessuna valutazione finora

- At Commands by ZTEDocumento62 pagineAt Commands by ZTEkalyanmn100% (1)

- Free Dreambox Server Sicnified by HazalDocumento3 pagineFree Dreambox Server Sicnified by Hazala6120903Nessuna valutazione finora

- Base Colpa 5mil JNDocumento628 pagineBase Colpa 5mil JNHuber GonzálezNessuna valutazione finora

- Consistency ChecksDocumento2.488 pagineConsistency Checksmaih_wNessuna valutazione finora

- CC by Sa 3.0Documento5 pagineCC by Sa 3.0Nicolas Cardenas jaramillo HDNessuna valutazione finora

- ANKUSH KUMAR GAUTAM - Mobile PDFDocumento1 paginaANKUSH KUMAR GAUTAM - Mobile PDFWesley Tom FritzNessuna valutazione finora

- Pin Member Whatsapp IndonesiaDocumento64 paginePin Member Whatsapp IndonesiaYudha Ari N0% (2)

- Quectel LTE Standard HTTP (S) Application Note V1.1Documento39 pagineQuectel LTE Standard HTTP (S) Application Note V1.1Girish BelagaliNessuna valutazione finora

- List User-Agent Switcher 110 Device BerbedaDocumento7 pagineList User-Agent Switcher 110 Device BerbedaYohanes Stenly SetiawanNessuna valutazione finora

- Quectel EC20 at Commands ManualDocumento231 pagineQuectel EC20 at Commands ManualRajkumar SinghNessuna valutazione finora

- Quectel Cellular Engine: AT CommandsDocumento14 pagineQuectel Cellular Engine: AT CommandsvijayforrockNessuna valutazione finora

- Play Credit Card Terms and ConditionsDocumento3 paginePlay Credit Card Terms and ConditionsBil KumarNessuna valutazione finora

- Template For IMEI UploadDocumento6 pagineTemplate For IMEI UploadManjeet KumarNessuna valutazione finora

- GpaisdiyDocumento294 pagineGpaisdiyNiesa Hanum MNessuna valutazione finora

- Imei AssignDocumento3 pagineImei AssignRoberto RiccioNessuna valutazione finora

- Nokia CodeDocumento1 paginaNokia Codebhavinbpatel6961Nessuna valutazione finora

- 3G Compatibility ListDocumento8 pagine3G Compatibility ListAdam FluertyNessuna valutazione finora

- Imei UnlockDocumento734 pagineImei UnlockFarel SiraitNessuna valutazione finora

- Level 3 Repair: 8-1. Components LayoutDocumento22 pagineLevel 3 Repair: 8-1. Components Layoutshamsudin yassinNessuna valutazione finora

- Binance LoginPassDocumento5 pagineBinance LoginPassGui VieraNessuna valutazione finora

- Theft Aware 2.00 For AndroidDocumento25 pagineTheft Aware 2.00 For Androiddomy_osNessuna valutazione finora

- Banks Reports FebDocumento4 pagineBanks Reports FebshayankiitNessuna valutazione finora

- Hot Fixes 14may22Documento81 pagineHot Fixes 14may22bhherhfdr0% (1)

- Bin MubiDocumento2 pagineBin MubiMoises AnibalNessuna valutazione finora

- Sprint Complete: Equipment Service and Repair Service Contract Program (ESRP) Effective November 2021Documento4 pagineSprint Complete: Equipment Service and Repair Service Contract Program (ESRP) Effective November 2021SeanNessuna valutazione finora

- Automation. PDF DocumenDocumento1 paginaAutomation. PDF DocumenBhavin GamiNessuna valutazione finora

- Wireless Mesh NetworksDocumento7 pagineWireless Mesh NetworksXyrille GalvezNessuna valutazione finora

- IETE Mid-Term Symposium: Cryptocurrencies and Cyber CrimesDocumento120 pagineIETE Mid-Term Symposium: Cryptocurrencies and Cyber CrimesAnupam TiwariNessuna valutazione finora

- BSNL Broadband Wireless (WiFi) Configuration Step by Step Procedure How ToDocumento5 pagineBSNL Broadband Wireless (WiFi) Configuration Step by Step Procedure How ToSubramanian PeriyanainaNessuna valutazione finora

- Termux For PC (2020) - Free Download For Windows 10 - 8 - 7Documento6 pagineTermux For PC (2020) - Free Download For Windows 10 - 8 - 7eliezerNessuna valutazione finora

- GPS Vehicle TrackDocumento132 pagineGPS Vehicle TrackKarthik DmNessuna valutazione finora

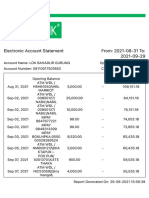

- Account StatementDocumento2 pagineAccount StatementGaurav MishraNessuna valutazione finora

- Kheadaha2 PDFDocumento422 pagineKheadaha2 PDFSukalyan BhadraNessuna valutazione finora

- Debug 1214Documento4 pagineDebug 1214Dobrán László AttilaNessuna valutazione finora

- Ingenico - 9500 - (I9500 - Betalingsterminal - Integrasjonsguide - V1.4)Documento49 pagineIngenico - 9500 - (I9500 - Betalingsterminal - Integrasjonsguide - V1.4)kees van der walNessuna valutazione finora

- NMS Transceiver Codes Global - v2.3 RevisedDocumento699 pagineNMS Transceiver Codes Global - v2.3 Revisedyudi pramNessuna valutazione finora

- Symmetry: Methods and Tools of Digital Triage in Forensic Context: Survey and Future DirectionsDocumento20 pagineSymmetry: Methods and Tools of Digital Triage in Forensic Context: Survey and Future DirectionsAgungdarono UserNessuna valutazione finora

- NS Writeup 03Documento7 pagineNS Writeup 03AkashNessuna valutazione finora

- CIS Apple iOS 15 and iPadOS 15 Benchmark v1.1.0Documento259 pagineCIS Apple iOS 15 and iPadOS 15 Benchmark v1.1.0him2000himNessuna valutazione finora

- Numeros SeriaisDocumento7 pagineNumeros SeriaisAnonymous FfMBms3eWRNessuna valutazione finora

- Reliance GSM New Ussd CodesDocumento1 paginaReliance GSM New Ussd CodesNarayana ReddyNessuna valutazione finora

- Toshiba Tecra Portege Qosmio Libretto Bios Password Unlock GuideDocumento4 pagineToshiba Tecra Portege Qosmio Libretto Bios Password Unlock GuideLaptop Rebirth50% (2)

- HSM 3des Key Pairs Generator and Composer For Combining KeysDocumento5 pagineHSM 3des Key Pairs Generator and Composer For Combining Keyssajad salehiNessuna valutazione finora

- Assignment 4Documento5 pagineAssignment 4Hafiz AhmadNessuna valutazione finora

- Soil NailingDocumento6 pagineSoil Nailingvinodreddy146Nessuna valutazione finora

- 82686b - LOAD SHARING MODULEDocumento2 pagine82686b - LOAD SHARING MODULENguyễn Đình ĐứcNessuna valutazione finora

- Introduction To DifferentiationDocumento10 pagineIntroduction To DifferentiationaurennosNessuna valutazione finora

- List of Some Common Surgical TermsDocumento5 pagineList of Some Common Surgical TermsShakil MahmodNessuna valutazione finora

- Semi Detailed Lesson PlanDocumento2 pagineSemi Detailed Lesson PlanJean-jean Dela Cruz CamatNessuna valutazione finora

- Data StructuresDocumento4 pagineData StructuresBenjB1983Nessuna valutazione finora

- Feed-Pump Hydraulic Performance and Design Improvement, Phase I: J2esearch Program DesignDocumento201 pagineFeed-Pump Hydraulic Performance and Design Improvement, Phase I: J2esearch Program DesignJonasNessuna valutazione finora

- P 348Documento196 pagineP 348a123456978Nessuna valutazione finora

- Dec JanDocumento6 pagineDec Janmadhujayan100% (1)

- Recruitment SelectionDocumento11 pagineRecruitment SelectionMOHAMMED KHAYYUMNessuna valutazione finora

- Internship Report Format For Associate Degree ProgramDocumento5 pagineInternship Report Format For Associate Degree ProgramBisma AmjaidNessuna valutazione finora

- 385C Waw1-Up PDFDocumento4 pagine385C Waw1-Up PDFJUNA RUSANDI SNessuna valutazione finora

- I I I I: Peroxid.Q!Documento2 pagineI I I I: Peroxid.Q!Diego PradelNessuna valutazione finora

- Brigade Product Catalogue Edition 20 EnglishDocumento88 pagineBrigade Product Catalogue Edition 20 EnglishPelotudoPeloteroNessuna valutazione finora

- Computers in Industry: Hugh Boyes, Bil Hallaq, Joe Cunningham, Tim Watson TDocumento12 pagineComputers in Industry: Hugh Boyes, Bil Hallaq, Joe Cunningham, Tim Watson TNawabMasidNessuna valutazione finora

- Product NDC # Compare To Strength Size Form Case Pack Abcoe# Cardinal Cin # Mckesson Oe # M&Doe#Documento14 pagineProduct NDC # Compare To Strength Size Form Case Pack Abcoe# Cardinal Cin # Mckesson Oe # M&Doe#Paras ShardaNessuna valutazione finora

- ENT 300 Individual Assessment-Personal Entrepreneurial CompetenciesDocumento8 pagineENT 300 Individual Assessment-Personal Entrepreneurial CompetenciesAbu Ammar Al-hakimNessuna valutazione finora

- Myanmar 1Documento3 pagineMyanmar 1Shenee Kate BalciaNessuna valutazione finora

- Arduino Uno CNC ShieldDocumento11 pagineArduino Uno CNC ShieldMărian IoanNessuna valutazione finora

- Research 093502Documento8 pagineResearch 093502Chrlszjhon Sales SuguitanNessuna valutazione finora

- Solubility Product ConstantsDocumento6 pagineSolubility Product ConstantsBilal AhmedNessuna valutazione finora

- Iaea Tecdoc 1092Documento287 pagineIaea Tecdoc 1092Andres AracenaNessuna valutazione finora

- 2-1. Drifting & Tunneling Drilling Tools PDFDocumento9 pagine2-1. Drifting & Tunneling Drilling Tools PDFSubhash KediaNessuna valutazione finora

- NABARD R&D Seminar FormatDocumento7 pagineNABARD R&D Seminar FormatAnupam G. RatheeNessuna valutazione finora

- Smart Gas Leakage Detection With Monitoring and Automatic Safety SystemDocumento4 pagineSmart Gas Leakage Detection With Monitoring and Automatic Safety SystemYeasin Arafat FahadNessuna valutazione finora

- Conservation Assignment 02Documento16 pagineConservation Assignment 02RAJU VENKATANessuna valutazione finora

- Business-Communication Solved MCQs (Set-3)Documento8 pagineBusiness-Communication Solved MCQs (Set-3)Pavan Sai Krishna KottiNessuna valutazione finora

- Kosher Leche Descremada Dairy America Usa Planta TiptonDocumento2 pagineKosher Leche Descremada Dairy America Usa Planta Tiptontania SaezNessuna valutazione finora

- CS-6777 Liu AbsDocumento103 pagineCS-6777 Liu AbsILLA PAVAN KUMAR (PA2013003013042)Nessuna valutazione finora