Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Fuji Apple, Walnut and Herb Salad With Roasted ChickenDocumento1 paginaFuji Apple, Walnut and Herb Salad With Roasted ChickengretatamaraNessuna valutazione finora

- Chickpea and Roasted Pepper SoupDocumento1 paginaChickpea and Roasted Pepper SoupgretatamaraNessuna valutazione finora

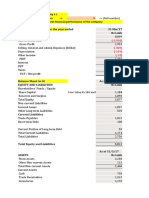

- Accounting Fundamentals II: Lesson 8 (Printer-Friendly Version)Documento7 pagineAccounting Fundamentals II: Lesson 8 (Printer-Friendly Version)gretatamaraNessuna valutazione finora

- Garlic Mashed Potato PancakesDocumento1 paginaGarlic Mashed Potato PancakesgretatamaraNessuna valutazione finora

- Lemon-Pecan PancakesDocumento1 paginaLemon-Pecan PancakesgretatamaraNessuna valutazione finora

- General Journal: Account Title Date Debit Credit Doc. NO. Post RefDocumento17 pagineGeneral Journal: Account Title Date Debit Credit Doc. NO. Post RefgretatamaraNessuna valutazione finora

- Accounting Fundamentals II: Quizzes: Lesson 9 Quiz ResultsDocumento2 pagineAccounting Fundamentals II: Quizzes: Lesson 9 Quiz ResultsgretatamaraNessuna valutazione finora

- Final Test QuestionsDocumento10 pagineFinal Test Questionsgretatamara0% (1)

- L09 SolutionsDocumento3 pagineL09 SolutionsgretatamaraNessuna valutazione finora

- L12 SolutionsDocumento15 pagineL12 SolutionsgretatamaraNessuna valutazione finora

- L01 Quiz1Documento2 pagineL01 Quiz1gretatamaraNessuna valutazione finora

- L02 SolutionsDocumento2 pagineL02 SolutionsgretatamaraNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1091)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Ds 3316063110100820221665188750035Documento3 pagineDs 3316063110100820221665188750035rey lunaNessuna valutazione finora

- FinMan WORKING CAPITAL MANAGEMENT - For PrintingDocumento46 pagineFinMan WORKING CAPITAL MANAGEMENT - For PrintingLito Jose Perez LalantaconNessuna valutazione finora

- Inflation Definition, WPI, CPI, Measurement and CausesDocumento2 pagineInflation Definition, WPI, CPI, Measurement and Causesatikbarbhuiya1432Nessuna valutazione finora

- Fa 3 Chapter 15 Error CorrectionDocumento5 pagineFa 3 Chapter 15 Error CorrectionKristine Florence Tolentino100% (1)

- Chapter 1 - Introduction To Managerial AccountingDocumento22 pagineChapter 1 - Introduction To Managerial AccountingviraNessuna valutazione finora

- Imtsons Investments LTDDocumento18 pagineImtsons Investments LTDAakashNessuna valutazione finora

- Promissory Note PDFDocumento16 paginePromissory Note PDFElma Picardal RejanoNessuna valutazione finora

- Purchase Order: Unit of Purchase Quantity Net Value (GBP) FB42PL16Documento2 paginePurchase Order: Unit of Purchase Quantity Net Value (GBP) FB42PL16pj4allNessuna valutazione finora

- Ch05 Tool KitDocumento31 pagineCh05 Tool KitAdamNessuna valutazione finora

- Mining Industry PresentationsDocumento38 pagineMining Industry Presentationspoitan2Nessuna valutazione finora

- Pilipinas Bank Vs CADocumento2 paginePilipinas Bank Vs CAHansel Jake B. PampiloNessuna valutazione finora

- CoreFund Capital, LLC Appoints Bonnie Castillo New PresidentDocumento2 pagineCoreFund Capital, LLC Appoints Bonnie Castillo New PresidentPR.comNessuna valutazione finora

- Energy: Andr e Månsson, Bengt Johansson, Lars J. NilssonDocumento14 pagineEnergy: Andr e Månsson, Bengt Johansson, Lars J. NilssonCarlos AlvarezNessuna valutazione finora

- Notes: Nell Doctrine (In Relation To Corporation's Power To Sell or Dispose Its Assets)Documento2 pagineNotes: Nell Doctrine (In Relation To Corporation's Power To Sell or Dispose Its Assets)Jovelle Zabala CayabanNessuna valutazione finora

- User ManualDocumento51 pagineUser ManualaNessuna valutazione finora

- BUS 5111 - Financial Management-Portfolio Activity Unit 4Documento4 pagineBUS 5111 - Financial Management-Portfolio Activity Unit 4LaVida LocaNessuna valutazione finora

- APM Assignment 2 - by SameeraDocumento18 pagineAPM Assignment 2 - by SameeraRahull GurnaniNessuna valutazione finora

- User Manual Learning Phase V2206Documento40 pagineUser Manual Learning Phase V2206Harsh DedhiaNessuna valutazione finora

- Class 12 Accountancy Solved Sample Paper 2 - 2012Documento37 pagineClass 12 Accountancy Solved Sample Paper 2 - 2012cbsestudymaterialsNessuna valutazione finora

- CardProtect PDSDocumento21 pagineCardProtect PDSPhilip GardinerNessuna valutazione finora

- Decentralize Smart Contract PlatformDocumento12 pagineDecentralize Smart Contract PlatformSindhu ThomasNessuna valutazione finora

- Reynaldo S. Nicolas - Devices Affecting Control Under The Corporation CodeDocumento35 pagineReynaldo S. Nicolas - Devices Affecting Control Under The Corporation CodesaverjaneNessuna valutazione finora

- Facebook IncDocumento154 pagineFacebook IncEon SandyNessuna valutazione finora

- The Philippine Charity Sweepstakes Office: Who Is The Owner of PCSO?Documento2 pagineThe Philippine Charity Sweepstakes Office: Who Is The Owner of PCSO?Nicole CabalanNessuna valutazione finora

- PetroRabigh E ProspectusDocumento132 paginePetroRabigh E Prospectusvineet_bmNessuna valutazione finora

- Mcbride p3 Exercises and AnswersDocumento55 pagineMcbride p3 Exercises and Answersapi-260512563Nessuna valutazione finora

- SCB Supervalue Titanium.Documento2 pagineSCB Supervalue Titanium.sanket shahNessuna valutazione finora

- REPUBLIC ACT No 10072Documento6 pagineREPUBLIC ACT No 10072dteroseNessuna valutazione finora

- The State of Fashion 2020 VFDocumento108 pagineThe State of Fashion 2020 VFpapaniko80% (5)

- Accounting Vocabulary: Easy-To-Learn English Terms For AccountingDocumento6 pagineAccounting Vocabulary: Easy-To-Learn English Terms For AccountingHamza El MissouabNessuna valutazione finora