Potrebbero piacerti anche

- ADVANCED CREDIT REPAIR SECRETS REVEALED: The Definitive Guide to Repair and Build Your Credit FastDa EverandADVANCED CREDIT REPAIR SECRETS REVEALED: The Definitive Guide to Repair and Build Your Credit FastValutazione: 5 su 5 stelle5/5 (3)

- How to Retire Debt-Free and Wealthy: A Finance Coach Reveals the Secrets, Tips, and Techniques of How Clients Become MillionairesDa EverandHow to Retire Debt-Free and Wealthy: A Finance Coach Reveals the Secrets, Tips, and Techniques of How Clients Become MillionairesNessuna valutazione finora

- Your Financial: Take The 31 - Day Fix Your Finances ChallengeDocumento4 pagineYour Financial: Take The 31 - Day Fix Your Finances ChallengepetravanderbruggenNessuna valutazione finora

- Credit Score: The Beginners Guide for Building, Repairing, Raising and Maintaining a Good Credit Score. Includes a Step-by-Step Program to Improve and Boost Your Bank Rating.Da EverandCredit Score: The Beginners Guide for Building, Repairing, Raising and Maintaining a Good Credit Score. Includes a Step-by-Step Program to Improve and Boost Your Bank Rating.Nessuna valutazione finora

- Omni Consulting Firm Credit Course Book: For Class or Stand Only Users - Profitable for AllDa EverandOmni Consulting Firm Credit Course Book: For Class or Stand Only Users - Profitable for AllNessuna valutazione finora

- Smart Home Tips: Credit, Money, Budget, Debt, Payday LoansDa EverandSmart Home Tips: Credit, Money, Budget, Debt, Payday LoansValutazione: 5 su 5 stelle5/5 (1)

- Quicken Refiguide NCDocumento11 pagineQuicken Refiguide NCthelawmanNessuna valutazione finora

- Best Debt Elimination Plan: Debt Management Strategies that Get You Out of Debt Quickly and Economically: Becoming Financially Independent, #1Da EverandBest Debt Elimination Plan: Debt Management Strategies that Get You Out of Debt Quickly and Economically: Becoming Financially Independent, #1Valutazione: 5 su 5 stelle5/5 (1)

- The Charles Schwab Guide To Finances After Fifty: Answers To Your Most Important Money QuestionsDocumento12 pagineThe Charles Schwab Guide To Finances After Fifty: Answers To Your Most Important Money QuestionsCrown Publishing Group0% (1)

- Credit Score SecretsDocumento73 pagineCredit Score SecretsVijaya Bhasker100% (1)

- Debt Free For LifeDocumento3 pagineDebt Free For LifeAhmed RazaNessuna valutazione finora

- Is Your Mortgage Tax Deductible?: 8 Things You Need To Know Before Implementing The Smith ManoeuvreDocumento8 pagineIs Your Mortgage Tax Deductible?: 8 Things You Need To Know Before Implementing The Smith ManoeuvreHarshalNessuna valutazione finora

- Credit Repair Guide: Restore Your Credit RatingDocumento28 pagineCredit Repair Guide: Restore Your Credit RatingWill Crawford0% (1)

- The Essential Guide To: Understanding DebtDocumento5 pagineThe Essential Guide To: Understanding DebtrubenNessuna valutazione finora

- Your Credit Your Home Your FutureDocumento86 pagineYour Credit Your Home Your FutureTim LaneNessuna valutazione finora

- Mod 1 Fundamentals of Personal FinanceDocumento15 pagineMod 1 Fundamentals of Personal FinanceShruti b ahujaNessuna valutazione finora

- Combine PDFDocumento70 pagineCombine PDFIulian RoșuNessuna valutazione finora

- Debt Free For LifeDocumento9 pagineDebt Free For LifeTim JoyceNessuna valutazione finora

- No More Debts: A Handy Guide With 6 Effective Tips To Be Debt-Free & Saving Up MoneyDa EverandNo More Debts: A Handy Guide With 6 Effective Tips To Be Debt-Free & Saving Up MoneyNessuna valutazione finora

- 3 simple steps become richer by next DiwaliDocumento4 pagine3 simple steps become richer by next DiwaliSurapaneni RishiNessuna valutazione finora

- Legacy: The Fundamental Principals of Family & Financial PlanningDa EverandLegacy: The Fundamental Principals of Family & Financial PlanningNessuna valutazione finora

- Assignment in Personal Finances LAGMAY EFRELYNDocumento2 pagineAssignment in Personal Finances LAGMAY EFRELYNEfrelyn LagmayNessuna valutazione finora

- The Debtinator: A Step-By-Step System to Eliminate Your DebtDa EverandThe Debtinator: A Step-By-Step System to Eliminate Your DebtNessuna valutazione finora

- FinanceDocumento17 pagineFinanceapi-375296128Nessuna valutazione finora

- Extending Your Runway: Ravi Gupta & Sonya Huang May 2022Documento24 pagineExtending Your Runway: Ravi Gupta & Sonya Huang May 2022raiutkarshNessuna valutazione finora

- Start To Manage and Control Your Personal Finance! Effective Advice to Finally Help You Take Control of Your Personal Finances!Da EverandStart To Manage and Control Your Personal Finance! Effective Advice to Finally Help You Take Control of Your Personal Finances!Nessuna valutazione finora

- Credit Make OverDocumento79 pagineCredit Make Overnewent772050% (2)

- Stop the Insanity: Success Strategies for Credit RepairDa EverandStop the Insanity: Success Strategies for Credit RepairNessuna valutazione finora

- The 250 Personal Finance Questions You Should Ask in Your 20s and 30sDa EverandThe 250 Personal Finance Questions You Should Ask in Your 20s and 30sValutazione: 3 su 5 stelle3/5 (1)

- Millennial PlaybookDocumento186 pagineMillennial PlaybookBrian JonesNessuna valutazione finora

- RPG Ebook Successful Property Investing 2023 1 PDFDocumento85 pagineRPG Ebook Successful Property Investing 2023 1 PDFkiminNessuna valutazione finora

- Financial Basics: 1. Make A Financial CalendarDocumento4 pagineFinancial Basics: 1. Make A Financial CalendarAngie WandyNessuna valutazione finora

- HowMoneyWorks 2Documento32 pagineHowMoneyWorks 2xeff blackNessuna valutazione finora

- 20 Tips For Getting Out of Debt NowDocumento6 pagine20 Tips For Getting Out of Debt NowRex RossNessuna valutazione finora

- Tiaa StrategiesDocumento20 pagineTiaa Strategiesjohap7Nessuna valutazione finora

- 4 Managing Debts Effectively PDFDocumento48 pagine4 Managing Debts Effectively PDFLawrence CezarNessuna valutazione finora

- Find Your Cash: How to find $100k extra cash in your business in the next 12 monthsDa EverandFind Your Cash: How to find $100k extra cash in your business in the next 12 monthsNessuna valutazione finora

- RetireJapan 10 Steps PDF SM UnknownDocumento14 pagineRetireJapan 10 Steps PDF SM Unknownmclaird01Nessuna valutazione finora

- Personal FinanceDocumento24 paginePersonal FinanceKirosTeklehaimanotNessuna valutazione finora

- How Canadians Can Get out of Debt and Save MoneyDa EverandHow Canadians Can Get out of Debt and Save MoneyNessuna valutazione finora

- Hidden Credit Repair Secrets: How to Fix Your Credit Score and Boost it to 720+ with Credit Repair Secrets: Change Your Financial Life. Protect and Manage Your Business, Your Money and Enjoy FreedomDa EverandHidden Credit Repair Secrets: How to Fix Your Credit Score and Boost it to 720+ with Credit Repair Secrets: Change Your Financial Life. Protect and Manage Your Business, Your Money and Enjoy FreedomNessuna valutazione finora

- 10 Questions About Money That You'Re Afraid To AsDocumento2 pagine10 Questions About Money That You'Re Afraid To AsMark LabramonteNessuna valutazione finora

- Financial Literacy-Middle School 13-PresenationDocumento31 pagineFinancial Literacy-Middle School 13-PresenationRodel floresNessuna valutazione finora

- How To Pay Off Your Mortgage in 5 YearsDa EverandHow To Pay Off Your Mortgage in 5 YearsValutazione: 4.5 su 5 stelle4.5/5 (6)

- Are You: Credit WiseDocumento32 pagineAre You: Credit Wisebesis111Nessuna valutazione finora

- Lootcamp: 4 Weeks to Reducing Debt and Increasing Your Financial FitnessDa EverandLootcamp: 4 Weeks to Reducing Debt and Increasing Your Financial FitnessValutazione: 4 su 5 stelle4/5 (1)

- A Smart Guide to Building Wealth: Money Moves Your Parents Wish They Had MadeDa EverandA Smart Guide to Building Wealth: Money Moves Your Parents Wish They Had MadeNessuna valutazione finora

- The Total Money Makeover by Dave Ramsey: Summary and AnalysisDa EverandThe Total Money Makeover by Dave Ramsey: Summary and AnalysisValutazione: 4.5 su 5 stelle4.5/5 (7)

- 5 Remarkable Steps to Financial FreedomDa Everand5 Remarkable Steps to Financial FreedomNessuna valutazione finora

- Your Road Map To Financial Freedom 101Documento14 pagineYour Road Map To Financial Freedom 101Samuel TeddyNessuna valutazione finora

- The Credit-Building Game: The Simple Blueprint for Building CreditDa EverandThe Credit-Building Game: The Simple Blueprint for Building CreditNessuna valutazione finora

- BIFFPP-Step 4 CPA BermudaDocumento6 pagineBIFFPP-Step 4 CPA BermudaRG-eviewerNessuna valutazione finora

- DebtFreeSecrets+V1 1Documento45 pagineDebtFreeSecrets+V1 1Raul Fraul100% (1)

- Velocity Banking - The Debt Free SecretDocumento27 pagineVelocity Banking - The Debt Free SecretsjjhalaNessuna valutazione finora

- Sequoia Capital Report ??Documento24 pagineSequoia Capital Report ??Soham SubhamNessuna valutazione finora

- Transportation Research Part E: Indranil Biswas, Alok Raj, Samir K. SrivastavaDocumento14 pagineTransportation Research Part E: Indranil Biswas, Alok Raj, Samir K. SrivastavaItalo ViracochaNessuna valutazione finora

- Framing The Triple Bottom Line Approach Direct and Mediation Effects Between Economic, Social and Environmental ElementsDocumento20 pagineFraming The Triple Bottom Line Approach Direct and Mediation Effects Between Economic, Social and Environmental ElementsPaulo de CastroNessuna valutazione finora

- Why You Must Mind The Gaap: A Single Accounting, Tax Filing, and Payroll Solution For BusinessesDocumento14 pagineWhy You Must Mind The Gaap: A Single Accounting, Tax Filing, and Payroll Solution For BusinessesPaulo de CastroNessuna valutazione finora

- Infinitive and verb forms in Portuguese and EnglishDocumento7 pagineInfinitive and verb forms in Portuguese and EnglishPaulo de CastroNessuna valutazione finora

- Applied Mathematical Modelling: Payman Ahi, Cory SearcyDocumento15 pagineApplied Mathematical Modelling: Payman Ahi, Cory SearcyJanriggs RodriguezNessuna valutazione finora

- Word OrderDocumento4 pagineWord OrderPaulo de CastroNessuna valutazione finora

- Puzzle words and definitionsDocumento1 paginaPuzzle words and definitionsPaulo de CastroNessuna valutazione finora

- THE Triple Bottom Line Reporting - Corporate ResponsibilityDocumento17 pagineTHE Triple Bottom Line Reporting - Corporate ResponsibilityPaulo de CastroNessuna valutazione finora

- Insights Into The TBL The Case of LibanoDocumento13 pagineInsights Into The TBL The Case of LibanoPaulo de CastroNessuna valutazione finora

- Regras de Plural - BásicoDocumento1 paginaRegras de Plural - BásicoPaulo de CastroNessuna valutazione finora

- Sentence Structure PDFDocumento7 pagineSentence Structure PDFPaulo de CastroNessuna valutazione finora

- 100 Sales Tips For 2017Documento52 pagine100 Sales Tips For 2017Paulo de Castro100% (1)

- Verb Tenses - Short Text AnalysisDocumento15 pagineVerb Tenses - Short Text AnalysisPaulo de CastroNessuna valutazione finora

- YC Seed Deck Template PDFDocumento11 pagineYC Seed Deck Template PDFPaulo de CastroNessuna valutazione finora

- Sustainable Entrepreneurship - Journal of Business EthicsDocumento23 pagineSustainable Entrepreneurship - Journal of Business EthicsPaulo de CastroNessuna valutazione finora

- Personal Pronouns - Exercise With AnswersDocumento10 paginePersonal Pronouns - Exercise With AnswersPaulo de CastroNessuna valutazione finora

- Social Entrepreneurship EducationDocumento12 pagineSocial Entrepreneurship EducationPaulo de CastroNessuna valutazione finora

- Verb To PreferDocumento25 pagineVerb To PreferPaulo de CastroNessuna valutazione finora

- Coal Mining VocabularyDocumento2 pagineCoal Mining VocabularyPaulo de CastroNessuna valutazione finora

- Video - The Art of Debate - Never Lose An Argument AgainDocumento13 pagineVideo - The Art of Debate - Never Lose An Argument AgainPaulo de CastroNessuna valutazione finora

- TutankhamunDocumento1 paginaTutankhamunPaulo de CastroNessuna valutazione finora

- A Complexity View of Industry 4.0Documento12 pagineA Complexity View of Industry 4.0Paulo de CastroNessuna valutazione finora

- Pronouns ChartDocumento5 paginePronouns ChartPaulo de CastroNessuna valutazione finora

- Passado Simples - Exercícios Gerais 4Documento5 paginePassado Simples - Exercícios Gerais 4Paulo de CastroNessuna valutazione finora

- Action Noun Collocation CrosswordDocumento1 paginaAction Noun Collocation CrosswordGonzalo RochaNessuna valutazione finora

- Infinitive and verb forms in Portuguese and EnglishDocumento7 pagineInfinitive and verb forms in Portuguese and EnglishPaulo de CastroNessuna valutazione finora

- Passado Simples - Texto e PerguntasDocumento1 paginaPassado Simples - Texto e PerguntasPaulo de CastroNessuna valutazione finora

- Bail Out NytDocumento1 paginaBail Out NytPaulo de CastroNessuna valutazione finora

- QuestionsDocumento6 pagineQuestionsPaulo de CastroNessuna valutazione finora

- The Sentence: Sentence Structure: 1. Affirmative 2. Interrogative 3. NegativeDocumento7 pagineThe Sentence: Sentence Structure: 1. Affirmative 2. Interrogative 3. NegativePaulo de CastroNessuna valutazione finora

- Internet Banking in SBIDocumento66 pagineInternet Banking in SBIsejal kasalkar50% (2)

- MAE by Maybank2u: Frequently Asked QuestionsDocumento40 pagineMAE by Maybank2u: Frequently Asked Questionslim wey songNessuna valutazione finora

- Cesu BillDocumento1 paginaCesu BillPunyesh KumarNessuna valutazione finora

- NRI BankingDocumento4 pagineNRI Bankingjayanti kappalNessuna valutazione finora

- AWS TECHNOLOGIES: E-Payment Solutions for KSA BusinessesDocumento15 pagineAWS TECHNOLOGIES: E-Payment Solutions for KSA BusinessesMuhammad WaqasNessuna valutazione finora

- Acct Statement XX2182 29082021Documento28 pagineAcct Statement XX2182 29082021Sunil VishwakarmaNessuna valutazione finora

- Agentes Autorizados ETF Site 05out21Documento5 pagineAgentes Autorizados ETF Site 05out21Daniel EliasNessuna valutazione finora

- International PaymentDocumento15 pagineInternational PaymentPooja JaiswalNessuna valutazione finora

- Hkex New Entrusted Loan Arrangement 信达国际Documento9 pagineHkex New Entrusted Loan Arrangement 信达国际Martin JpNessuna valutazione finora

- Ibs Port Klang 1 31/10/23Documento11 pagineIbs Port Klang 1 31/10/23iemaqeelnasNessuna valutazione finora

- Mortgage Letter 2010-14Documento3 pagineMortgage Letter 2010-14YuriNessuna valutazione finora

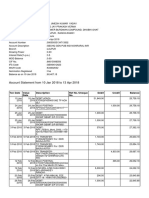

- Account Statement From 10 Jan 2018 To 13 Apr 2018Documento3 pagineAccount Statement From 10 Jan 2018 To 13 Apr 2018UMESH KUMAR YadavNessuna valutazione finora

- Private Banking DetailsDocumento7 paginePrivate Banking Detailsraj221Nessuna valutazione finora

- Estafa case resolutionDocumento3 pagineEstafa case resolutionJhudith De Julio BuhayNessuna valutazione finora

- Education Loan of Sbi BankDocumento52 pagineEducation Loan of Sbi BankRahul SanasNessuna valutazione finora

- Appropriation of Payments by BanksDocumento13 pagineAppropriation of Payments by BanksMALKANI DISHA DEEPAKNessuna valutazione finora

- GB30703 Group AssignmentDocumento2 pagineGB30703 Group AssignmentMarch ClaNessuna valutazione finora

- Challan FormDocumento2 pagineChallan FormKarunakara CheerlaNessuna valutazione finora

- Back To Back LCDocumento1 paginaBack To Back LCJayant Nair0% (1)

- Principles of Finance for Business LeadersDocumento28 paginePrinciples of Finance for Business LeadersYannah HidalgoNessuna valutazione finora

- Noc From BLDRDocumento3 pagineNoc From BLDRsameersbnNessuna valutazione finora

- Audit of Cash and Cash Equivalents Internal ControlsDocumento7 pagineAudit of Cash and Cash Equivalents Internal ControlsRNessuna valutazione finora

- Customer Satisfaction with HSBC ATM ServicesDocumento19 pagineCustomer Satisfaction with HSBC ATM Servicesnamnh0307Nessuna valutazione finora

- Union Bank of India Credit Card Payment Through UpiDocumento2 pagineUnion Bank of India Credit Card Payment Through Upisateesh008Nessuna valutazione finora

- ) ) @Ç!!'b!!!!-%eM!r : This Bill $75.90 Previous Balance - $9.40 TotalDocumento5 pagine) ) @Ç!!'b!!!!-%eM!r : This Bill $75.90 Previous Balance - $9.40 Totalmark samoNessuna valutazione finora

- Financial Inclusion Strategy of The Timor-Leste GovernmentDocumento140 pagineFinancial Inclusion Strategy of The Timor-Leste GovernmentPapers and Powerpoints from UNTL-VU Joint Conferenes in DiliNessuna valutazione finora

- Numerical On Credit RiskDocumento4 pagineNumerical On Credit RiskLeo SaimNessuna valutazione finora

- KVB 753Documento14 pagineKVB 753ManikandanNessuna valutazione finora

- TVM Problems: Calculating Present & Future Values of Annuities, Loans, InvestmentsDocumento2 pagineTVM Problems: Calculating Present & Future Values of Annuities, Loans, InvestmentsKhondaker RafsanjaniNessuna valutazione finora

- What Is Basel III and Overview of Basel Framework in PakistanDocumento4 pagineWhat Is Basel III and Overview of Basel Framework in PakistanSayyam KhanNessuna valutazione finora