Potrebbero piacerti anche

- The Impact of Web 2.0 & E 2.0Documento26 pagineThe Impact of Web 2.0 & E 2.0wchuckiNessuna valutazione finora

- Interactive TV: TV Trends iTV Core Concepts iTV Applications iTV Technologies iTV Revenue Models Itv R&DDocumento72 pagineInteractive TV: TV Trends iTV Core Concepts iTV Applications iTV Technologies iTV Revenue Models Itv R&DSam TripathiNessuna valutazione finora

- Next Generation IPTV Services and TechnologiesDa EverandNext Generation IPTV Services and TechnologiesValutazione: 5 su 5 stelle5/5 (1)

- GPON Customer PresentationDocumento36 pagineGPON Customer PresentationChesco Lopez Conde100% (1)

- Sofia Digital Whitepaper DVB RGBDocumento16 pagineSofia Digital Whitepaper DVB RGBKhushbooNessuna valutazione finora

- User Interface Development For Interactive Television: Extending A Commercialdtv Platform To The VirtualchannelapiDocumento10 pagineUser Interface Development For Interactive Television: Extending A Commercialdtv Platform To The VirtualchannelapiEndless SummerNessuna valutazione finora

- Television Industry: in NigeriaDocumento17 pagineTelevision Industry: in NigeriaX WriterNessuna valutazione finora

- TiVo Case Analysis Marketing HBSDocumento9 pagineTiVo Case Analysis Marketing HBSmahtaabk100% (1)

- What Content Providers Need To Know About... : Ott MonitoringDocumento2 pagineWhat Content Providers Need To Know About... : Ott MonitoringNazuk KabraNessuna valutazione finora

- 2) Session 2 PDFDocumento21 pagine2) Session 2 PDFAmit RajNessuna valutazione finora

- Standards For Ott: Bringing Order To Chaos: September 2019Documento16 pagineStandards For Ott: Bringing Order To Chaos: September 2019guillermo ceballosNessuna valutazione finora

- AppsFlyer OTT GuideDocumento27 pagineAppsFlyer OTT GuideNikhil DintakurthiNessuna valutazione finora

- IPTV Over Cable: Ariel SzternbergDocumento56 pagineIPTV Over Cable: Ariel SzternbergVlad BerNessuna valutazione finora

- Methods and Applications in Interactive BroadcastingDocumento8 pagineMethods and Applications in Interactive BroadcastingEndless SummerNessuna valutazione finora

- Tivo:: A Case Study OnDocumento11 pagineTivo:: A Case Study OnNg Eng ChongNessuna valutazione finora

- Hotstar Capstone ProjectDocumento19 pagineHotstar Capstone Projectkartik mathurNessuna valutazione finora

- MohanDocumento31 pagineMohanJenylen Tajanlangit-CabisoNessuna valutazione finora

- Ppt. Marketing of Media ServicesDocumento96 paginePpt. Marketing of Media ServicesANJUM ASHRI100% (1)

- If You Stream It, Will They Watch?Documento34 pagineIf You Stream It, Will They Watch?FaizahKadirNessuna valutazione finora

- Emtk Pubex 2020Documento29 pagineEmtk Pubex 2020cctv aldodiNessuna valutazione finora

- Pure Live 2018 Screen 0 PDFDocumento99 paginePure Live 2018 Screen 0 PDFGoeorge CoffinetNessuna valutazione finora

- IPTV Internet Video ABEGEN PDFDocumento100 pagineIPTV Internet Video ABEGEN PDFFaizahKadirNessuna valutazione finora

- Evolution of TV 7 Dynamics Transforming TV ArticlesDocumento19 pagineEvolution of TV 7 Dynamics Transforming TV ArticlesVanessa FonsecaNessuna valutazione finora

- Eng TELE-satellite 1007Documento132 pagineEng TELE-satellite 1007Alexander WieseNessuna valutazione finora

- D20O 2013 BeeSmart KKDocumento2 pagineD20O 2013 BeeSmart KKJasman MaulanaNessuna valutazione finora

- Eng TELE-satellite 1103Documento164 pagineEng TELE-satellite 1103Alexander WieseNessuna valutazione finora

- Internet Protocol Television Seminar ReportDocumento34 pagineInternet Protocol Television Seminar Reporttripsabhi08100% (5)

- Veselinovska 2014Documento6 pagineVeselinovska 2014dario97satanNessuna valutazione finora

- By Group 10 - Section BDocumento15 pagineBy Group 10 - Section Bshubham jainNessuna valutazione finora

- Emerging Technology Iptv: Project Report OnDocumento16 pagineEmerging Technology Iptv: Project Report OnNaveen KumarNessuna valutazione finora

- DTH War in IndiaDocumento17 pagineDTH War in IndiaKavita BaeetNessuna valutazione finora

- R Rep BT.2447 2019 PDF eDocumento22 pagineR Rep BT.2447 2019 PDF eYisäk DesälegnNessuna valutazione finora

- EMTK - Public Expose 2021Documento30 pagineEMTK - Public Expose 2021Darwin TjongNessuna valutazione finora

- ABCDocumento22 pagineABCSanchit GargNessuna valutazione finora

- White Paper: An Introduction To IPTVDocumento11 pagineWhite Paper: An Introduction To IPTVCindy MaldonadoNessuna valutazione finora

- Keynote MaterialDocumento21 pagineKeynote Materialsvasanth1Nessuna valutazione finora

- Accenture Bringing TV To LifeDocumento11 pagineAccenture Bringing TV To LifemscallonNessuna valutazione finora

- IAB UK Changing The Channel - A PDFDocumento44 pagineIAB UK Changing The Channel - A PDFacdesai100% (1)

- Internet Protocol Television: A Project Report OnDocumento33 pagineInternet Protocol Television: A Project Report OnAkash KhandelwalNessuna valutazione finora

- SectionA - Group3 - Tivo in 2002Documento26 pagineSectionA - Group3 - Tivo in 2002shreyanshagrawalNessuna valutazione finora

- 06 RadioDNS NickDocumento40 pagine06 RadioDNS Nickjose medina gordilloNessuna valutazione finora

- EE6364 Iptv Network Design: Presented By: Dhvanit Dave Dileep Sandipan Pratik Shedge Uday Mali Reddy Venkata DuggishettyDocumento22 pagineEE6364 Iptv Network Design: Presented By: Dhvanit Dave Dileep Sandipan Pratik Shedge Uday Mali Reddy Venkata DuggishettyJatin JoshuaNessuna valutazione finora

- 2021 - A New Era in Broadcast TV - The Media SchoolsDocumento9 pagine2021 - A New Era in Broadcast TV - The Media Schoolsakinlabi aderibigbeNessuna valutazione finora

- IP-to-TV Video Calling: Trends and Best Practices For IP and Mobile Video Calls BroadcastingDocumento7 pagineIP-to-TV Video Calling: Trends and Best Practices For IP and Mobile Video Calls BroadcastingNizamuddin KaziNessuna valutazione finora

- Presentacion FTTRDocumento12 paginePresentacion FTTRpaulinosoNessuna valutazione finora

- A Dive Into IPTVDocumento6 pagineA Dive Into IPTVM-soft solutionsNessuna valutazione finora

- Tutorial On IPTV and Its Latest Developments: January 2011Documento7 pagineTutorial On IPTV and Its Latest Developments: January 2011Ermin SehicNessuna valutazione finora

- Tutorial On IPTV and Its Latest Developments: January 2011Documento7 pagineTutorial On IPTV and Its Latest Developments: January 2011Demandas SanchezabogadosNessuna valutazione finora

- HBBTV WhitepaperDocumento10 pagineHBBTV WhitepaperrahulkingerNessuna valutazione finora

- Current Trends in Indian TelevisionDocumento8 pagineCurrent Trends in Indian Televisionthe_f0rsak3nNessuna valutazione finora

- Tutorial On IPTV and Its Latest Developments: January 2011Documento7 pagineTutorial On IPTV and Its Latest Developments: January 2011Andri JunaediNessuna valutazione finora

- Tutorial On IPTV and Its Latest Developments: January 2011Documento7 pagineTutorial On IPTV and Its Latest Developments: January 2011Eyob AberaNessuna valutazione finora

- Trends in TVDocumento6 pagineTrends in TVprasenkarNessuna valutazione finora

- Tutorial On IPTV and Its Latest Developments: January 2011Documento7 pagineTutorial On IPTV and Its Latest Developments: January 2011Prasad RaoNessuna valutazione finora

- Title : Internet Protocol TelevisionDocumento4 pagineTitle : Internet Protocol TelevisionHiren ChawdaNessuna valutazione finora

- Iptv EditedDocumento28 pagineIptv EditedSphurthi RaoNessuna valutazione finora

- IPTV PresDocumento23 pagineIPTV PresIshu SinglaNessuna valutazione finora

- IPTVPaperDocumento6 pagineIPTVPaperHaitham FouratiNessuna valutazione finora

- JVL Annual Report - 2018-19Documento124 pagineJVL Annual Report - 2018-19Sanjay BhoirNessuna valutazione finora

- Curefit Financials FY19Documento5 pagineCurefit Financials FY19Sanjay BhoirNessuna valutazione finora

- Food and Nutrition Security Analysis IndiaDocumento254 pagineFood and Nutrition Security Analysis IndiaSanjay BhoirNessuna valutazione finora

- The Enchanted Wood by Enid Blyton PDFDocumento5 pagineThe Enchanted Wood by Enid Blyton PDFSanjay BhoirNessuna valutazione finora

- Evolution of Set Top Box DataDocumento27 pagineEvolution of Set Top Box DataSanjay BhoirNessuna valutazione finora

- Sponsormap Sponsorship Research & Roi PDFDocumento50 pagineSponsormap Sponsorship Research & Roi PDFSanjay BhoirNessuna valutazione finora

- History - of - Sports & Ent MKTGDocumento123 pagineHistory - of - Sports & Ent MKTGSanjay BhoirNessuna valutazione finora

- Amazon Approach To SegmentationDocumento8 pagineAmazon Approach To SegmentationSanjay BhoirNessuna valutazione finora

- BBC World News Audience SegmentationDocumento8 pagineBBC World News Audience SegmentationSanjay BhoirNessuna valutazione finora

- GE's Olympic SponsorshipDocumento33 pagineGE's Olympic SponsorshipSanjay BhoirNessuna valutazione finora

- DMA 2010-Statistical-Fact-Book PDFDocumento123 pagineDMA 2010-Statistical-Fact-Book PDFSanjay BhoirNessuna valutazione finora

- Deloitte Tech Med Telecompredcns 2015Documento76 pagineDeloitte Tech Med Telecompredcns 2015Sanjay BhoirNessuna valutazione finora

- How To Grow Radio Station AudiencesDocumento11 pagineHow To Grow Radio Station AudiencesSanjay Bhoir100% (1)

- Moles MeaningDocumento16 pagineMoles MeaningSanjay Bhoir100% (1)

- Film Language - Christian MetzDocumento12 pagineFilm Language - Christian MetzragatasuryaNessuna valutazione finora

- Subject Form Time Content StandardDocumento2 pagineSubject Form Time Content StandardlizandrewNessuna valutazione finora

- 29.principles of Teaching, Steps in Extension Teaching.Documento5 pagine29.principles of Teaching, Steps in Extension Teaching.Barathraj D18100% (1)

- Write An Essay Expressing Your Opinion On This Matter of Not Allowing Students To Bring Mobile Phones To SchoolDocumento2 pagineWrite An Essay Expressing Your Opinion On This Matter of Not Allowing Students To Bring Mobile Phones To SchoolOscar TeohNessuna valutazione finora

- Lesson Plan: Stages of THE Lesson Time Teacher'S and Pupils'Activities Interaction Materials and Aids SkillsDocumento5 pagineLesson Plan: Stages of THE Lesson Time Teacher'S and Pupils'Activities Interaction Materials and Aids SkillsMaricela TopaleaNessuna valutazione finora

- Types of WikiDocumento6 pagineTypes of WikimadellNessuna valutazione finora

- Training MethodsDocumento14 pagineTraining MethodsParita Vekaria100% (1)

- Canvas Role PermissionsDocumento1 paginaCanvas Role PermissionsJohnNessuna valutazione finora

- Fiona Erickson's ResumeDocumento1 paginaFiona Erickson's ResumefionaericksonNessuna valutazione finora

- Judge The Relevance and Worth of Ideas DAY 2Documento17 pagineJudge The Relevance and Worth of Ideas DAY 2Angela Grace TrinidadNessuna valutazione finora

- Free Student Planner Undated Calendar Girly GirlDocumento13 pagineFree Student Planner Undated Calendar Girly GirlDragomir Isabella100% (1)

- The Mass Media and PoliticsDocumento2 pagineThe Mass Media and PoliticsНаталія ЯкубецьNessuna valutazione finora

- DEMAND GENERATORS - REVISEdDocumento2 pagineDEMAND GENERATORS - REVISEdJenny Pearl PerezNessuna valutazione finora

- Now and Get: Best VTU Student Companion You Can GetDocumento5 pagineNow and Get: Best VTU Student Companion You Can GetSriram NatarajanNessuna valutazione finora

- How To Read An Engineering Research PaperDocumento4 pagineHow To Read An Engineering Research PaperJulian MartinezNessuna valutazione finora

- Must Win BattlesDocumento117 pagineMust Win Battlesramasalim100% (4)

- Error AnalysisDocumento7 pagineError AnalysisAbby OjalesNessuna valutazione finora

- Midterm Module For EnglishDocumento42 pagineMidterm Module For EnglishMarie ShaneNessuna valutazione finora

- Huawei Drive Test Solution V1 0 20110824Documento26 pagineHuawei Drive Test Solution V1 0 20110824jaymart lunaNessuna valutazione finora

- Lan Wan ArchitectureDocumento60 pagineLan Wan ArchitectureBilly TierraNessuna valutazione finora

- Odoo Connect 2019 - Exhibitors GuideDocumento8 pagineOdoo Connect 2019 - Exhibitors GuideS ANessuna valutazione finora

- Writing For Impact 3a-4b (With Key)Documento49 pagineWriting For Impact 3a-4b (With Key)Tâm Lê Văn50% (2)

- SBLE3123 English Profiency IIIDocumento11 pagineSBLE3123 English Profiency IIINur Solehah OthmanNessuna valutazione finora

- Guidelines UMBC PortfolioDocumento5 pagineGuidelines UMBC PortfolioNaaman Ty BrownNessuna valutazione finora

- Digital Communications: Chapter 1. IntroductionDocumento22 pagineDigital Communications: Chapter 1. IntroductionAhmedsadatNessuna valutazione finora

- Aviation MX HF Newsletter March 2020Documento13 pagineAviation MX HF Newsletter March 2020Wilson BenincoreNessuna valutazione finora

- Lexical Relations: Entailment Paraphrase ContradictionDocumento8 pagineLexical Relations: Entailment Paraphrase ContradictionKhalid Minhas100% (1)

- Learners' Attitudes Towards Using Communicative Approach in Teaching English at Wolkite Yaberus Preparatory SchoolDocumento13 pagineLearners' Attitudes Towards Using Communicative Approach in Teaching English at Wolkite Yaberus Preparatory SchoolIJELS Research JournalNessuna valutazione finora

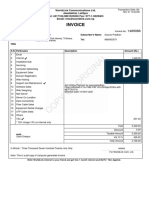

- Invoice: Worldlink Communications Ltd. Jawalakhel, Lalitpur Tel: 4217100,9801523050 Fax: 977-1-5529403Documento1 paginaInvoice: Worldlink Communications Ltd. Jawalakhel, Lalitpur Tel: 4217100,9801523050 Fax: 977-1-5529403Gaurav PradhanNessuna valutazione finora

- Approaches and Methods in Teaching Social Studies Unit 3Documento12 pagineApproaches and Methods in Teaching Social Studies Unit 3Karen SabateNessuna valutazione finora