Potrebbero piacerti anche

- CA Foundation Accounting SolutionsDocumento117 pagineCA Foundation Accounting SolutionsAkash AjayNessuna valutazione finora

- Tally Erp 9 Practise Set 1Documento28 pagineTally Erp 9 Practise Set 1Anusha ShettyNessuna valutazione finora

- Villamor FinalDocumento25 pagineVillamor FinalRinconada Benori ReynalynNessuna valutazione finora

- GST Entries For Every Month SalesDocumento3 pagineGST Entries For Every Month SalesGiri Sukumar100% (1)

- STUDY MATERIAL AccountingcomClass XIDocumento144 pagineSTUDY MATERIAL AccountingcomClass XImalathi SNessuna valutazione finora

- Index - Avatar The Word Master BookDocumento49 pagineIndex - Avatar The Word Master BookAlok Kumar100% (1)

- Sample Accounts ProblemsDocumento103 pagineSample Accounts ProblemsJayashree MaheshNessuna valutazione finora

- Tally AssignmentDocumento25 pagineTally AssignmentHimanshu YadavNessuna valutazione finora

- Journal Date Particulars L.F. Amt. (DR.) Amt. (CR.) : Solution Class 11 - Accountancy Test 2Documento9 pagineJournal Date Particulars L.F. Amt. (DR.) Amt. (CR.) : Solution Class 11 - Accountancy Test 2BHS PRAYAGRAJNessuna valutazione finora

- Basic Accounting Terms.1Documento5 pagineBasic Accounting Terms.1k srinivasNessuna valutazione finora

- Business Ledger Notes PDFDocumento16 pagineBusiness Ledger Notes PDFmark njeru ngigi100% (1)

- 100 Journal EntriesDocumento9 pagine100 Journal EntriesMajid JamilNessuna valutazione finora

- List of Ledgers: S.No Ledger Name Under: GroupDocumento5 pagineList of Ledgers: S.No Ledger Name Under: GroupSuraj KumarNessuna valutazione finora

- EnglishDocumento82 pagineEnglishMayaNessuna valutazione finora

- Six Day in Tally Class (What Is Ledger and How To Create Ledger in Tally)Documento9 pagineSix Day in Tally Class (What Is Ledger and How To Create Ledger in Tally)Kamlesh KumarNessuna valutazione finora

- Accountancy XiiDocumento122 pagineAccountancy XiiNancy Ekka100% (1)

- Tally Assignment Yash ComDocumento9 pagineTally Assignment Yash Comraj S.NNessuna valutazione finora

- Basics of Accounting - QBDocumento7 pagineBasics of Accounting - QBsujanthqatarNessuna valutazione finora

- FAA Ist AssignemntDocumento9 pagineFAA Ist AssignemntRameshNessuna valutazione finora

- Ledger Grouping in TAllyDocumento7 pagineLedger Grouping in TAllyramaNessuna valutazione finora

- Test 3Documento7 pagineTest 3info view0% (1)

- Tally Assignment With GSTDocumento28 pagineTally Assignment With GSTCoindcx SrkNessuna valutazione finora

- Journal EntriesDocumento61 pagineJournal EntriesTavnish Singh100% (1)

- Tally ProblemsDocumento9 pagineTally ProblemsM ZNessuna valutazione finora

- Accounting Entries Under GST For Different SituationsDocumento42 pagineAccounting Entries Under GST For Different Situationsamit chavariaNessuna valutazione finora

- Tally Module 1 Assignment SolutionDocumento6 pagineTally Module 1 Assignment Solutioncharu bishtNessuna valutazione finora

- AccountingDocumento437 pagineAccountingNeel Hati100% (1)

- CA Foundation Accounting Notes by Bharadwaj InstituteDocumento127 pagineCA Foundation Accounting Notes by Bharadwaj Institutenasiransar26Nessuna valutazione finora

- PEA305 WorkbookDocumento119 paginePEA305 Workbookbibajev147Nessuna valutazione finora

- GB Training & Placement Centre: Tally ERP 9 Certificate CourseDocumento2 pagineGB Training & Placement Centre: Tally ERP 9 Certificate CourseswayamNessuna valutazione finora

- Assignment 1 ACCOUNTANCYDocumento3 pagineAssignment 1 ACCOUNTANCYCHINMAY AGRAWALNessuna valutazione finora

- Worksheet Ledger and Trial BalanceDocumento4 pagineWorksheet Ledger and Trial BalanceRajni Sinha VermaNessuna valutazione finora

- Inter CA Direct Tax Homework SolutionsDocumento67 pagineInter CA Direct Tax Homework SolutionsAbhijit HoroNessuna valutazione finora

- Tally - Erp9: Free Online Computer Classes OnDocumento14 pagineTally - Erp9: Free Online Computer Classes OnAditya VermaNessuna valutazione finora

- Question 7Documento2 pagineQuestion 7abhishek georgeNessuna valutazione finora

- Problem 1Documento3 pagineProblem 1karthikeyan01Nessuna valutazione finora

- Tally Syllabus: 1. Basics of AccountingDocumento4 pagineTally Syllabus: 1. Basics of AccountingijrailNessuna valutazione finora

- Chapter 7 LedgerDocumento18 pagineChapter 7 LedgerJumayma Maryam100% (1)

- Accounting Equation Imp 1Documento5 pagineAccounting Equation Imp 1hiritik gupta100% (1)

- Index: S. NO. Page. NoDocumento728 pagineIndex: S. NO. Page. NoShruti RajNessuna valutazione finora

- 02D. Cma Inter Direct Tax Practice Test Series - Ay 2020-21Documento210 pagine02D. Cma Inter Direct Tax Practice Test Series - Ay 2020-21Himanshu RajNessuna valutazione finora

- Questions On Trial Balance To StudentsDocumento6 pagineQuestions On Trial Balance To Studentsveraji3735Nessuna valutazione finora

- FA1 General JournalDocumento5 pagineFA1 General JournalamirNessuna valutazione finora

- GST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyDa EverandGST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyValutazione: 5 su 5 stelle5/5 (1)

- 10 Illustration of Ledger 24.10.08Documento7 pagine10 Illustration of Ledger 24.10.08denish gandhi100% (1)

- NCERT Class 11 Accountancy Book (Part I)Documento288 pagineNCERT Class 11 Accountancy Book (Part I)Aashu DhalwalNessuna valutazione finora

- Multiple Choice Question Bank (MCQ) Term - I: Class - XIIDocumento59 pagineMultiple Choice Question Bank (MCQ) Term - I: Class - XIIDiya KhandelwalNessuna valutazione finora

- Tally Test: Kishan Lal SharmaDocumento4 pagineTally Test: Kishan Lal Sharmakhan patelNessuna valutazione finora

- Tally 036Documento191 pagineTally 036anjalishah7Nessuna valutazione finora

- General Journal: Date Description Debit CreditDocumento7 pagineGeneral Journal: Date Description Debit CreditAmanuel DemekeNessuna valutazione finora

- Extra Journal QuestionsDocumento3 pagineExtra Journal QuestionsMba BNessuna valutazione finora

- Prep Trading - Profit-And-Loss-Ac Balance SheetDocumento25 paginePrep Trading - Profit-And-Loss-Ac Balance Sheetfaltumail379100% (1)

- Exercises On Acc Eqn - 26 QuesDocumento12 pagineExercises On Acc Eqn - 26 QuesNeelu AggrawalNessuna valutazione finora

- Questions Journal, Ledger & TBDocumento9 pagineQuestions Journal, Ledger & TBHarsh GhaiNessuna valutazione finora

- Question Bank (Accounting Problems)Documento11 pagineQuestion Bank (Accounting Problems)Abhishek MohantyNessuna valutazione finora

- Accounting Imp 100 Q'sDocumento159 pagineAccounting Imp 100 Q'sVijayasri KumaravelNessuna valutazione finora

- Tally NotesDocumento25 pagineTally NotesBhanu SinghNessuna valutazione finora

- Tally - ERP9 Book With GSTDocumento1.843 pagineTally - ERP9 Book With GSThatimNessuna valutazione finora

- FoA I CH Two...Documento31 pagineFoA I CH Two...Ela Man ĤămměŕşNessuna valutazione finora

- Topic 3 - Recording Transactions (STU)Documento60 pagineTopic 3 - Recording Transactions (STU)thiennnannn45Nessuna valutazione finora

- X-Mas New Year: CelebrationsDocumento11 pagineX-Mas New Year: Celebrations1986anuNessuna valutazione finora

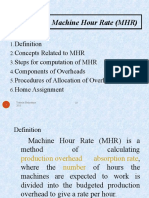

- Overhead - Machine Hour RateDocumento17 pagineOverhead - Machine Hour Rate1986anu100% (1)

- Grade 1 IMO in PDFDocumento11 pagineGrade 1 IMO in PDF1986anuNessuna valutazione finora

- Stress Management in The Context of Bhagavad-Gita: Dr. Kallave Maheshwar GangadharraoDocumento5 pagineStress Management in The Context of Bhagavad-Gita: Dr. Kallave Maheshwar Gangadharrao1986anuNessuna valutazione finora

- Day4 Residential Status and Incidence of Tax (9 Oct)Documento12 pagineDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNessuna valutazione finora

- 1st April NPV Vs IRRDocumento12 pagine1st April NPV Vs IRR1986anuNessuna valutazione finora

- 31st March Performance BudgetingDocumento13 pagine31st March Performance Budgeting1986anuNessuna valutazione finora

- Stress Management and GeetaDocumento5 pagineStress Management and Geeta1986anuNessuna valutazione finora

- (Book Chapter) Risk-Analysis-in-Capital-BudgetingDocumento49 pagine(Book Chapter) Risk-Analysis-in-Capital-Budgeting1986anu100% (2)

- Self ManagementDocumento22 pagineSelf Management1986anu83% (6)

- Chapter - I Mutual Funds in IndiaDocumento28 pagineChapter - I Mutual Funds in India1986anuNessuna valutazione finora

- Venture CapitalDocumento45 pagineVenture Capital1986anuNessuna valutazione finora

- Foreign BanksDocumento9 pagineForeign Banks1986anuNessuna valutazione finora

- Advance TaxDocumento2 pagineAdvance Tax1986anuNessuna valutazione finora

- Public Sector BanksDocumento1 paginaPublic Sector Banks1986anuNessuna valutazione finora

- Presented By:: Shubham Bhutada Aurangabad (MH)Documento30 paginePresented By:: Shubham Bhutada Aurangabad (MH)1986anu100% (1)

- Depository and Stock ExchangeDocumento22 pagineDepository and Stock Exchange1986anuNessuna valutazione finora

- QuestionnaireDocumento3 pagineQuestionnaire1986anuNessuna valutazione finora

- Inclusive GrowthDocumento8 pagineInclusive Growth1986anuNessuna valutazione finora

- Tugas ManPro Group 1Documento2 pagineTugas ManPro Group 1Salshadina SundariNessuna valutazione finora

- Group 7: Managing Risk and Reward in The Entrepreneurial VentureDocumento2 pagineGroup 7: Managing Risk and Reward in The Entrepreneurial VentureCONCORDIA RAFAEL IVANNessuna valutazione finora

- Lundin Oilgate War Crimes Carl Bildt (Company Propaganda)Documento108 pagineLundin Oilgate War Crimes Carl Bildt (Company Propaganda)mary engNessuna valutazione finora

- Bentley Haestad Solutions For Water Loss ControlDocumento2 pagineBentley Haestad Solutions For Water Loss ControlElena BucurașNessuna valutazione finora

- Impact of Startups On Local EconomyDocumento53 pagineImpact of Startups On Local Economyurbanaraquib05Nessuna valutazione finora

- Payment Gateway PlayerDocumento5 paginePayment Gateway PlayerHilmanie RamadhanNessuna valutazione finora

- Shapiro Chapter 20 SolutionsDocumento13 pagineShapiro Chapter 20 SolutionsRuiting ChenNessuna valutazione finora

- Preamble To Bill of QuantitiesDocumento1 paginaPreamble To Bill of QuantitiesAziz ul HakeemNessuna valutazione finora

- Product Launch Playbook EbookDocumento36 pagineProduct Launch Playbook EbookVăn Thịnh LêNessuna valutazione finora

- Business Sample LettersDocumento3 pagineBusiness Sample Lettersshaikat1009549Nessuna valutazione finora

- WEEK 1 - COVERAGE (Article 1767-1783 of The New Civil Code) : I. Contract of PartnershipDocumento3 pagineWEEK 1 - COVERAGE (Article 1767-1783 of The New Civil Code) : I. Contract of Partnershipcarl patNessuna valutazione finora

- Sub Order Labels 94ce8e7a 1b4d 4d5b Aac6 23950027e54dDocumento2 pagineSub Order Labels 94ce8e7a 1b4d 4d5b Aac6 23950027e54dDaryaee AhmedNessuna valutazione finora

- Team 2 CIA 2Documento12 pagineTeam 2 CIA 2Bhoomika BNessuna valutazione finora

- 21S1 AC1103 Lesson 03 Discussion QuestionsDocumento4 pagine21S1 AC1103 Lesson 03 Discussion Questionsxiu yingNessuna valutazione finora

- Important Questions - Income Tax PDFDocumento6 pagineImportant Questions - Income Tax PDFShourya RajputNessuna valutazione finora

- Digital Marketing Plan of Tesco PLCDocumento15 pagineDigital Marketing Plan of Tesco PLCMehwish Pervaiz100% (1)

- Chapter 8 and 9Documento3 pagineChapter 8 and 9Ajith GeorgeNessuna valutazione finora

- Cyber Security For Operational TechnologyDocumento2 pagineCyber Security For Operational TechnologyManikandan NadanasabapthyNessuna valutazione finora

- Administration & Logistic ManagerDocumento2 pagineAdministration & Logistic ManagerFahad KhanNessuna valutazione finora

- ITFG - Bulletin 9Documento7 pagineITFG - Bulletin 9TanviNessuna valutazione finora

- Go-To-Market Strategies - The Ultimate Playbook For Startup Expansion To International MarketsDocumento40 pagineGo-To-Market Strategies - The Ultimate Playbook For Startup Expansion To International MarketsLivia EllenNessuna valutazione finora

- Lokesh Punj Cvdec2018Documento11 pagineLokesh Punj Cvdec2018LOKESH PUNJNessuna valutazione finora

- Case w4 Walmart in JapanDocumento3 pagineCase w4 Walmart in JapanMohd Alif50% (2)

- Poe Imp - Question & Bit BankDocumento13 paginePoe Imp - Question & Bit BankPippalapalli IndrimaNessuna valutazione finora

- CA Foundation MTP 2020 Paper 1 AnsDocumento9 pagineCA Foundation MTP 2020 Paper 1 AnsSaurabh Kumar MauryaNessuna valutazione finora

- MN Updated Bank Contract 9.36Documento5 pagineMN Updated Bank Contract 9.36vqcheslav.karaNessuna valutazione finora

- 32704cadsxvc6970 Sample Data 100Documento6 pagine32704cadsxvc6970 Sample Data 100Nimbupani AdvertisersNessuna valutazione finora

- Model Exit Exam - Fundamentals of Accounting IDocumento9 pagineModel Exit Exam - Fundamentals of Accounting Inatnael0224Nessuna valutazione finora

- Marketing Plan AssignmentDocumento8 pagineMarketing Plan AssignmentAsad Ali khanNessuna valutazione finora

- PP Presentation Q 15 ADocumento8 paginePP Presentation Q 15 ARita LakhsmiNessuna valutazione finora