Potrebbero piacerti anche

- Sample of Motion For ReconsiderationDocumento2 pagineSample of Motion For ReconsiderationVinci Poncardas80% (5)

- Comparison Train Law and NircDocumento37 pagineComparison Train Law and Nircczabina fatima delica89% (19)

- Comparison Train Law and NircDocumento37 pagineComparison Train Law and Nircczabina fatima delica89% (19)

- Revenue Memorandum CIRCULAR NO. 51-2018Documento16 pagineRevenue Memorandum CIRCULAR NO. 51-2018Jastine BreatheNessuna valutazione finora

- Government Accounting ManualDocumento62 pagineGovernment Accounting ManualDez Za100% (1)

- Notice of Availment of Substituted Filing of Percentage Tax ReturnsDocumento1 paginaNotice of Availment of Substituted Filing of Percentage Tax ReturnsJomar TenezaNessuna valutazione finora

- Collection Procedures and Tax RemediesDocumento25 pagineCollection Procedures and Tax RemediesJobeLle MarquezNessuna valutazione finora

- 2307Documento2 pagine2307Nephy Bersales Taberara67% (3)

- Annex B-1 RR 11-2018 Sworn Statement of Declaration of Gross Sales and ReceiptsDocumento1 paginaAnnex B-1 RR 11-2018 Sworn Statement of Declaration of Gross Sales and ReceiptsEliza Corpuz Gadon89% (19)

- Appendix 65 - WMRDocumento1 paginaAppendix 65 - WMRJoe Jana Muchuelas BajaNessuna valutazione finora

- Boa Sworn Statement For AccreditationDocumento1 paginaBoa Sworn Statement For AccreditationBillcounterNessuna valutazione finora

- Landlord Tax Planning StrategiesDa EverandLandlord Tax Planning StrategiesNessuna valutazione finora

- Accruals and DeferralsDocumento2 pagineAccruals and DeferralsravisankarNessuna valutazione finora

- Sample Letter for Guest Lecturer Visit and HonorariumDocumento1 paginaSample Letter for Guest Lecturer Visit and HonorariumChristy Ledesma-NavarroNessuna valutazione finora

- Financials Setup GuideDocumento317 pagineFinancials Setup GuideAlberto Mario Delahoz OlacireguiNessuna valutazione finora

- BIR issues guidelines for nationwide evaluation of cash registersDocumento6 pagineBIR issues guidelines for nationwide evaluation of cash registersGil Pino0% (1)

- Form 0605 PDFDocumento2 pagineForm 0605 PDFeugene badereNessuna valutazione finora

- BIR Ruling No. 242-18 (Gift Certs.)Documento7 pagineBIR Ruling No. 242-18 (Gift Certs.)LizNessuna valutazione finora

- SAP MM Overview For TechnicalDocumento27 pagineSAP MM Overview For Technicalbakkali_bilalNessuna valutazione finora

- Audit Engagement LetterDocumento4 pagineAudit Engagement LetterJessicaGonzalesNessuna valutazione finora

- Additonal Disclosure RR 15 2010Documento5 pagineAdditonal Disclosure RR 15 2010Emil A. MolinaNessuna valutazione finora

- Mary Joy L. Amigos Rice Store Notes To The Financial StatementsDocumento5 pagineMary Joy L. Amigos Rice Store Notes To The Financial StatementsLizanne GauranaNessuna valutazione finora

- Income Payor DeclarationDocumento1 paginaIncome Payor DeclarationMahko albert RslesNessuna valutazione finora

- Year-End Tax Requirements and ProceduresDocumento164 pagineYear-End Tax Requirements and ProceduresDarioNessuna valutazione finora

- NFC July 2023 UpdatedDocumento3 pagineNFC July 2023 UpdatedMuhammad UsmanNessuna valutazione finora

- Annex B-2 RR 11-2018Documento1 paginaAnnex B-2 RR 11-2018Princess RegalaNessuna valutazione finora

- Revenue Regulations No. 2-98 Withholding Tax GuideDocumento16 pagineRevenue Regulations No. 2-98 Withholding Tax GuideLea Samantha GallardoNessuna valutazione finora

- PFF053 MembersContributionRemittanceForm V02-FillableDocumento2 paginePFF053 MembersContributionRemittanceForm V02-FillableCYvelle TorefielNessuna valutazione finora

- MC 2018-034 - Updated Guidelines On RATADocumento7 pagineMC 2018-034 - Updated Guidelines On RATAKarla KatigbakNessuna valutazione finora

- Annex B-2 RR 11-2018Documento1 paginaAnnex B-2 RR 11-2018Kristine JoyceNessuna valutazione finora

- BIR's Tax Ruling Process ExplainedDocumento3 pagineBIR's Tax Ruling Process ExplainedConnieAllanaMacapagaoNessuna valutazione finora

- Ra 7160 IrrDocumento263 pagineRa 7160 IrrAlvaro Garingo100% (21)

- E SalesDocumento58 pagineE Salesgrini gunayan50% (2)

- Bir RR No 2 2015 Annex CDocumento3 pagineBir RR No 2 2015 Annex CCupang West MPCNessuna valutazione finora

- How to File Form 2316, Annex C and Annex F by Feb. 28Documento4 pagineHow to File Form 2316, Annex C and Annex F by Feb. 28Ivan Benedicto100% (1)

- RR 2-98 Section 2.57 (B) - CWTDocumento3 pagineRR 2-98 Section 2.57 (B) - CWTZenaida LatorreNessuna valutazione finora

- 1601 CDocumento6 pagine1601 CJose Venturina Villacorta100% (1)

- Sworn Statement For Tax Clearance SampleDocumento1 paginaSworn Statement For Tax Clearance SampleRachel ChanNessuna valutazione finora

- COA M2014 013 CellcardDocumento2 pagineCOA M2014 013 CellcardRobehgene Atud-JavinarNessuna valutazione finora

- EFPS Letter of Intent SampleDocumento1 paginaEFPS Letter of Intent SampleBernardino PacificAceNessuna valutazione finora

- Expanded Withholding Taxes On Government Income PaymentsDocumento172 pagineExpanded Withholding Taxes On Government Income PaymentsBien Bowie A. CortezNessuna valutazione finora

- 1702 QDocumento3 pagine1702 Qappipinnim50% (2)

- Invoice Receipt For Property Form GF 30 A 2Documento1 paginaInvoice Receipt For Property Form GF 30 A 2Rexis ReginanNessuna valutazione finora

- Annex C RR 11-2018Documento1 paginaAnnex C RR 11-2018Rheneir MoraNessuna valutazione finora

- DOLE CS Form No. 212 Attachment Work Experience Sheet 1Documento2 pagineDOLE CS Form No. 212 Attachment Work Experience Sheet 1Danilo PateñoNessuna valutazione finora

- Appendix 49 - Instructions - RPPCVDocumento1 paginaAppendix 49 - Instructions - RPPCVCENTRAL OFFICE ACCOUNTINGNessuna valutazione finora

- Annex B-1 Guide, Instructions and Blank Copy: (Several Income Payors)Documento4 pagineAnnex B-1 Guide, Instructions and Blank Copy: (Several Income Payors)Kristel Anne LiwagNessuna valutazione finora

- 2019 Sec Clarifies Manner of Preparation and Filing of Afs Under The Revised Corporation CodeDocumento2 pagine2019 Sec Clarifies Manner of Preparation and Filing of Afs Under The Revised Corporation CodeAnne DomingoNessuna valutazione finora

- Bir Ruling (Da-031-07)Documento2 pagineBir Ruling (Da-031-07)Stacy Liong BloggerAccountNessuna valutazione finora

- Tax Update RR 18-2012Documento32 pagineTax Update RR 18-2012johamarz6245Nessuna valutazione finora

- Sworn Declaration BirDocumento1 paginaSworn Declaration Birynid wageNessuna valutazione finora

- 1702 NewDocumento11 pagine1702 NewDIVINE WAGTINGANNessuna valutazione finora

- EMELINO T MAESTRO BIR Ask For ReceiptDocumento1 paginaEMELINO T MAESTRO BIR Ask For Receiptjuliet_emelinotmaestroNessuna valutazione finora

- Annex DDocumento8 pagineAnnex DVicky Tamo-oNessuna valutazione finora

- Audit Report - TuburanDocumento87 pagineAudit Report - TuburanMaria100% (1)

- BIR Form 2316 UndertakingDocumento1 paginaBIR Form 2316 UndertakingJan Paolo CruzNessuna valutazione finora

- Certification Statement of Management's Responsibility (Itr)Documento1 paginaCertification Statement of Management's Responsibility (Itr)Earl Jhune Amoranto100% (1)

- BIR FORM 2307 SampleDocumento6 pagineBIR FORM 2307 SampleEasyHear Philippines by NuGen Hearing Devices, Inc.Nessuna valutazione finora

- Property transfer report summaryDocumento2 pagineProperty transfer report summaryCatherine BenbanNessuna valutazione finora

- Annex F RR 11-2018Documento1 paginaAnnex F RR 11-2018Gerynes Mae Bacarra100% (1)

- Pag-IBIG eSRS Guide for Small EmployersDocumento3 paginePag-IBIG eSRS Guide for Small EmployersJulio LuisNessuna valutazione finora

- 2307Documento3 pagine2307JUCONS ConstructionNessuna valutazione finora

- Expanded Withholding TaxDocumento3 pagineExpanded Withholding TaxCordero TJNessuna valutazione finora

- A.8 Report On The Physical Count of Semi Expendable PropertyDocumento9 pagineA.8 Report On The Physical Count of Semi Expendable Propertyjaypee raguroNessuna valutazione finora

- Income Tax Law - A Capsule For Quick Recap IPCC Nov 18Documento28 pagineIncome Tax Law - A Capsule For Quick Recap IPCC Nov 18k moviesNessuna valutazione finora

- RATES FOR WITHHOLDING (INCOME) TAX 2023Documento1 paginaRATES FOR WITHHOLDING (INCOME) TAX 2023Muhammad Arham KhaliqNessuna valutazione finora

- Computation of Income Tax Due and PayableDocumento14 pagineComputation of Income Tax Due and Payablealia fauniNessuna valutazione finora

- Q1: Jan 2018: Deferred Tax Liabilities Deferred Tax AssetsDocumento17 pagineQ1: Jan 2018: Deferred Tax Liabilities Deferred Tax AssetsCliNessuna valutazione finora

- Withholding Rates Tax Year 2024Documento1 paginaWithholding Rates Tax Year 2024Maira ShahNessuna valutazione finora

- Rules On Succession of S. BaranggayDocumento4 pagineRules On Succession of S. BaranggayAtty. Jackelyn Joy PernitezNessuna valutazione finora

- Clamping Senate1 PDFDocumento3 pagineClamping Senate1 PDFAtty. Jackelyn Joy PernitezNessuna valutazione finora

- Dilg LoDocumento5 pagineDilg LoAtty. Jackelyn Joy PernitezNessuna valutazione finora

- DILG Legal Opinion 2012-101Documento1 paginaDILG Legal Opinion 2012-101Atty. Jackelyn Joy PernitezNessuna valutazione finora

- DILG Resources 201128 4e453a40c3Documento76 pagineDILG Resources 201128 4e453a40c3Mary Jane A DelosReyesNessuna valutazione finora

- Approved IRR On Controlled Chemicals PDFDocumento19 pagineApproved IRR On Controlled Chemicals PDFAtty. Jackelyn Joy PernitezNessuna valutazione finora

- 2012 Revised IRR of RA 7183 With Endorsement To UP Law Center PDFDocumento14 pagine2012 Revised IRR of RA 7183 With Endorsement To UP Law Center PDFAtty. Jackelyn Joy PernitezNessuna valutazione finora

- CSC Guidelines On Job Order PDFDocumento7 pagineCSC Guidelines On Job Order PDFAtty. Jackelyn Joy PernitezNessuna valutazione finora

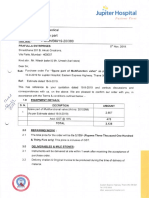

- Jupiter Thane PODocumento4 pagineJupiter Thane POAnonymous SXTKyUsNessuna valutazione finora

- MUHS revises TA/DA rules for travel by air, rail, roadDocumento10 pagineMUHS revises TA/DA rules for travel by air, rail, roadsachin sonawane100% (1)

- Account Statement 05 01 2021 PDFDocumento1 paginaAccount Statement 05 01 2021 PDFGabiMalaquiasNessuna valutazione finora

- Jio Mobile Statement for Kanika MalhotraDocumento3 pagineJio Mobile Statement for Kanika MalhotraDhruve PatelNessuna valutazione finora

- Updated List of Insurance Entities in Good Standing As at November 20, 2020Documento5 pagineUpdated List of Insurance Entities in Good Standing As at November 20, 2020Fuaad DodooNessuna valutazione finora

- BAPA FormDocumento6 pagineBAPA FormkatrinaNessuna valutazione finora

- Bill Payment: Details On Breb (Prepaid) ConfigurationDocumento12 pagineBill Payment: Details On Breb (Prepaid) ConfigurationMd Tanvir Hossain100% (1)

- Tibetan Grill: Jacob SheridanDocumento23 pagineTibetan Grill: Jacob SheridanJacob Sheridan100% (1)

- Kendra paraDocumento5 pagineKendra paraPrarthana MohapatraNessuna valutazione finora

- Account Statement From 1 Feb 2022 To 31 Jan 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento15 pagineAccount Statement From 1 Feb 2022 To 31 Jan 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAarti ThdfcNessuna valutazione finora

- Final Price AED 773: Booking ConfirmationDocumento2 pagineFinal Price AED 773: Booking ConfirmationKristina KristinaNessuna valutazione finora

- Top 4 Lifetime Free Credit Cards That You Should Look Out For in JULY 2023Documento3 pagineTop 4 Lifetime Free Credit Cards That You Should Look Out For in JULY 2023Anchal ChopraNessuna valutazione finora

- Post-Closing Trial BalanceDocumento3 paginePost-Closing Trial BalanceSuszie Sue70% (10)

- Eross Security Force AgencyDocumento2 pagineEross Security Force AgencyJbars Backyard GFNessuna valutazione finora

- Lam paraDocumento1 paginaLam paraSpecialOneNessuna valutazione finora

- B2B Delivery Instructions in LatviaDocumento3 pagineB2B Delivery Instructions in LatviaacmeaccNessuna valutazione finora

- Understanding Brazil's Payment IndustryDocumento32 pagineUnderstanding Brazil's Payment IndustryPedro AleNessuna valutazione finora

- Bengaluru To Jaipur Lurkmv: Air Asia I5-1576Documento3 pagineBengaluru To Jaipur Lurkmv: Air Asia I5-1576maneeshNessuna valutazione finora

- Terumo - Tllu6099284 - EdDocumento2 pagineTerumo - Tllu6099284 - EdmnmusorNessuna valutazione finora

- XII ScienceDocumento1 paginaXII ScienceShahzaib MughalNessuna valutazione finora

- Account StatementDocumento18 pagineAccount StatementLollyNessuna valutazione finora

- Indian Income Tax Return Acknowledgement Form ITR-6Documento1 paginaIndian Income Tax Return Acknowledgement Form ITR-6Deepak kumar M RNessuna valutazione finora

- Acctg 16 - Final LessonsDocumento24 pagineAcctg 16 - Final LessonsKarla OñasNessuna valutazione finora

- INVENTORY MGMT OBJECTIVESDocumento3 pagineINVENTORY MGMT OBJECTIVESAzyrah Lyren Seguban Ulpindo100% (1)

- EXPENSES AUGUST 2019 - Ms. JewelynDocumento31 pagineEXPENSES AUGUST 2019 - Ms. JewelynJewelyn C. Espares-CioconNessuna valutazione finora

- ABSLI SecurePlus Plan Brochure PDFDocumento16 pagineABSLI SecurePlus Plan Brochure PDFRajNessuna valutazione finora