Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Cibil - Report (P - SANJEEV KAMAL - 12 - 05 - 2023 14 - 49 - 45)Documento7 pagineCibil - Report (P - SANJEEV KAMAL - 12 - 05 - 2023 14 - 49 - 45)Miss PallaviNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- IBook - An Introduction To Non-Life Insurance Mathematics (1993)Documento113 pagineIBook - An Introduction To Non-Life Insurance Mathematics (1993)Jennifer ParkerNessuna valutazione finora

- Micro Finance in IndiaDocumento59 pagineMicro Finance in IndiaApurva Bangera100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Chapter 08 AnswersDocumento25 pagineChapter 08 AnswersMissy Rose LegaraNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Up To 2020-02-18 - HSBC Business Direct Portfolio Summary 02 - StatementDocumento3 pagineUp To 2020-02-18 - HSBC Business Direct Portfolio Summary 02 - StatementLevi dos SantosNessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Accounting Equation ExercisesDocumento2 pagineAccounting Equation ExercisesBert Rainier OpimoNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Edelweiss Financial Services LTDDocumento7 pagineEdelweiss Financial Services LTDMukesh SharmaNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Assessment 3 2024 Financial AssetDocumento9 pagineAssessment 3 2024 Financial Assetmarinel pioquidNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- DHFL Sanction LetterDocumento6 pagineDHFL Sanction LetterRamesh Kulkarni75% (4)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Additional Illustrations-13Documento9 pagineAdditional Illustrations-13Gulneer LambaNessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Draft Fixture 22 May 2023Documento9 pagineDraft Fixture 22 May 2023Amitav Ranjan DewanjeeNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Dissolution of A PartnerDocumento11 pagineDissolution of A PartnerjdsiNessuna valutazione finora

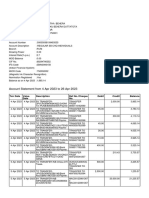

- Account Statement From 4 Apr 2023 To 26 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento7 pagineAccount Statement From 4 Apr 2023 To 26 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceBIKRAM KUMAR BEHERANessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- DMGT512 Financial Institutions and ServicesDocumento264 pagineDMGT512 Financial Institutions and Serviceskrisari9Nessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Exon Mobile Financial Data BloombergDocumento32 pagineExon Mobile Financial Data BloombergShardul MudeNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- NEGOTIABLE INSTRUMENT-Written Compliance - 20170201215-GACUTANDocumento27 pagineNEGOTIABLE INSTRUMENT-Written Compliance - 20170201215-GACUTANAnneNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Cfa Level 1 BrochureDocumento4 pagineCfa Level 1 Brochureaditya24292Nessuna valutazione finora

- Balance StatementDocumento3 pagineBalance StatementMellanie True Hills100% (1)

- Account StatementDocumento12 pagineAccount StatementPRABHAKAR REDDY TBSF - TELANGANANessuna valutazione finora

- Reading 21 Financial Analysis TechniquesDocumento74 pagineReading 21 Financial Analysis TechniquesNeerajNessuna valutazione finora

- Discount Market IntroductionDocumento2 pagineDiscount Market IntroductionsadathnooriNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Partnership Agreement: 1. PartiesDocumento11 paginePartnership Agreement: 1. PartiesAmelia ConwayNessuna valutazione finora

- Access Bank PLCDocumento2 pagineAccess Bank PLCDikadi Chinedu MicahNessuna valutazione finora

- 1001 Questions For Last Moment Banking PreparationsDocumento35 pagine1001 Questions For Last Moment Banking PreparationsAparajito SethNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- MOSt Market Roundup 27 TH Aug 21Documento7 pagineMOSt Market Roundup 27 TH Aug 21vikalp123123Nessuna valutazione finora

- S.K.School of Business ManagementDocumento21 pagineS.K.School of Business ManagementManan Gondaliya0% (1)

- FinmanDocumento9 pagineFinmanCharles MateoNessuna valutazione finora

- Chapter 008 SolutionsDocumento6 pagineChapter 008 SolutionsAnton VelkovNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (120)

- Analisis Rasio Keuangan - PT Blue BirdDocumento8 pagineAnalisis Rasio Keuangan - PT Blue BirdAzis HailyNessuna valutazione finora

- Chargeback GuideDocumento716 pagineChargeback GuideAna Paola T Munoz0% (1)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)