Potrebbero piacerti anche

- Acc 3200 MidtermDocumento5 pagineAcc 3200 MidtermCici ZhouNessuna valutazione finora

- Cost AccountingDocumento15 pagineCost Accountingesayas goysaNessuna valutazione finora

- Group 8 - Chap 2 An Introduction To Cost Terms and PurposeseDocumento39 pagineGroup 8 - Chap 2 An Introduction To Cost Terms and Purposeseqgminh7114Nessuna valutazione finora

- Summary Chapter 1Documento13 pagineSummary Chapter 1Danny FranklinNessuna valutazione finora

- 2 - Cost Concepts and BehaviorDocumento3 pagine2 - Cost Concepts and BehaviorPattraniteNessuna valutazione finora

- Module 2 - Introduction To Cost ConceptsDocumento51 pagineModule 2 - Introduction To Cost Conceptskaizen4apexNessuna valutazione finora

- Atp 106 LPM Accounting - Topic 6 - Costing and BudgetingDocumento17 pagineAtp 106 LPM Accounting - Topic 6 - Costing and BudgetingTwain JonesNessuna valutazione finora

- MGT Acctg Cost ConceptDocumento30 pagineMGT Acctg Cost ConceptApril Pearl VenezuelaNessuna valutazione finora

- 79 52 ET V1 S1 - Unit - 6 PDFDocumento19 pagine79 52 ET V1 S1 - Unit - 6 PDFTanmay JagetiaNessuna valutazione finora

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesDa EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNessuna valutazione finora

- Cost Analysis: 1) Opportunity Costs and Outlay CostsDocumento8 pagineCost Analysis: 1) Opportunity Costs and Outlay Costsakash creationNessuna valutazione finora

- Chapter 2 Cost IDocumento13 pagineChapter 2 Cost IHussen AbdulkadirNessuna valutazione finora

- MCODocumento11 pagineMCOsubhaa DasNessuna valutazione finora

- 11th Sem - Cost ACT 1st NoteDocumento5 pagine11th Sem - Cost ACT 1st NoteRobin420420Nessuna valutazione finora

- Period Cost Is Related To Level of Production and SaleDocumento6 paginePeriod Cost Is Related To Level of Production and SaleMd. Saiful AlamNessuna valutazione finora

- Note of Cost Accounting IncomDocumento5 pagineNote of Cost Accounting IncomAdam AbdullahiNessuna valutazione finora

- Chap 2 The-Manager-and-Management-AccountingDocumento11 pagineChap 2 The-Manager-and-Management-Accountingqgminh7114Nessuna valutazione finora

- Management Accounting Notes: Nature of Management Accounting Characteristics of Management AccountingDocumento7 pagineManagement Accounting Notes: Nature of Management Accounting Characteristics of Management AccountingRobin FernandoNessuna valutazione finora

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageDa EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageValutazione: 5 su 5 stelle5/5 (1)

- Marginal and Absorption CostingDocumento5 pagineMarginal and Absorption CostingHrutik DeshmukhNessuna valutazione finora

- Cost AnalysisDocumento48 pagineCost AnalysisdrajingoNessuna valutazione finora

- Full Cost AccountingDocumento27 pagineFull Cost AccountingMarjorie OndevillaNessuna valutazione finora

- Chapter FourDocumento12 pagineChapter FourhabatmuNessuna valutazione finora

- Chapter Two: Cost Terminology and Classification: Learning OutcomesDocumento8 pagineChapter Two: Cost Terminology and Classification: Learning OutcomesKanbiro Orkaido100% (1)

- MAF Notes Mid ExamDocumento8 pagineMAF Notes Mid ExamPenguin Da Business GooseNessuna valutazione finora

- Cost Accounitng NotesDocumento17 pagineCost Accounitng NotesDarlene JoyceNessuna valutazione finora

- Management AccountingDocumento13 pagineManagement AccountingYashwant ShrimaliNessuna valutazione finora

- Introduction To Cost Accounting Final With PDFDocumento19 pagineIntroduction To Cost Accounting Final With PDFLemon EnvoyNessuna valutazione finora

- Cost ConceptDocumento6 pagineCost ConceptDeepti KumariNessuna valutazione finora

- Management Accounting NotesDocumento9 pagineManagement Accounting NotesGazal GuptaNessuna valutazione finora

- Management Accounting NotesDocumento9 pagineManagement Accounting NoteskamdicaNessuna valutazione finora

- Cost Accounting: Information For Decision Making: Learning ObjectivesDocumento11 pagineCost Accounting: Information For Decision Making: Learning ObjectivesJohn OpeñaNessuna valutazione finora

- WWW - Globalcma.in: Cost Accounting Interview QuestionsDocumento12 pagineWWW - Globalcma.in: Cost Accounting Interview Questionsjawed ahmerNessuna valutazione finora

- Definition of Cost AccountingDocumento11 pagineDefinition of Cost Accountingkenshi ihsnekNessuna valutazione finora

- Classification of CostingDocumento22 pagineClassification of CostingMohamaad SihatthNessuna valutazione finora

- Cost Accounting - Meaning and ScopeDocumento27 pagineCost Accounting - Meaning and ScopemenakaNessuna valutazione finora

- Accountancy SectionDocumento124 pagineAccountancy Sections7k1994Nessuna valutazione finora

- ACC 321 Final Exam ReviewDocumento6 pagineACC 321 Final Exam ReviewLauren KlaassenNessuna valutazione finora

- Cost Accounting DefinationsDocumento7 pagineCost Accounting DefinationsJâmâl HassanNessuna valutazione finora

- Acca Paper 1.2Documento25 pagineAcca Paper 1.2anon-280248Nessuna valutazione finora

- Costingmaterials and LabourDocumento12 pagineCostingmaterials and LabourANISAHMNessuna valutazione finora

- COST ANALYSIS - 62 Questions With AnswersDocumento6 pagineCOST ANALYSIS - 62 Questions With Answersmehdi everythingNessuna valutazione finora

- Cost Volume Profit AnalysisDocumento32 pagineCost Volume Profit AnalysisADILLA ADZHARUDDIN100% (1)

- Module 1 - Overview of Cost AccountingDocumento7 pagineModule 1 - Overview of Cost AccountingMae JessaNessuna valutazione finora

- Chapter 5Documento13 pagineChapter 5abraha gebruNessuna valutazione finora

- Cost Accounting and Control: Cagayan State UniversityDocumento74 pagineCost Accounting and Control: Cagayan State UniversityAntonNessuna valutazione finora

- Cost Accounting and Control Lecture NotesDocumento11 pagineCost Accounting and Control Lecture NotesAnalyn LafradezNessuna valutazione finora

- CST Accounting by Ig ClassesDocumento39 pagineCST Accounting by Ig Classesraman sharma100% (1)

- Elements of Cost: Expense TypesDocumento17 pagineElements of Cost: Expense Typesسعيد الشوكانيNessuna valutazione finora

- Universidad Tecnológica de Coahuila Production Cost Accounting ClassDocumento13 pagineUniversidad Tecnológica de Coahuila Production Cost Accounting ClassEdgar IbarraNessuna valutazione finora

- Cost & Management Accounting (ACT 301) : Department: BBA Group: 1Documento7 pagineCost & Management Accounting (ACT 301) : Department: BBA Group: 1Mony MstNessuna valutazione finora

- Managerial Accounting: Cost TerminologyDocumento18 pagineManagerial Accounting: Cost TerminologyHibaaq Axmed100% (1)

- Meaning of Cost AccountingDocumento16 pagineMeaning of Cost Accounting1028Nessuna valutazione finora

- CostDocumento33 pagineCostversmajardoNessuna valutazione finora

- CostingDocumento32 pagineCostingnidhiNessuna valutazione finora

- FIN600 Module 3 Notes - Financial Management Accounting ConceptsDocumento20 pagineFIN600 Module 3 Notes - Financial Management Accounting ConceptsInés Tetuá TralleroNessuna valutazione finora

- ACC 304 Oral First TermDocumento3 pagineACC 304 Oral First TermMahmudul HasanNessuna valutazione finora

- MB 0042Documento30 pagineMB 0042Rehan QuadriNessuna valutazione finora

- BBA Management AccountingDocumento8 pagineBBA Management AccountingMohamaad SihatthNessuna valutazione finora

- Professor Steve Markoff Preparation Assignment For Class #1: Fundamentals of AccountingDocumento4 pagineProfessor Steve Markoff Preparation Assignment For Class #1: Fundamentals of Accountinganon_733987828Nessuna valutazione finora

- Financial Accounting and Reporting 1 (Acg001) Week 2: Accounting and Its Environment (Part 1)Documento19 pagineFinancial Accounting and Reporting 1 (Acg001) Week 2: Accounting and Its Environment (Part 1)kookie bunnyNessuna valutazione finora

- Introduction To Financial Accounting NotesDocumento3 pagineIntroduction To Financial Accounting NotesRaksa HemNessuna valutazione finora

- Aud339 Audit ReportDocumento22 pagineAud339 Audit ReportNur IzzahNessuna valutazione finora

- 0157 20230901 Motion To Comply With The August 14 RO Final CombinedDocumento86 pagine0157 20230901 Motion To Comply With The August 14 RO Final CombinedMetro Puerto RicoNessuna valutazione finora

- Uems Aac 2022Documento133 pagineUems Aac 2022maswebNessuna valutazione finora

- Cuck Cost Accounting PDFDocumento119 pagineCuck Cost Accounting PDFaponojecy50% (2)

- Account TitlesDocumento4 pagineAccount TitlesHermae Bucton100% (1)

- AP-200Q (Quizzer - Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Documento10 pagineAP-200Q (Quizzer - Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Bernadette Panican100% (1)

- Financial Accounting Objectives Sem V PDFDocumento14 pagineFinancial Accounting Objectives Sem V PDFAyman MalikNessuna valutazione finora

- ReceivablesDocumento4 pagineReceivableshellohello50% (2)

- Waterfall Chart Slides PowerPoint TemplateDocumento30 pagineWaterfall Chart Slides PowerPoint Templateziad ghanemNessuna valutazione finora

- At Quizzer 3 - 2018 Code of Ethics For Professional Accountants in The Phils T1AY2122Documento15 pagineAt Quizzer 3 - 2018 Code of Ethics For Professional Accountants in The Phils T1AY2122Rena NervalNessuna valutazione finora

- Training Perpajakan - FINALDocumento52 pagineTraining Perpajakan - FINALDonald BebekNessuna valutazione finora

- Book 6Documento4 pagineBook 6Actg SolmanNessuna valutazione finora

- Mary Anne C. Bantog: ObjectiveDocumento4 pagineMary Anne C. Bantog: ObjectiveUWatch TVNessuna valutazione finora

- Accounting Entries in R12 Account Receivables - Oracle Apps Knowledge SharingDocumento6 pagineAccounting Entries in R12 Account Receivables - Oracle Apps Knowledge Sharingdevender143Nessuna valutazione finora

- GL SQLDocumento44 pagineGL SQLBalaji Shinde100% (1)

- CfasDocumento3 pagineCfasWinnie ToribioNessuna valutazione finora

- GL PPT Basic For Oracle AppsDocumento81 pagineGL PPT Basic For Oracle AppsPhanendra KumarNessuna valutazione finora

- College of Accountancy: Lesson 1 - Concepts of CapitalDocumento4 pagineCollege of Accountancy: Lesson 1 - Concepts of Capitalfirestorm riveraNessuna valutazione finora

- Problem Solving: Merchandising Problem (Periodic Inventory System)Documento1 paginaProblem Solving: Merchandising Problem (Periodic Inventory System)Vincent Madrid100% (6)

- Internship Report of NBPDocumento122 pagineInternship Report of NBPrabirabi94% (47)

- TEST BANK For Advanced Financial Accounting 13th Edition by Theodore Christensen Verified Chapter's 1 - 20 CompleteDocumento70 pagineTEST BANK For Advanced Financial Accounting 13th Edition by Theodore Christensen Verified Chapter's 1 - 20 Completemarcuskenyatta275Nessuna valutazione finora

- Ebook College Accounting Chapters 1 30 13Th Edition Price Solutions Manual Full Chapter PDFDocumento67 pagineEbook College Accounting Chapters 1 30 13Th Edition Price Solutions Manual Full Chapter PDFconvive.unsadden.hgp2100% (12)

- AP-5906 ReceivablesDocumento5 pagineAP-5906 Receivablesjhouvan100% (1)

- Accounting For Merchandising Operations: Weygandt - Kieso - KimmelDocumento62 pagineAccounting For Merchandising Operations: Weygandt - Kieso - KimmelMaidah NaeemNessuna valutazione finora

- Chapter 4: Completing The Accounting Cycle 1. Steps in Prepareing A WorksheetDocumento8 pagineChapter 4: Completing The Accounting Cycle 1. Steps in Prepareing A WorksheetNguyễn Quỳnh AnhNessuna valutazione finora

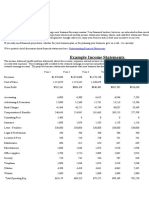

- Example Income Statements: Business Plan Financial ProjectionsDocumento3 pagineExample Income Statements: Business Plan Financial ProjectionsSUMANTO SHARANNessuna valutazione finora

- Chapter 7aDocumento14 pagineChapter 7aKanton Fernandez100% (6)