Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Introduction To Soft Floor CoveringsDocumento13 pagineIntroduction To Soft Floor CoveringsJothi Vel Murugan83% (6)

- Revised PARA Element2 Radio LawsDocumento81 pagineRevised PARA Element2 Radio LawsAurora Pelagio Vallejos100% (4)

- AHU CatalogueDocumento16 pagineAHU CatalogueWai Ee YapNessuna valutazione finora

- 27 Points of Difference Between Personnel Management & HRDDocumento2 pagine27 Points of Difference Between Personnel Management & HRDMurtaza Ejaz33% (3)

- CBLM - Interpreting Technical DrawingDocumento18 pagineCBLM - Interpreting Technical DrawingGlenn F. Salandanan89% (45)

- Project ProposalDocumento2 pagineProject Proposalqueen malik80% (5)

- Cot Observation ToolDocumento14 pagineCot Observation ToolArnoldBaladjayNessuna valutazione finora

- Mass and Heat Balance of Steelmaking in Bof As Compared To Eaf ProcessesDocumento15 pagineMass and Heat Balance of Steelmaking in Bof As Compared To Eaf ProcessesAgil Setyawan100% (1)

- Digital Speed Control of DC Motor For Industrial Automation Using Pulse Width Modulation TechniqueDocumento6 pagineDigital Speed Control of DC Motor For Industrial Automation Using Pulse Width Modulation TechniquevendiNessuna valutazione finora

- Dashrath Nandan JAVA (Unit2) NotesDocumento18 pagineDashrath Nandan JAVA (Unit2) NotesAbhinandan Singh RanaNessuna valutazione finora

- Case StudyDocumento15 pagineCase StudyChaitali moreyNessuna valutazione finora

- BGP PDFDocumento100 pagineBGP PDFJeya ChandranNessuna valutazione finora

- Benchmark Leadership Philosphy Ead 501Documento5 pagineBenchmark Leadership Philosphy Ead 501api-494301924Nessuna valutazione finora

- Contract 1 ProjectDocumento21 pagineContract 1 ProjectAditi BanerjeeNessuna valutazione finora

- DLL - English 5 - Q3 - W8Documento8 pagineDLL - English 5 - Q3 - W8Merlyn S. Al-osNessuna valutazione finora

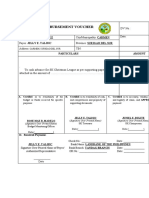

- Disbursement VoucherDocumento7 pagineDisbursement VoucherDan MarkNessuna valutazione finora

- AAPG 2012 ICE Technical Program & Registration AnnouncementDocumento64 pagineAAPG 2012 ICE Technical Program & Registration AnnouncementAAPG_EventsNessuna valutazione finora

- OMN-TRA-SSR-OETC-Course Workbook 2daysDocumento55 pagineOMN-TRA-SSR-OETC-Course Workbook 2daysMANIKANDAN NARAYANASAMYNessuna valutazione finora

- 96 Dec2018 NZGeoNews PDFDocumento139 pagine96 Dec2018 NZGeoNews PDFAditya PrasadNessuna valutazione finora

- EceDocumento75 pagineEcevignesh16vlsiNessuna valutazione finora

- Conference Paper 2Documento5 pagineConference Paper 2Sri JayanthNessuna valutazione finora

- SPWM Vs SVMDocumento11 pagineSPWM Vs SVMpmbalajibtechNessuna valutazione finora

- Re BuyerDocumento20 pagineRe BuyerElias OjuokNessuna valutazione finora

- 3Documento76 pagine3Uday ShankarNessuna valutazione finora

- Consequences of Self-Handicapping: Effects On Coping, Academic Performance, and AdjustmentDocumento11 pagineConsequences of Self-Handicapping: Effects On Coping, Academic Performance, and AdjustmentAlliah Kate SalvadorNessuna valutazione finora

- 103-Article Text-514-1-10-20190329Documento11 pagine103-Article Text-514-1-10-20190329Elok KurniaNessuna valutazione finora

- Tournament Rules and MechanicsDocumento2 pagineTournament Rules and MechanicsMarkAllenPascualNessuna valutazione finora

- TMA GuideDocumento3 pagineTMA GuideHamshavathini YohoratnamNessuna valutazione finora

- Read The Dialogue Below and Answer The Following QuestionDocumento5 pagineRead The Dialogue Below and Answer The Following QuestionDavid GainesNessuna valutazione finora

- Basics PDFDocumento21 pagineBasics PDFSunil KumarNessuna valutazione finora