Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- How To Start A Hot Dog Stand - Free GuideDocumento43 pagineHow To Start A Hot Dog Stand - Free Guidesteve184837550% (2)

- Partnership Operations: Accounting Cycle of A PartnershipDocumento13 paginePartnership Operations: Accounting Cycle of A Partnershipred100% (1)

- Customer Centric Selling Summary by Frumi Rachel BarrDocumento21 pagineCustomer Centric Selling Summary by Frumi Rachel Barrpurple_bad100% (1)

- Three Models of Corporate Social ResponsibilityDocumento8 pagineThree Models of Corporate Social Responsibilityred100% (4)

- HP Channel StrategyDocumento10 pagineHP Channel StrategyMohammad Delowar Hossain100% (5)

- SWOT Analysis Focus PointDocumento3 pagineSWOT Analysis Focus PointJaeEun Siwon100% (3)

- A Study On Pantaloons Supply Chain DistributionDocumento20 pagineA Study On Pantaloons Supply Chain DistributionVINIT SINGH0% (1)

- Technology and Livelihood Education Entre Module 2Documento13 pagineTechnology and Livelihood Education Entre Module 2Boy SawagaNessuna valutazione finora

- General and Application Controls For Information SystemDocumento12 pagineGeneral and Application Controls For Information SystemredNessuna valutazione finora

- Risk Exposures and The Internal Control StructureDocumento20 pagineRisk Exposures and The Internal Control StructureredNessuna valutazione finora

- RiskmgmteventsDocumento2 pagineRiskmgmteventsredNessuna valutazione finora

- Managing Security of InformationDocumento4 pagineManaging Security of InformationredNessuna valutazione finora

- Phoenix Petroleum Philippines, IncDocumento1 paginaPhoenix Petroleum Philippines, IncredNessuna valutazione finora

- National Income DeterminationDocumento8 pagineNational Income DeterminationredNessuna valutazione finora

- The Three Pillars of SustainabilityDocumento9 pagineThe Three Pillars of SustainabilityredNessuna valutazione finora

- Ilocos Norte 17Documento5 pagineIlocos Norte 17redNessuna valutazione finora

- CSR Policy EdcDocumento3 pagineCSR Policy EdcredNessuna valutazione finora

- Aggregate Planning Strategies: Aggregate Planning Is The Process of Developing, Analyzing, and Maintaining A PreliminaryDocumento6 pagineAggregate Planning Strategies: Aggregate Planning Is The Process of Developing, Analyzing, and Maintaining A PreliminaryredNessuna valutazione finora

- Business ProposalDocumento10 pagineBusiness ProposalredNessuna valutazione finora

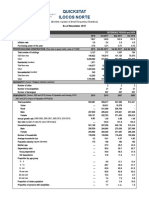

- Quickstat Ilocos Norte: (Monthly Update of Most Requested Statistics)Documento4 pagineQuickstat Ilocos Norte: (Monthly Update of Most Requested Statistics)redNessuna valutazione finora

- Increases Media Coverage: 1. Improves Public ImageDocumento6 pagineIncreases Media Coverage: 1. Improves Public ImageredNessuna valutazione finora

- Concrete BlockDocumento3 pagineConcrete BlockredNessuna valutazione finora

- Uber Case StudyDocumento15 pagineUber Case StudyNafisa NavallNessuna valutazione finora

- OSCM McqsDocumento3 pagineOSCM Mcqssundeep chaudhariNessuna valutazione finora

- Rural Marketing 260214 PDFDocumento282 pagineRural Marketing 260214 PDFarulsureshNessuna valutazione finora

- Rural Marketing in Indian ContextDocumento5 pagineRural Marketing in Indian ContextSikander Khilji100% (1)

- Two Part Tariff ExampleDocumento8 pagineTwo Part Tariff Exampleestevez999Nessuna valutazione finora

- Asias Temples of LuxuryDocumento7 pagineAsias Temples of Luxuryjasonvulog3626Nessuna valutazione finora

- Vendor Managed InventoryDocumento12 pagineVendor Managed InventoryPulkit SinhaNessuna valutazione finora

- Plant Layout of Coca Cola: Presented By: SMITA SINGH-2009PMB136 NAMITA NARULA-2009PMB147Documento33 paginePlant Layout of Coca Cola: Presented By: SMITA SINGH-2009PMB136 NAMITA NARULA-2009PMB147Saurav Singh100% (1)

- 11152019Documento31 pagine11152019Lindsey Ianna Pablo Andres100% (1)

- Legal Studies XII - Improvement First Weekly Test - 2Documento3 pagineLegal Studies XII - Improvement First Weekly Test - 2Surbhit ShrivastavaNessuna valutazione finora

- Indonesia Sales Order FormDocumento1 paginaIndonesia Sales Order FormObis BeladasNessuna valutazione finora

- College of Business Administration: Management and Marketing DepartmentDocumento43 pagineCollege of Business Administration: Management and Marketing Departmentnina jobleNessuna valutazione finora

- New Perspective On Services MarketingDocumento32 pagineNew Perspective On Services MarketingLuthfi Farhana100% (2)

- Managing People For Service AdvantageDocumento37 pagineManaging People For Service AdvantageAnkit KumarNessuna valutazione finora

- ch02 QPMDocumento21 paginech02 QPMovaisNessuna valutazione finora

- WACC Case StudyDocumento2 pagineWACC Case StudyMuhammad AdeelNessuna valutazione finora

- Model Test 2: Listening ComprehensionDocumento19 pagineModel Test 2: Listening ComprehensionSergioDanielMazzeoNessuna valutazione finora

- Apna Bazaar Consumer Co-OperativeDocumento36 pagineApna Bazaar Consumer Co-OperativeAnchal singh0% (1)

- RANA HANNA - MarketingDocumento19 pagineRANA HANNA - MarketingRana HannaNessuna valutazione finora

- Chapter 11Documento53 pagineChapter 11Vijendhar ReddyNessuna valutazione finora

- Consumer Perception Keshoram 63 14Documento63 pagineConsumer Perception Keshoram 63 14Arun KumaarNessuna valutazione finora

- SP IMMIGRATION SERVICES INC. Fiancail Plan - Rough DraftDocumento24 pagineSP IMMIGRATION SERVICES INC. Fiancail Plan - Rough Draftmalik_saleem_akbarNessuna valutazione finora

- CaseletsDocumento2 pagineCaseletsDivya Bharathi RNessuna valutazione finora

- Chapter 3.2 Futures HedgingDocumento19 pagineChapter 3.2 Futures HedginglelouchNessuna valutazione finora