Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Top SecretDocumento45 pagineTop SecretkrisnaNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Security Analysis and Portfolio Management - Lecture Notes, Study Material and Important Questions, AnswersDocumento5 pagineSecurity Analysis and Portfolio Management - Lecture Notes, Study Material and Important Questions, AnswersM.V. TV67% (3)

- Investment and Portfolio AnalysisDocumento26 pagineInvestment and Portfolio Analysismakoto-sanNessuna valutazione finora

- Bloomberg Aptitude Test BATDocumento35 pagineBloomberg Aptitude Test BATqcfinanceNessuna valutazione finora

- A Project Report On Overview of Indian Stock MarketDocumento25 pagineA Project Report On Overview of Indian Stock MarketAshok Chowdary GNessuna valutazione finora

- Ceili Sample Questions Set 2Documento26 pagineCeili Sample Questions Set 2jsdawson67% (3)

- Introduction To Foreign Exchange Rates, Second EditionDocumento32 pagineIntroduction To Foreign Exchange Rates, Second EditionCharleneKronstedt100% (1)

- EPD - Argus PDFDocumento5 pagineEPD - Argus PDFJeff SturgeonNessuna valutazione finora

- MMP - RatingsDocumento4 pagineMMP - RatingsJeff SturgeonNessuna valutazione finora

- HEP - Ratings PDFDocumento4 pagineHEP - Ratings PDFJeff SturgeonNessuna valutazione finora

- EPD - Schwab PDFDocumento16 pagineEPD - Schwab PDFJeff SturgeonNessuna valutazione finora

- HP - Argus PDFDocumento5 pagineHP - Argus PDFJeff SturgeonNessuna valutazione finora

- MMP - SchwabDocumento17 pagineMMP - SchwabJeff SturgeonNessuna valutazione finora

- OHI - RatingsDocumento4 pagineOHI - RatingsJeff SturgeonNessuna valutazione finora

- Leibold RF Weaver 3B Collins 2B Jackson LF Felsch CF Gandil 1B Risberg SS Schalk C PDocumento12 pagineLeibold RF Weaver 3B Collins 2B Jackson LF Felsch CF Gandil 1B Risberg SS Schalk C PJeff SturgeonNessuna valutazione finora

- Schwab Ratios User GuideDocumento2 pagineSchwab Ratios User GuideJeff SturgeonNessuna valutazione finora

- OKE - SchwabDocumento5 pagineOKE - SchwabJeff SturgeonNessuna valutazione finora

- MDP - SchwabDocumento5 pagineMDP - SchwabJeff SturgeonNessuna valutazione finora

- MDP - RatingsDocumento4 pagineMDP - RatingsJeff SturgeonNessuna valutazione finora

- OKE - ArgusDocumento5 pagineOKE - ArgusJeff SturgeonNessuna valutazione finora

- OKE - RatingsDocumento4 pagineOKE - RatingsJeff SturgeonNessuna valutazione finora

- Aztec Gold Dry RubDocumento9 pagineAztec Gold Dry RubJeff SturgeonNessuna valutazione finora

- Byrne 3B Leach CF Clarke LF Wagner SS Miller 2B Abstein 1B Wilson RF Gibson C PDocumento12 pagineByrne 3B Leach CF Clarke LF Wagner SS Miller 2B Abstein 1B Wilson RF Gibson C PJeff SturgeonNessuna valutazione finora

- Slagle CF Sheckard LF Schulte RF Chance 1B Steinfeldt 3B Tinker SS Evers 2B Kling C PDocumento12 pagineSlagle CF Sheckard LF Schulte RF Chance 1B Steinfeldt 3B Tinker SS Evers 2B Kling C PJeff SturgeonNessuna valutazione finora

- Browne RF Donlin CF Mcgann 1B Mertes LF Dahlen Ss Devlin 3B Gilbert 2B Bresnahan C PDocumento12 pagineBrowne RF Donlin CF Mcgann 1B Mertes LF Dahlen Ss Devlin 3B Gilbert 2B Bresnahan C PJeff SturgeonNessuna valutazione finora

- Cfra - TmusDocumento9 pagineCfra - TmusJeff SturgeonNessuna valutazione finora

- Betts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFDocumento16 pagineBetts RF Benintendi LF Bogearts SS Martinez DH Devers 3B Nunez 2B Holt 1B Leon C Bradley Jr. CFJeff SturgeonNessuna valutazione finora

- Argus - DLR PDFDocumento5 pagineArgus - DLR PDFJeff SturgeonNessuna valutazione finora

- Digital Realty Trust Inc: Analyst's NotesDocumento5 pagineDigital Realty Trust Inc: Analyst's NotesJeff SturgeonNessuna valutazione finora

- Argus - TMUSDocumento6 pagineArgus - TMUSJeff SturgeonNessuna valutazione finora

- Morningstar - TMUSDocumento15 pagineMorningstar - TMUSJeff SturgeonNessuna valutazione finora

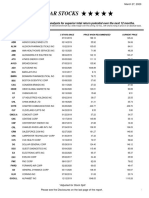

- Five Star StocksDocumento5 pagineFive Star StocksJeff SturgeonNessuna valutazione finora

- Sanofi Sa: Analyst's NotesDocumento5 pagineSanofi Sa: Analyst's NotesJeff SturgeonNessuna valutazione finora

- Argus - SNY PDFDocumento5 pagineArgus - SNY PDFJeff SturgeonNessuna valutazione finora

- Interim Order in The Matter of Mr. Anirudh SethiDocumento14 pagineInterim Order in The Matter of Mr. Anirudh SethiShyam SunderNessuna valutazione finora

- Class 02Documento3 pagineClass 02Aasim Bin BakrNessuna valutazione finora

- 2013-10 Avolon - Funding The FutureDocumento18 pagine2013-10 Avolon - Funding The Futureawang90Nessuna valutazione finora

- The Act Borrowers Guide To Lma Loan Documentation For Investment Grade Borrowers June 2014 SupplementDocumento20 pagineThe Act Borrowers Guide To Lma Loan Documentation For Investment Grade Borrowers June 2014 SupplementkamisyedNessuna valutazione finora

- Stock Market Development and Economic GrowthDocumento18 pagineStock Market Development and Economic GrowthAhmedNessuna valutazione finora

- Capital Goods-Non Electrical Equipment - Update1 - NewDocumento20 pagineCapital Goods-Non Electrical Equipment - Update1 - Newjasraj_singhNessuna valutazione finora

- Unit 1Documento19 pagineUnit 1nestani shiukashviliNessuna valutazione finora

- Trắc nghiệm LTTCDocumento269 pagineTrắc nghiệm LTTCLINH NGUYEN NGOC THUYNessuna valutazione finora

- Chapter 4 - Review Questions 1Documento8 pagineChapter 4 - Review Questions 1Mizzy FernandezNessuna valutazione finora

- Economics HSC Course FULL NOTES - Text.markedDocumento72 pagineEconomics HSC Course FULL NOTES - Text.markedKrishna KannanNessuna valutazione finora

- Study of Factors Affecting Sales of ICICI Prudential Mutual Fund and Promotion and Competition Analysis of Its Popular SchemesDocumento64 pagineStudy of Factors Affecting Sales of ICICI Prudential Mutual Fund and Promotion and Competition Analysis of Its Popular SchemesChandan SrivastavaNessuna valutazione finora

- Diversification of Nigeria Economy and Applied Mathematicians As DriverDocumento9 pagineDiversification of Nigeria Economy and Applied Mathematicians As DriverOyelami Benjamin Oyediran100% (1)

- Note Topic 2Documento4 pagineNote Topic 2ModraNessuna valutazione finora

- Al-Bashir, Al-Amine - Risk - Management in IF - Analyses of Derivatives InstrumentsDocumento361 pagineAl-Bashir, Al-Amine - Risk - Management in IF - Analyses of Derivatives InstrumentsСергей БизюковNessuna valutazione finora

- Capital Market, Consumption and Investment (L1) : - Materials From Chapters 1&2, CWSDocumento22 pagineCapital Market, Consumption and Investment (L1) : - Materials From Chapters 1&2, CWSKamran Kamran100% (1)

- Bajaj CapitalDocumento15 pagineBajaj Capitalharshita khadayteNessuna valutazione finora

- PWC Emerging Trends in Real Estate 2017Documento108 paginePWC Emerging Trends in Real Estate 2017TBP_Think_Tank100% (4)

- Internship Report On: Non-Performing Loans in Banking Sector of Bangladesh: Causes and EffectDocumento29 pagineInternship Report On: Non-Performing Loans in Banking Sector of Bangladesh: Causes and EffectSurajit RoyNessuna valutazione finora

- Study of Risk Management in Stock Broking FirmDocumento71 pagineStudy of Risk Management in Stock Broking Firmamol_dindokar83% (12)

- Master Thesis Topics in Finance and BankingDocumento8 pagineMaster Thesis Topics in Finance and Bankingangeladominguezaurora100% (1)

- Inside Financial Markets: Khader ShaikDocumento71 pagineInside Financial Markets: Khader ShaikDaviNessuna valutazione finora

- Chapter 1 History and Development of Banking System in MalaysiaDocumento18 pagineChapter 1 History and Development of Banking System in MalaysiaMadihah JamianNessuna valutazione finora

- RE1 Trading CaseDocumento3 pagineRE1 Trading CaseDerrick LowNessuna valutazione finora