Potrebbero piacerti anche

- VolatilityDocumento6 pagineVolatilityEdoardo MartignoniNessuna valutazione finora

- Systematic Liquidity: Gur Huberman and Dominika HalkaDocumento18 pagineSystematic Liquidity: Gur Huberman and Dominika HalkaabhinavatripathiNessuna valutazione finora

- On The Relationship Between Investor Sentiment, Vix and Trading VolumeDocumento8 pagineOn The Relationship Between Investor Sentiment, Vix and Trading VolumeMinh TongNessuna valutazione finora

- Volatility Terminology: Finance Standard Deviation Financial Instrument RiskDocumento4 pagineVolatility Terminology: Finance Standard Deviation Financial Instrument RiskNikesh PoddarNessuna valutazione finora

- 02 SynopsisDocumento44 pagine02 SynopsisSanaullah M SultanpurNessuna valutazione finora

- What's Stock Market Volatility?Documento6 pagineWhat's Stock Market Volatility?Prathap PratapNessuna valutazione finora

- Volatility Analysis of The Price SeriesDocumento15 pagineVolatility Analysis of The Price SeriesRonitsinghthakur SinghNessuna valutazione finora

- Stock Market Volatility: An Evaluation: DR - Debesh BhowmikDocumento18 pagineStock Market Volatility: An Evaluation: DR - Debesh BhowmikPreeti LambaNessuna valutazione finora

- Why Is Price Volatility Not RiskyDocumento2 pagineWhy Is Price Volatility Not RiskyPalakNessuna valutazione finora

- The Stock MarketDocumento4 pagineThe Stock MarketBhumika BhardwajNessuna valutazione finora

- VOLATILITYDocumento13 pagineVOLATILITYOberoi MalhOtra MeenakshiNessuna valutazione finora

- Currency Futures Impact Spot VolatilityDocumento40 pagineCurrency Futures Impact Spot VolatilityrrrrrrrrNessuna valutazione finora

- Sapm Da 2Documento20 pagineSapm Da 2Surya SNessuna valutazione finora

- Presented By-Amit Kumar Khewar Roll No.109502 Nit-WarangalDocumento10 paginePresented By-Amit Kumar Khewar Roll No.109502 Nit-WarangalAmit KhewarNessuna valutazione finora

- Foreign Exchange SpeculationDocumento13 pagineForeign Exchange SpeculationKristy Dela PeñaNessuna valutazione finora

- Hsu JmpaperDocumento50 pagineHsu JmpaperKok Jin GanNessuna valutazione finora

- Morris LiquidityblackholesDocumento19 pagineMorris LiquidityblackholesOloyede RidwanNessuna valutazione finora

- Common Determinants of Bond and Stock Market Liquidity The Impact of Financial Crises Monetary Policy and Mutual Fund FlowsDocumento51 pagineCommon Determinants of Bond and Stock Market Liquidity The Impact of Financial Crises Monetary Policy and Mutual Fund FlowsAhmed100% (1)

- Properties of High Frequency DAX Returns Intraday Patterns, Philippe MassetDocumento28 pagineProperties of High Frequency DAX Returns Intraday Patterns, Philippe MassetDigito DunkeyNessuna valutazione finora

- Understanding Volatility and How To Measure It: Key TakeawaysDocumento2 pagineUnderstanding Volatility and How To Measure It: Key TakeawaysCr HtNessuna valutazione finora

- Final Project On Volatility - New 2Documento99 pagineFinal Project On Volatility - New 2vipul099Nessuna valutazione finora

- Prakash 123Documento47 paginePrakash 123Prakash VishwakarmaNessuna valutazione finora

- ContributedDocumento3 pagineContributedapi-291251278Nessuna valutazione finora

- Chapter - IDocumento50 pagineChapter - IshahimermaidNessuna valutazione finora

- Risk Appetite Indexes: A Survey of MethodologiesDocumento7 pagineRisk Appetite Indexes: A Survey of MethodologiesDavid BudaghyanNessuna valutazione finora

- VolatilityDocumento280 pagineVolatilityRAMESHBABU100% (1)

- Security Analysis Is Primarily Concerned With The Analysis of A Security With A ViewDocumento4 pagineSecurity Analysis Is Primarily Concerned With The Analysis of A Security With A ViewarmailgmNessuna valutazione finora

- Stock Market Volatility FinalDocumento27 pagineStock Market Volatility FinalKhwaish PahwaNessuna valutazione finora

- International Forex Market Volatility An Empirical Study of 61 Global Currency PairsDocumento5 pagineInternational Forex Market Volatility An Empirical Study of 61 Global Currency PairsInternational Journal of Innovative Science and Research TechnologyNessuna valutazione finora

- An Institutional Theory of Momentum and Revealsal Rev. Financ. Stud.-2013-Vayanos-1087-145Documento59 pagineAn Institutional Theory of Momentum and Revealsal Rev. Financ. Stud.-2013-Vayanos-1087-145IGift WattanatornNessuna valutazione finora

- Global Shocks: An Investment Guide for Turbulent MarketsDa EverandGlobal Shocks: An Investment Guide for Turbulent MarketsNessuna valutazione finora

- Key Financial Terms and RatiosDocumento16 pagineKey Financial Terms and RatiosShravan KumarNessuna valutazione finora

- Wurgler Baker Investor SentimentDocumento23 pagineWurgler Baker Investor SentimentJohnathan WangNessuna valutazione finora

- Nvestors' Types of Behaviour During CrisisDocumento12 pagineNvestors' Types of Behaviour During Crisisdion.yanuarmawanNessuna valutazione finora

- Prospect Theory and Asset PricesDocumento38 pagineProspect Theory and Asset PricesAbdullah AlamNessuna valutazione finora

- Colegio Mayor de Nuestra Señora Del Rosario: International FinanceDocumento92 pagineColegio Mayor de Nuestra Señora Del Rosario: International FinanceDavid Alejandro RuizNessuna valutazione finora

- Illiquidity and Stock Returns - Cross-Section and Time-Series Effects - Yakov AmihudDocumento50 pagineIlliquidity and Stock Returns - Cross-Section and Time-Series Effects - Yakov AmihudKim PhượngNessuna valutazione finora

- Week 1 - Summary With Definitions and Graphs Week 1 - Summary With Definitions and GraphsDocumento16 pagineWeek 1 - Summary With Definitions and Graphs Week 1 - Summary With Definitions and GraphsRita GonçalvesNessuna valutazione finora

- Volatility CommoditiesDocumento10 pagineVolatility CommoditiesMarco PoloNessuna valutazione finora

- Bates Crash Risk MarketDocumento48 pagineBates Crash Risk Markettmp01@jesperlund.comNessuna valutazione finora

- MARKET EFFICIENCY AND ANOMALIESDocumento2 pagineMARKET EFFICIENCY AND ANOMALIESPrincess Joy Andayan BorangNessuna valutazione finora

- Literature Review On Currency DevaluationDocumento6 pagineLiterature Review On Currency Devaluationafmacfadbdwpmc100% (1)

- Stochastic Volatility Models Considerations for ActuariesDocumento35 pagineStochastic Volatility Models Considerations for ActuariesFrancisco López-HerreraNessuna valutazione finora

- Why The Excess VolatilityDocumento4 pagineWhy The Excess VolatilitysandeepvempatiNessuna valutazione finora

- When Does Investor Sentiment Predict Stock Returns?: San-Lin Chung, Chi-Hsiou Hung, and Chung-Ying YehDocumento40 pagineWhen Does Investor Sentiment Predict Stock Returns?: San-Lin Chung, Chi-Hsiou Hung, and Chung-Ying YehddkillerNessuna valutazione finora

- Rabin A Monetary Theory - 271 275Documento5 pagineRabin A Monetary Theory - 271 275Anonymous T2LhplUNessuna valutazione finora

- Putting Volatility To WorkDocumento8 paginePutting Volatility To WorkhotpariNessuna valutazione finora

- Investor Sentiment in The Stock Market: Malcolm Baker and Jeffrey WurglerDocumento23 pagineInvestor Sentiment in The Stock Market: Malcolm Baker and Jeffrey WurglerALEEM TEHSEENNessuna valutazione finora

- Carry Trades Currency CrashesDocumento36 pagineCarry Trades Currency CrasheswrknprgrsNessuna valutazione finora

- ErwtwexDocumento50 pagineErwtwexgoenshinNessuna valutazione finora

- Understanding Yield Curves and Interest Rate RisksDocumento15 pagineUnderstanding Yield Curves and Interest Rate RiskskevNessuna valutazione finora

- Buying and Selling Volatility - Connolly KevinDocumento218 pagineBuying and Selling Volatility - Connolly Kevinjshew_jr_junk100% (1)

- The Carry Trade and FundamentalsDocumento36 pagineThe Carry Trade and FundamentalsJean-Jacques RousseauNessuna valutazione finora

- How Market Illiquidity Affects Stock Returns Over TimeDocumento26 pagineHow Market Illiquidity Affects Stock Returns Over TimeAlexandre Berlanda CostaNessuna valutazione finora

- The Behavior of Taiwanese Investors in Asset Allocation: Apjba 3,1Documento13 pagineThe Behavior of Taiwanese Investors in Asset Allocation: Apjba 3,1clarinsdNessuna valutazione finora

- Objectives of Study 1. To Study and Understand The Concept of "Derivative Market" 2. To Know To Concept of Risk Management in ZephirumDocumento47 pagineObjectives of Study 1. To Study and Understand The Concept of "Derivative Market" 2. To Know To Concept of Risk Management in ZephirumRashid ShaikhNessuna valutazione finora

- SWING TRADING: Maximizing Returns and Minimizing Risk through Time-Tested Techniques and Tactics (2023 Guide for Beginners)Da EverandSWING TRADING: Maximizing Returns and Minimizing Risk through Time-Tested Techniques and Tactics (2023 Guide for Beginners)Nessuna valutazione finora

- Trading Implied Volatility: Extrinsiq Advanced Options Trading Guides, #4Da EverandTrading Implied Volatility: Extrinsiq Advanced Options Trading Guides, #4Valutazione: 4 su 5 stelle4/5 (1)

- Locked-In Range Analysis: Why Most Traders Must Lose Money in the Futures Market (Forex)Da EverandLocked-In Range Analysis: Why Most Traders Must Lose Money in the Futures Market (Forex)Valutazione: 1 su 5 stelle1/5 (1)

- Cost Sheet Preparation of Bangalore Iyangar BackeryDocumento6 pagineCost Sheet Preparation of Bangalore Iyangar BackeryAshish KotianNessuna valutazione finora

- Merger of Centurion Bank of Punjab & HDFCDocumento23 pagineMerger of Centurion Bank of Punjab & HDFCAshish Kotian100% (2)

- Mergers in Indian Banks: A Study on Mergers of HDFC Bank Ltd and Centurion Bank of Punjab LtdDocumento10 pagineMergers in Indian Banks: A Study on Mergers of HDFC Bank Ltd and Centurion Bank of Punjab LtdmehulraoNessuna valutazione finora

- Description Details: Minihelpdesk@met - EduDocumento1 paginaDescription Details: Minihelpdesk@met - EduAshish KotianNessuna valutazione finora

- Early Development in AmericaDocumento2 pagineEarly Development in AmericaAshish KotianNessuna valutazione finora

- HR JobDocumento1 paginaHR JobAshish KotianNessuna valutazione finora

- Creative Theatre: Searching For A-Z Finnest Tuning .? Your Search Ends HereDocumento31 pagineCreative Theatre: Searching For A-Z Finnest Tuning .? Your Search Ends HereAshish KotianNessuna valutazione finora

- MathDocumento251 pagineMathac1popova.4944Nessuna valutazione finora

- Capital BudgetingDocumento2 pagineCapital BudgetingSteven MalimbwiNessuna valutazione finora

- Promissory NotesDocumento3 paginePromissory NotesTrisha Mae BoholNessuna valutazione finora

- Ch.8 Preparation of Accounts From Incomplete RecordsDocumento22 pagineCh.8 Preparation of Accounts From Incomplete RecordsMalayaranjan PanigrahiNessuna valutazione finora

- Valuation of SecuritiesDocumento43 pagineValuation of SecuritiesVaidyanathan RavichandranNessuna valutazione finora

- Financial Liabilities - Bonds Payable - Practice Set (QUESTIONNAIRE)Documento4 pagineFinancial Liabilities - Bonds Payable - Practice Set (QUESTIONNAIRE)ashleydelmundo14Nessuna valutazione finora

- Chapter 5 Income Concepts MCQsDocumento6 pagineChapter 5 Income Concepts MCQsAbood FSNessuna valutazione finora

- FM Unit1.Documento166 pagineFM Unit1.shaik masoodNessuna valutazione finora

- 28 Comm 308 Final Exam (Winter 2016)Documento11 pagine28 Comm 308 Final Exam (Winter 2016)TejaNessuna valutazione finora

- Case Study AssignmentDocumento3 pagineCase Study AssignmentfalinaNessuna valutazione finora

- Valuing Bonds Yield Maturity CurrentDocumento12 pagineValuing Bonds Yield Maturity CurrentLaraNessuna valutazione finora

- 14 Deloitte Presentation 2 Slide Per PageDocumento46 pagine14 Deloitte Presentation 2 Slide Per PagemihailtomaNessuna valutazione finora

- SemiDocumento7 pagineSemiNanzNessuna valutazione finora

- Ent 300Documento13 pagineEnt 300Fawwaz ZawawiNessuna valutazione finora

- Lecture 4 INVESTMENT CRITERIA FOR PROJECT APPRAISALDocumento49 pagineLecture 4 INVESTMENT CRITERIA FOR PROJECT APPRAISALANH VÕ TỪNessuna valutazione finora

- Free Cash FlowsDocumento51 pagineFree Cash FlowsYagyaaGoyalNessuna valutazione finora

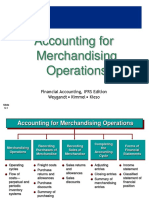

- Accounting For Merchandising Operations: Financial Accounting, IFRS Edition Weygandt Kimmel KiesoDocumento25 pagineAccounting For Merchandising Operations: Financial Accounting, IFRS Edition Weygandt Kimmel KiesoAndi Annisa DianputriNessuna valutazione finora

- Upstream Petroleum EconomicsDocumento17 pagineUpstream Petroleum Economicsjhon berez223344Nessuna valutazione finora

- Mathematics of Finance 8th Edition Brown Test BankDocumento112 pagineMathematics of Finance 8th Edition Brown Test BankLarryHicksetdrb100% (18)

- Numerical Problem of DividendDocumento8 pagineNumerical Problem of DividendShreya DikshitNessuna valutazione finora

- Solutions CH 14Documento63 pagineSolutions CH 14Abdalelah FrarjehNessuna valutazione finora

- BBC Ar Online 2009 10Documento101 pagineBBC Ar Online 2009 10Pornthep KamonpetchNessuna valutazione finora

- Pablo Fernández 80 Common Errors in Company Valuation IESE Business SchoolDocumento27 paginePablo Fernández 80 Common Errors in Company Valuation IESE Business SchoolFFNessuna valutazione finora

- Unit 4: Mathematics of FinanceDocumento34 pagineUnit 4: Mathematics of FinanceDawit MekonnenNessuna valutazione finora

- 28 Vasigh Erfani Aircraft ValueDocumento4 pagine28 Vasigh Erfani Aircraft ValueW.J. ZondagNessuna valutazione finora

- Chapter 6 RWJ FormulasDocumento71 pagineChapter 6 RWJ FormulasSanjna ChimnaniNessuna valutazione finora

- Financial Analysis: Alka Assistant Director Power System Training Institute BangaloreDocumento40 pagineFinancial Analysis: Alka Assistant Director Power System Training Institute Bangaloregaurang1111Nessuna valutazione finora

- Bond Tables Extend L 00 SPR A RichDocumento206 pagineBond Tables Extend L 00 SPR A RichMarcelo Lisciotto ZaninNessuna valutazione finora

- Chapter 5 Financial Forwards and FuturesDocumento16 pagineChapter 5 Financial Forwards and FutureshardrockerseanNessuna valutazione finora

- Calculating Bond Prices at Different YieldsDocumento25 pagineCalculating Bond Prices at Different YieldsMaybelle BernalNessuna valutazione finora