Potrebbero piacerti anche

- Vouching Summary NotesDocumento6 pagineVouching Summary NotesVikram KumarNessuna valutazione finora

- A. Key Internal Control B. Transaction Related Audit Objectives C. Test of Control D. Substantive Test of TransactionDocumento5 pagineA. Key Internal Control B. Transaction Related Audit Objectives C. Test of Control D. Substantive Test of TransactionRosanaDíazNessuna valutazione finora

- AUD02 - 02 Transaction CyclesDocumento54 pagineAUD02 - 02 Transaction CyclesMark BajacanNessuna valutazione finora

- Presentation Audit of Acquisition and Payment CycleDocumento38 paginePresentation Audit of Acquisition and Payment CycleSyaffiq UbaidillahNessuna valutazione finora

- Audit Of InventoriesDocumento22 pagineAudit Of InventoriesVaradan K RajendranNessuna valutazione finora

- Auditing CycleDocumento2 pagineAuditing CycletemedebereNessuna valutazione finora

- 2.1 Audit of Sales and ReceivablesDocumento2 pagine2.1 Audit of Sales and ReceivablesNavsNessuna valutazione finora

- Auditor's Response P2P CycleDocumento8 pagineAuditor's Response P2P CycleMarwin AceNessuna valutazione finora

- AEB15 SM C18 v3Documento33 pagineAEB15 SM C18 v3Aaqib Hossain100% (1)

- Audit of the Acquisition and Payment Cycle TestsDocumento11 pagineAudit of the Acquisition and Payment Cycle TestsChotimatul ChusnaaNessuna valutazione finora

- Chapter 4 Transaction CyclesDocumento24 pagineChapter 4 Transaction CyclesconsulivyNessuna valutazione finora

- Audit of Expenditure CycleDocumento5 pagineAudit of Expenditure CycleMa Tiffany Gura RobleNessuna valutazione finora

- Prof BullinaDocumento2 pagineProf BullinaAr-Reb AquinoNessuna valutazione finora

- Expenditure Cycle: Purchasing and DisbursementDocumento18 pagineExpenditure Cycle: Purchasing and DisbursementWenah TupasNessuna valutazione finora

- Revenue CycleDocumento10 pagineRevenue CycleMart BanaresNessuna valutazione finora

- GROUP 2: Audit of Expenditure Cycle: Tests of Controls and Substantive Tests of Transactions - I by CabreraDocumento3 pagineGROUP 2: Audit of Expenditure Cycle: Tests of Controls and Substantive Tests of Transactions - I by Cabreratankofdoom 4Nessuna valutazione finora

- TOC and Substantive Test Cyle Expenditure and Disbursement CycleDocumento6 pagineTOC and Substantive Test Cyle Expenditure and Disbursement CycleGirl langNessuna valutazione finora

- Chapter 10. Tests of ControlsDocumento25 pagineChapter 10. Tests of Controlsreeem312477Nessuna valutazione finora

- The Auditnet GuidesDocumento16 pagineThe Auditnet GuidesChinh Le DinhNessuna valutazione finora

- SVFC BS Accountancy1Documento29 pagineSVFC BS Accountancy1Lorraine TomasNessuna valutazione finora

- Audit Scope Accounts Involved Audit ProcedureDocumento12 pagineAudit Scope Accounts Involved Audit Procedurekarenmae intangNessuna valutazione finora

- Lab 3Documento10 pagineLab 3valen martaNessuna valutazione finora

- Audit II - CH 2-Student Notes, April, 2022Documento16 pagineAudit II - CH 2-Student Notes, April, 2022Abel ZewdeNessuna valutazione finora

- Jawaban Chapter 18Documento34 pagineJawaban Chapter 18Heltiana Nufriyanti75% (4)

- Purchase and Disbursement Cycle ControlsDocumento30 paginePurchase and Disbursement Cycle ControlsVenus Lyka LomocsoNessuna valutazione finora

- Process of Verification of Assets and Liabilities: by Amrutha S 122104183 Ii Bcom Cs - 1Documento15 pagineProcess of Verification of Assets and Liabilities: by Amrutha S 122104183 Ii Bcom Cs - 1amrutha subbiahNessuna valutazione finora

- Transaction Cycles Audit TestsDocumento8 pagineTransaction Cycles Audit TestsTrixie CasipleNessuna valutazione finora

- AUDIT PROGRAM For Cash Disbursements 2Documento5 pagineAUDIT PROGRAM For Cash Disbursements 2jezreel dela mercedNessuna valutazione finora

- Purchase Controls QuestionnaireDocumento3 paginePurchase Controls QuestionnaireMarieJoiaNessuna valutazione finora

- Lecture 9Documento33 pagineLecture 9lawlokyiNessuna valutazione finora

- Test Controls Transactions CyclesDocumento8 pagineTest Controls Transactions CyclesPatrick Joshua BreisNessuna valutazione finora

- Audit Accrued Expenses ProgramDocumento10 pagineAudit Accrued Expenses ProgramPutu Adi NugrahaNessuna valutazione finora

- Audit Programme for Trade PayablesDocumento5 pagineAudit Programme for Trade PayablesMiljane PerdizoNessuna valutazione finora

- Substantive Audit Receivables PDFDocumento23 pagineSubstantive Audit Receivables PDFnanabaNessuna valutazione finora

- Audit of Acquisition and Payment CycleDocumento30 pagineAudit of Acquisition and Payment CycleontykerlsNessuna valutazione finora

- Audit Program SalesDocumento4 pagineAudit Program SalesRhett SageNessuna valutazione finora

- Audit ProgramDocumento4 pagineAudit ProgramZoha KhaliqNessuna valutazione finora

- Synthesis - Auditprobfinalsss 1Documento35 pagineSynthesis - Auditprobfinalsss 1Thirdy MockyNessuna valutazione finora

- Transaction-Related Audit Objective Possible Internal Controls Common Tests of ControlsDocumento3 pagineTransaction-Related Audit Objective Possible Internal Controls Common Tests of ControlsJustin DavenportNessuna valutazione finora

- Specific Further Audit ProceduresDocumento4 pagineSpecific Further Audit ProceduresCattleyaNessuna valutazione finora

- Audit of Inventories: The Use of Assertions in Obtaining Audit EvidenceDocumento9 pagineAudit of Inventories: The Use of Assertions in Obtaining Audit EvidencemoNessuna valutazione finora

- Audit AssertionsDocumento1 paginaAudit AssertionsDevice Factory UnlockNessuna valutazione finora

- Audit of Expenditure Cycle TestsDocumento19 pagineAudit of Expenditure Cycle Teststankofdoom 4100% (1)

- Audit of The Revenue and Collection CycleDocumento5 pagineAudit of The Revenue and Collection CycleLalaine ReyesNessuna valutazione finora

- Acc117-Chapter 5Documento51 pagineAcc117-Chapter 5Fadilah JefriNessuna valutazione finora

- KELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditDocumento39 pagineKELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditAkuntansi 6511Nessuna valutazione finora

- AP 1901 Inventories PDFDocumento8 pagineAP 1901 Inventories PDFToni Rhys ArguellesNessuna valutazione finora

- Davita - Dewardani - 182321069 Tugas Pengauditan KeuanganDocumento4 pagineDavita - Dewardani - 182321069 Tugas Pengauditan KeuanganHAHAHA HIHIHINessuna valutazione finora

- AP.3401 Audit of InventoriesDocumento8 pagineAP.3401 Audit of InventoriesMonica GarciaNessuna valutazione finora

- Transaction Cycles - Test of Controls and Substantive Tests of TransactionsDocumento9 pagineTransaction Cycles - Test of Controls and Substantive Tests of TransactionsfeNessuna valutazione finora

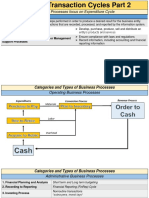

- AT 06-07 Transaction Cycles Part 2Documento12 pagineAT 06-07 Transaction Cycles Part 2EeuhNessuna valutazione finora

- Lab Iii Audit of Sales and Collection Cycle: I. TujuanDocumento8 pagineLab Iii Audit of Sales and Collection Cycle: I. TujuanyenitaNessuna valutazione finora

- 3.1 Audit of Purchases and PayablesDocumento1 pagina3.1 Audit of Purchases and PayablesNavsNessuna valutazione finora

- Audit Procedures for Accounts Receivable, Cash, InventoryDocumento2 pagineAudit Procedures for Accounts Receivable, Cash, InventoryRoseyy GalitNessuna valutazione finora

- Internal Check: C. P. Mansoor AhmedDocumento18 pagineInternal Check: C. P. Mansoor AhmedZohaib Ali ButtNessuna valutazione finora

- Revenue CycleDocumento7 pagineRevenue CycleArly Kurt TorresNessuna valutazione finora

- Control Activities Over Sales and ReceiptsDocumento2 pagineControl Activities Over Sales and ReceiptsKhyam Ahmed QaziNessuna valutazione finora

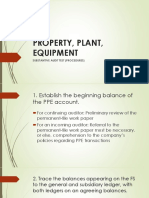

- PPE-Audit-ProceduresDocumento10 paginePPE-Audit-ProceduresjexNessuna valutazione finora

- ORDER NaufalDocumento5 pagineORDER NaufalFira aisyah meilaniNessuna valutazione finora

- Revealed From A Top Realtor: The Fastest Way To Sell Properties Like Crazy In Real Estate - Even If You Are A Complete NewbieDa EverandRevealed From A Top Realtor: The Fastest Way To Sell Properties Like Crazy In Real Estate - Even If You Are A Complete NewbieNessuna valutazione finora

- Hydroponics For KidsDocumento18 pagineHydroponics For KidsAjay GiriNessuna valutazione finora

- Science Fair - Hydroponics: Grow Plants Without SoilDocumento2 pagineScience Fair - Hydroponics: Grow Plants Without SoilAjay GiriNessuna valutazione finora

- Paper-9: Income Tax & AuditingDocumento15 paginePaper-9: Income Tax & AuditingAjay GiriNessuna valutazione finora

- Chapter 3Documento9 pagineChapter 3Ajay GiriNessuna valutazione finora

- How To Preapre For Exam-1Documento7 pagineHow To Preapre For Exam-1Ajay GiriNessuna valutazione finora

- 37 Powers and DutiesDocumento33 pagine37 Powers and DutiesAjay GiriNessuna valutazione finora

- How To Prepare Exam SubjectwiseDocumento5 pagineHow To Prepare Exam SubjectwiseAjay GiriNessuna valutazione finora

- Q. No - 2Documento12 pagineQ. No - 2Ajay GiriNessuna valutazione finora

- How To Preapre For Exam-1Documento7 pagineHow To Preapre For Exam-1Ajay GiriNessuna valutazione finora

- Q No - 1Documento6 pagineQ No - 1Ajay GiriNessuna valutazione finora

- Lease Financing (FM Assignment)Documento4 pagineLease Financing (FM Assignment)sameer_sheoran100% (1)

- OOM Schengen Visitor Insurance: Application FormDocumento3 pagineOOM Schengen Visitor Insurance: Application FormJoan RamirezNessuna valutazione finora

- Cma Tax PaperDocumento760 pagineCma Tax Paperritesh shrinewarNessuna valutazione finora

- Western Digital Financial AnalysisDocumento9 pagineWestern Digital Financial AnalysisblockeisuNessuna valutazione finora

- Binus Financial Analyst Academy CFA Program Level 1 Semester 2 Batch 34 2018 V4eDocumento5 pagineBinus Financial Analyst Academy CFA Program Level 1 Semester 2 Batch 34 2018 V4eBudiman SnowieNessuna valutazione finora

- Baye 9e Chapter 06Documento24 pagineBaye 9e Chapter 06Kevin Eka PutraNessuna valutazione finora

- Glencore 31 5 11Documento6 pagineGlencore 31 5 11Chandra ChadalawadaNessuna valutazione finora

- Sales Process Max NewDocumento67 pagineSales Process Max NewumeshrathoreNessuna valutazione finora

- MCQ Mba First YearDocumento164 pagineMCQ Mba First YearsachinNessuna valutazione finora

- Internal Control Manual (Brokerage House)Documento22 pagineInternal Control Manual (Brokerage House)hamzaaccaNessuna valutazione finora

- 356SDocumento256 pagine356SMian UsmanNessuna valutazione finora

- S - ALR - 87012284 - Financial Statements & Trial BalanceDocumento9 pagineS - ALR - 87012284 - Financial Statements & Trial Balancessrinivas64Nessuna valutazione finora

- JPM Russian Securities - Ordinary Shares (GB - EN) (03!09!2014)Documento4 pagineJPM Russian Securities - Ordinary Shares (GB - EN) (03!09!2014)Carl WellsNessuna valutazione finora

- The Curious Loan Approval Case AnalysisDocumento2 pagineThe Curious Loan Approval Case AnalysisIla Singh67% (6)

- Questionnaire ActDocumento6 pagineQuestionnaire ActLorainne AjocNessuna valutazione finora

- Padma Oil Jamuna Oil Ratio AnalysisDocumento17 paginePadma Oil Jamuna Oil Ratio AnalysisMd.mamunur Rashid0% (2)

- Market Strategy of Dabur HajmolaDocumento47 pagineMarket Strategy of Dabur HajmolaImran Khan50% (2)

- 03 IAS 36 SlidesDocumento34 pagine03 IAS 36 SlidesSuvro AvroNessuna valutazione finora

- 20180806qkv6b8 PDFDocumento33 pagine20180806qkv6b8 PDFMusa MohamadNessuna valutazione finora

- Internship Report On "General Banking & Foreign Exchange Activities of BASIC Bank Limited: A Study On Dilkusha Corporate BrunchDocumento88 pagineInternship Report On "General Banking & Foreign Exchange Activities of BASIC Bank Limited: A Study On Dilkusha Corporate BrunchRayhan Zahid HasanNessuna valutazione finora

- City of Utica DRI ApplicationDocumento88 pagineCity of Utica DRI ApplicationAnonymous LajAHHEENessuna valutazione finora

- Analysis of Home Loan in Bassein Catholic Co-Operative Bank Ltd. (Scheduled Bank)Documento58 pagineAnalysis of Home Loan in Bassein Catholic Co-Operative Bank Ltd. (Scheduled Bank)Nikhil BhaleraoNessuna valutazione finora

- Kohler CompanyDocumento3 pagineKohler CompanyDuncan BakerNessuna valutazione finora

- Panasonic vs. CIRDocumento6 paginePanasonic vs. CIRLeBron DurantNessuna valutazione finora

- Microsoft Vs Ford Data CaseDocumento7 pagineMicrosoft Vs Ford Data CaseFis MalesoriNessuna valutazione finora

- Financial Management CAPM ExerciseDocumento2 pagineFinancial Management CAPM ExerciseAMIRTHARAAJ A/L VIJAYAN MBS211063Nessuna valutazione finora

- Trading Rules and ProceduresDocumento20 pagineTrading Rules and ProceduresAmir Shahzad TararNessuna valutazione finora

- Tutorial 5 PDFDocumento2 pagineTutorial 5 PDFBarakaNessuna valutazione finora

- IAP1 OperationsDocumento7 pagineIAP1 OperationsromeoNessuna valutazione finora

- Mentor-on-the-Lake CRA OrdinanceDocumento6 pagineMentor-on-the-Lake CRA OrdinanceThe News-HeraldNessuna valutazione finora