Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- FM Butler Grup 2Documento10 pagineFM Butler Grup 2Anna Dewi Wijayanto100% (1)

- General Credit v. Alsons DigestDocumento2 pagineGeneral Credit v. Alsons Digestershaki100% (4)

- M3 - Gross Estate - Common Rules Students'Documento43 pagineM3 - Gross Estate - Common Rules Students'micaella pasionNessuna valutazione finora

- 03 Discounted Dividend ValuationDocumento55 pagine03 Discounted Dividend ValuationUmang PatelNessuna valutazione finora

- Cost Systems and Cost Accumulation: Multiple ChoiceDocumento26 pagineCost Systems and Cost Accumulation: Multiple ChoiceAdnan KhanNessuna valutazione finora

- Chart and Analysis - CompiledDocumento9 pagineChart and Analysis - Compiledmac mercado100% (1)

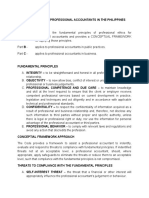

- Code of Ethics For Professional Accountants in The PhilippinesDocumento3 pagineCode of Ethics For Professional Accountants in The Philippinesmac mercadoNessuna valutazione finora

- NU Organization Incurred The Following Transactions Throughout The Academic Year 2016-2017Documento2 pagineNU Organization Incurred The Following Transactions Throughout The Academic Year 2016-2017mac mercadoNessuna valutazione finora

- Sol Ass3Documento5 pagineSol Ass3mac mercadoNessuna valutazione finora

- Interview and Observation To Acquire Dara Lack of System That Is AvailableDocumento1 paginaInterview and Observation To Acquire Dara Lack of System That Is Availablemac mercadoNessuna valutazione finora

- Strong Order Book Promises Revenue Growth: KNR's Healthy OrderDocumento10 pagineStrong Order Book Promises Revenue Growth: KNR's Healthy OrderNimesh PatelNessuna valutazione finora

- Activity 06 - Financial Statement PreparationDocumento4 pagineActivity 06 - Financial Statement PreparationMariz TiuNessuna valutazione finora

- Answer Any Four Questions. (4X6 24) : Time: 3 Hours Max. Marks:120Documento5 pagineAnswer Any Four Questions. (4X6 24) : Time: 3 Hours Max. Marks:120hanumanthaiahgowdaNessuna valutazione finora

- FR MCQ'sDocumento72 pagineFR MCQ'sMy KingdomNessuna valutazione finora

- Sec-A - Group 8 - SecureNowDocumento7 pagineSec-A - Group 8 - SecureNowPuneet GargNessuna valutazione finora

- Financial Analysis 2Documento2 pagineFinancial Analysis 2Sylvia GynNessuna valutazione finora

- Papers of Financial AccountingDocumento144 paginePapers of Financial AccountingnidamahNessuna valutazione finora

- Chapter 7: The Regular Output Vat Sources of Regular Output VATDocumento5 pagineChapter 7: The Regular Output Vat Sources of Regular Output VATArdee May BayaniNessuna valutazione finora

- Lesson 4 - Types and Costs of Financial CapitalDocumento18 pagineLesson 4 - Types and Costs of Financial CapitalChristel YeoNessuna valutazione finora

- Exercises Short ProblemsDocumento6 pagineExercises Short ProblemsKlaire SwswswsNessuna valutazione finora

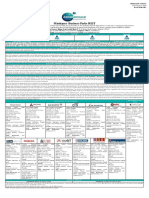

- Mindspace REIT Offer Document - 220720201425 PDFDocumento676 pagineMindspace REIT Offer Document - 220720201425 PDFsrihariNessuna valutazione finora

- Fina6000 Module 5 - Capital Structure BDocumento32 pagineFina6000 Module 5 - Capital Structure BMar SGNessuna valutazione finora

- The Nature of Accounting and Accounting Equation L1Documento23 pagineThe Nature of Accounting and Accounting Equation L1Charos Aslonovna75% (4)

- Revival Investments & Financial Solutions v1Documento13 pagineRevival Investments & Financial Solutions v1robitrevivalNessuna valutazione finora

- BeechyChap21 PDFDocumento51 pagineBeechyChap21 PDFkeo phommaNessuna valutazione finora

- Financing Decisions - Practice QuestionsDocumento3 pagineFinancing Decisions - Practice QuestionsAbrarNessuna valutazione finora

- Financial EconomicsDocumento18 pagineFinancial EconomicsvivianaNessuna valutazione finora

- NP & Debt Restructuring HO - 2064575149Documento3 pagineNP & Debt Restructuring HO - 2064575149JOHANNANessuna valutazione finora

- PTPPDocumento155 paginePTPPnaufalmuhammadNessuna valutazione finora

- 1 Manufacturing ExercisesDocumento3 pagine1 Manufacturing ExercisesRead this SecretNessuna valutazione finora

- FM MCQsDocumento74 pagineFM MCQsNidheena K SNessuna valutazione finora

- Financial Statement Tesco 2019 Horizontal AnalysisDocumento1 paginaFinancial Statement Tesco 2019 Horizontal Analysissuraj lamaNessuna valutazione finora

- 2018 Schindler Annual Report FB eDocumento136 pagine2018 Schindler Annual Report FB eKs BharathiyarNessuna valutazione finora

- IA2 Income TaxesDocumento1 paginaIA2 Income TaxesJoey Mhey BenicoNessuna valutazione finora

- Bharti Airtel LTD (BHARTI IN) - AdjustedDocumento4 pagineBharti Airtel LTD (BHARTI IN) - AdjustedDebarnob SarkarNessuna valutazione finora