Potrebbero piacerti anche

- Technical Indicators For Forex ForecastingDocumento11 pagineTechnical Indicators For Forex Forecastinghamed mokhtariNessuna valutazione finora

- Combining Trend and Oscillator SignalsDocumento11 pagineCombining Trend and Oscillator SignalsKoyasanNessuna valutazione finora

- Stock Deep Learning Paper FinalDocumento9 pagineStock Deep Learning Paper FinalKuldeep KumarNessuna valutazione finora

- An Application of Moving Average Convergence and Divergence (MACD) Indicator On Selected Stocks Listed On National Stock Exchange (NSE)Documento17 pagineAn Application of Moving Average Convergence and Divergence (MACD) Indicator On Selected Stocks Listed On National Stock Exchange (NSE)HemanthNessuna valutazione finora

- An Automated Trading System With Multi-Indicator Fusion Based On D-S Evidence Theory in Forex MarketDocumento5 pagineAn Automated Trading System With Multi-Indicator Fusion Based On D-S Evidence Theory in Forex MarketRohit SangralNessuna valutazione finora

- Refined MacdDocumento17 pagineRefined Macdapolodoro7Nessuna valutazione finora

- Class 2 Pattern RecognitionDocumento77 pagineClass 2 Pattern RecognitionYixing WNessuna valutazione finora

- ESM 644 Financial Management Dr. Hazim El-BazDocumento29 pagineESM 644 Financial Management Dr. Hazim El-Bazkhawla2789Nessuna valutazione finora

- Profitability of Oscillators Used in Technical Analysis For Financial MarketDocumento8 pagineProfitability of Oscillators Used in Technical Analysis For Financial MarketNikilesh MekaNessuna valutazione finora

- The Basis of Technical AnalysisDocumento7 pagineThe Basis of Technical AnalysisFranklin Aleyamma JoseNessuna valutazione finora

- Stock Trading Algorithm Using MACD, ROC, and Stochastic SignalsDocumento6 pagineStock Trading Algorithm Using MACD, ROC, and Stochastic Signalski_tsuketeNessuna valutazione finora

- Improving Stock Trend Prediction Using LSTM Neural Network Trained On A Complex Trading StrategyDocumento13 pagineImproving Stock Trend Prediction Using LSTM Neural Network Trained On A Complex Trading StrategyIJRASETPublicationsNessuna valutazione finora

- RanjitDocumento3 pagineRanjitRAHUL SHARMANessuna valutazione finora

- An Automatic Stock Trading System Using Particle Swarm Optimization (2017)Documento4 pagineAn Automatic Stock Trading System Using Particle Swarm Optimization (2017)Gonza NNessuna valutazione finora

- Forecasting of Security Prices Using Relative Strength Index 04.05.2015Documento21 pagineForecasting of Security Prices Using Relative Strength Index 04.05.2015Alexis TocquevilleNessuna valutazione finora

- Event-Driven LSTM For Forex Price PredictionDocumento7 pagineEvent-Driven LSTM For Forex Price Prediction岳佳Nessuna valutazione finora

- Gautam BlackbookDocumento93 pagineGautam BlackbookRio duttNessuna valutazione finora

- Various Moving Average Convergence Divergence TradDocumento8 pagineVarious Moving Average Convergence Divergence TradMiladEbrahimiNessuna valutazione finora

- p1851 PDFDocumento7 paginep1851 PDFingaleharshalNessuna valutazione finora

- Wayne A. Thorp - The MACD A Combo of Indicators For The Best of Both WorldsDocumento5 pagineWayne A. Thorp - The MACD A Combo of Indicators For The Best of Both WorldsShavya SharmaNessuna valutazione finora

- BEST INDICATORS FOR CRYPTOCURRENCY TRADINGDocumento8 pagineBEST INDICATORS FOR CRYPTOCURRENCY TRADINGUgo BenNessuna valutazione finora

- SaimDocumento7 pagineSaimNishtha SethNessuna valutazione finora

- Forex Trading Robot With Technical and FDocumento9 pagineForex Trading Robot With Technical and Falisalisu4446Nessuna valutazione finora

- Technical S AnalysisDocumento3 pagineTechnical S AnalysisSarvesh SinghNessuna valutazione finora

- Corporate Finance Technical AnalysisDocumento19 pagineCorporate Finance Technical AnalysisAvinash KumarNessuna valutazione finora

- Technical AnalysisDocumento17 pagineTechnical AnalysisHarsharaj MelantaNessuna valutazione finora

- Research Paper SMPDocumento5 pagineResearch Paper SMPDevashishGuptaNessuna valutazione finora

- Trendsin Stock MarketDocumento7 pagineTrendsin Stock MarketRahil KhanNessuna valutazione finora

- Using Hidden Markov Model For Stock Day Trade ForecastingDocumento12 pagineUsing Hidden Markov Model For Stock Day Trade ForecastingPatrick LangstromNessuna valutazione finora

- Research MethodologyDocumento5 pagineResearch Methodologysonal gargNessuna valutazione finora

- Indicator Soup: Enhance Your Technical Trading - September 2007 - by Darrell JobmanDocumento5 pagineIndicator Soup: Enhance Your Technical Trading - September 2007 - by Darrell JobmanLuisa HynesNessuna valutazione finora

- MACD Ebook PDFDocumento20 pagineMACD Ebook PDFegdejuana50% (2)

- Gaurav Bhagat CSE 5th SemDocumento8 pagineGaurav Bhagat CSE 5th SemGaurav BhagatNessuna valutazione finora

- Securities Analysis and Portfolio Management: Prices Usually Always Move in TrendsDocumento8 pagineSecurities Analysis and Portfolio Management: Prices Usually Always Move in TrendsStuti Jain100% (1)

- Trading Tactics in the Financial Market: Mathematical Methods to Improve PerformanceDa EverandTrading Tactics in the Financial Market: Mathematical Methods to Improve PerformanceNessuna valutazione finora

- Techinacl Anlysis Report of Task 1 &2Documento24 pagineTechinacl Anlysis Report of Task 1 &2Godha ManitejaNessuna valutazione finora

- Gautam Final BlackcookDocumento82 pagineGautam Final BlackcookRio duttNessuna valutazione finora

- Data in BriefDocumento7 pagineData in BriefJonNessuna valutazione finora

- Technical Analysis PDFDocumento11 pagineTechnical Analysis PDFlightbarqNessuna valutazione finora

- Technical Analysis PDF Free Guide DownloadDocumento9 pagineTechnical Analysis PDF Free Guide DownloadHevi EmmanuelNessuna valutazione finora

- An Intelligent Market Making Strategy in PDFDocumento13 pagineAn Intelligent Market Making Strategy in PDFLuca PilottiNessuna valutazione finora

- Top Forex Indicators To Use: Your Solution For Financial CongestionDocumento60 pagineTop Forex Indicators To Use: Your Solution For Financial CongestionKamoheloNessuna valutazione finora

- Technical Analysis PDFDocumento11 pagineTechnical Analysis PDFAdam ChoNessuna valutazione finora

- Folts PDFDocumento6 pagineFolts PDFThe_SunNessuna valutazione finora

- Technical Forex Trading by R. A. BensonDocumento2 pagineTechnical Forex Trading by R. A. BensonTrust FirmNessuna valutazione finora

- Technical Analysis MasterClass CheatSheet PDFDocumento14 pagineTechnical Analysis MasterClass CheatSheet PDFAman KumarNessuna valutazione finora

- Bachelor in Business Administration (Hons) FINANCE (BA242) : Future Trading Plan (FTP)Documento26 pagineBachelor in Business Administration (Hons) FINANCE (BA242) : Future Trading Plan (FTP)Muhammad FaizNessuna valutazione finora

- Indicators - The Best Technical Indicators For Digital TradingDocumento32 pagineIndicators - The Best Technical Indicators For Digital Tradingarsalan yavariNessuna valutazione finora

- What Is The Forex Technical Analysis?Documento37 pagineWhat Is The Forex Technical Analysis?funny079Nessuna valutazione finora

- PudiledowekizolefumDocumento2 paginePudiledowekizolefumkakaaNessuna valutazione finora

- An Intelligent Market Making Strategy in Algorithmic TradingDocumento14 pagineAn Intelligent Market Making Strategy in Algorithmic Tradingakshay12489Nessuna valutazione finora

- Jurnal 5 - MACDDocumento12 pagineJurnal 5 - MACDAhmad IrfanNessuna valutazione finora

- The PalmDocumento45 pagineThe PalmDarren_1986Nessuna valutazione finora

- How To Use Moving Average PDF GuideDocumento13 pagineHow To Use Moving Average PDF GuideNephiAlmarasDecaycoNessuna valutazione finora

- Research Article: Predicting Stock Price Trend Using MACD Optimized by Historical VolatilityDocumento13 pagineResearch Article: Predicting Stock Price Trend Using MACD Optimized by Historical VolatilityNnogge LovisNessuna valutazione finora

- TECHNICAL ANALYSIS FOR BEGINNERS: A Beginner's Guide to Mastering Technical Analysis (2024 Crash Course)Da EverandTECHNICAL ANALYSIS FOR BEGINNERS: A Beginner's Guide to Mastering Technical Analysis (2024 Crash Course)Nessuna valutazione finora

- The Strategic Technical Analysis of the Financial Markets: An All-Inclusive Guide to Trading Methods and ApplicationsDa EverandThe Strategic Technical Analysis of the Financial Markets: An All-Inclusive Guide to Trading Methods and ApplicationsNessuna valutazione finora

- News Release: Nomura Individual Investor SurveyDocumento17 pagineNews Release: Nomura Individual Investor Surveysatish sNessuna valutazione finora

- Simple Supper Trading SystemDocumento3 pagineSimple Supper Trading Systemsatish sNessuna valutazione finora

- 1208452Documento4 pagine1208452satish sNessuna valutazione finora

- The Stock Market Update: September 11, 2012 © David H. WeisDocumento1 paginaThe Stock Market Update: September 11, 2012 © David H. Weissatish sNessuna valutazione finora

- Es130617 1Documento4 pagineEs130617 1satish sNessuna valutazione finora

- Unusual Options Activity Halftime Report - : There Is A Risk of Loss in All TradingDocumento3 pagineUnusual Options Activity Halftime Report - : There Is A Risk of Loss in All Tradingsatish sNessuna valutazione finora

- Get More Out of Trading with PPO Indicator ManualDocumento4 pagineGet More Out of Trading with PPO Indicator Manualsatish sNessuna valutazione finora

- Crystal Structures. Miscellaneous Inorganic Compounds, Silicates, and Basic Structural InformationDocumento3 pagineCrystal Structures. Miscellaneous Inorganic Compounds, Silicates, and Basic Structural Informationsatish sNessuna valutazione finora

- ETF & Mutual Fund Rankings: All Cap Growth Style: Best & Worst FundsDocumento5 pagineETF & Mutual Fund Rankings: All Cap Growth Style: Best & Worst Fundssatish sNessuna valutazione finora

- Top 20 Day Trading Rules For SuccessDocumento4 pagineTop 20 Day Trading Rules For Successbugbugbugbug100% (3)

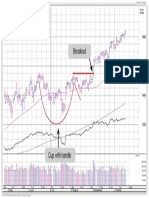

- Raschke0204 PDFDocumento10 pagineRaschke0204 PDFAnonymous xU5JHJe5Nessuna valutazione finora

- BattenBook Chapter7Enhanced PDFDocumento55 pagineBattenBook Chapter7Enhanced PDFsatish sNessuna valutazione finora

- Power PatternsDocumento41 paginePower Patternsedmond1100% (1)

- Sharpening Skills WyckoffDocumento16 pagineSharpening Skills Wyckoffsatish s100% (1)

- The Art of Timing The TradeDocumento1 paginaThe Art of Timing The Tradesatish s0% (3)

- Position SizingDocumento29 paginePosition SizingIan Moncrieffe94% (18)

- Wabash National Corp WNC: Last Close Fair Value Market CapDocumento4 pagineWabash National Corp WNC: Last Close Fair Value Market Capsatish sNessuna valutazione finora

- Greatness SurveyDocumento14 pagineGreatness SurveyNew York PostNessuna valutazione finora

- Pega 7 1 Sla1Documento3 paginePega 7 1 Sla1satish sNessuna valutazione finora

- Forecasting Stock Returns: What Signals Matter, and What Do They Say Now?Documento20 pagineForecasting Stock Returns: What Signals Matter, and What Do They Say Now?dabiel straumannNessuna valutazione finora

- CH 4Documento38 pagineCH 4satish sNessuna valutazione finora

- Receiving, Inspection, Acceptance Testing and Acceptance or Rejection ProcessesDocumento18 pagineReceiving, Inspection, Acceptance Testing and Acceptance or Rejection ProcessesjeswinNessuna valutazione finora

- How To Buy Common Patterns1 2Documento1 paginaHow To Buy Common Patterns1 2satish sNessuna valutazione finora

- Uniti Group Inc UNIT: Last Close Fair Value Market CapDocumento4 pagineUniti Group Inc UNIT: Last Close Fair Value Market Capsatish sNessuna valutazione finora

- Trading by Quantum Rules - Quantum Anthropic Principle: Ep@alpha - Uwb.edu - PLDocumento8 pagineTrading by Quantum Rules - Quantum Anthropic Principle: Ep@alpha - Uwb.edu - PLsatish sNessuna valutazione finora

- Money Management Controlling Risk and Capturing Profits by Dave LandryDocumento20 pagineMoney Management Controlling Risk and Capturing Profits by Dave LandryRxCapeNessuna valutazione finora

- Kuhn FEMADocumento1 paginaKuhn FEMAsatish sNessuna valutazione finora

- Greenhill & Co Inc GHL: DividendsDocumento5 pagineGreenhill & Co Inc GHL: Dividendssatish sNessuna valutazione finora

- Smartbuild - Smart Design For Smart SystemsDocumento1 paginaSmartbuild - Smart Design For Smart Systemssatish sNessuna valutazione finora

- LC37D90Documento208 pagineLC37D90Piter De AzizNessuna valutazione finora

- ZAAA x32 Ironman SK (ZAA) & Captain SK (ZAAA) MB 6L E Version PDFDocumento48 pagineZAAA x32 Ironman SK (ZAA) & Captain SK (ZAAA) MB 6L E Version PDFSebastian StanacheNessuna valutazione finora

- Post Test Principles of TeachingDocumento8 paginePost Test Principles of TeachingGibriel SllerNessuna valutazione finora

- SML Lab ManuelDocumento24 pagineSML Lab Manuelnavin rathiNessuna valutazione finora

- F-RPO-02A Research Protocol AssessmentDocumento4 pagineF-RPO-02A Research Protocol AssessmentEuniece CepilloNessuna valutazione finora

- Manufacturing KPI Dashboard Someka Excel Template V3 Free VersionDocumento11 pagineManufacturing KPI Dashboard Someka Excel Template V3 Free VersionYoro Diallo50% (2)

- DJVUDocumento2 pagineDJVUEric FansiNessuna valutazione finora

- Justin Bieber 'Agrees To Fight Tom Cruise' in An Unbelievable UFC Hollywood ShowdownDocumento180 pagineJustin Bieber 'Agrees To Fight Tom Cruise' in An Unbelievable UFC Hollywood ShowdownRyukendo KenjiNessuna valutazione finora

- Ansi Ieee C37.101 19931Documento60 pagineAnsi Ieee C37.101 19931Wilmar Andres Martinez100% (1)

- Online Motorcycle Taxis Speed You to ConcertsDocumento12 pagineOnline Motorcycle Taxis Speed You to ConcertsYudi Pujiadi100% (1)

- Oracle WDP GuideDocumento5 pagineOracle WDP GuidePrashant PrakashNessuna valutazione finora

- Deploy Specific Packages in SSISDocumento114 pagineDeploy Specific Packages in SSISmachi418Nessuna valutazione finora

- Kerem Kemik CV - Family Doctor ProfileDocumento3 pagineKerem Kemik CV - Family Doctor ProfileKerem KemikNessuna valutazione finora

- Uvm Cookbook CollectionDocumento54 pagineUvm Cookbook CollectionQuý Trương QuangNessuna valutazione finora

- Buyside Risk Management SystemsDocumento16 pagineBuyside Risk Management SystemsjosephmeawadNessuna valutazione finora

- Test Sample 1 - May 30 2020 Easergy P3U30 Settings Report 2020-05-30 14 - 43 - 09Documento255 pagineTest Sample 1 - May 30 2020 Easergy P3U30 Settings Report 2020-05-30 14 - 43 - 09jobpei2Nessuna valutazione finora

- Transmission Line Parameter CalculationDocumento12 pagineTransmission Line Parameter Calculationksg9731100% (4)

- A Comparative Study On Machine Learning Techniques Using Titanic DatasetDocumento6 pagineA Comparative Study On Machine Learning Techniques Using Titanic Datasetfitoj akaNessuna valutazione finora

- Hacking Module 11Documento53 pagineHacking Module 11Chye HengNessuna valutazione finora

- 2014 Cascadia - 2Documento3 pagine2014 Cascadia - 2Kirk Easom100% (1)

- DosBox Manual by Howling Mad Murdock 1.9aDocumento23 pagineDosBox Manual by Howling Mad Murdock 1.9alindseysmith999Nessuna valutazione finora

- Cmu-4000 Og 5230790130Documento74 pagineCmu-4000 Og 5230790130roshan mungurNessuna valutazione finora

- i5/OS Commands ExplainedDocumento18 paginei5/OS Commands Explainedrachmat99Nessuna valutazione finora

- 8085 InteruptsDocumento13 pagine8085 InteruptsAsawari DudwadkarNessuna valutazione finora

- 5 BM-03 Composite Function BM-03 Worksheet-02Documento4 pagine5 BM-03 Composite Function BM-03 Worksheet-02Marcus Maccoy AcordaNessuna valutazione finora

- Honeypot Base PaperDocumento9 pagineHoneypot Base PaperGuraja Sai AbhishekNessuna valutazione finora

- Project Proposal Business Presentation in Dark Blue Pink Abstract Tech StyleDocumento17 pagineProject Proposal Business Presentation in Dark Blue Pink Abstract Tech StyleAbel TayeNessuna valutazione finora

- Oilfield Equipment Manual Connection and SealingDocumento28 pagineOilfield Equipment Manual Connection and SealingIgor Ungur100% (2)

- SDPB ManualDocumento14 pagineSDPB ManualAaron HillmanNessuna valutazione finora

- Analytical Fleet Maintenance Management: 3rd EditionDocumento1 paginaAnalytical Fleet Maintenance Management: 3rd EditionAnas R. Abu KashefNessuna valutazione finora