Potrebbero piacerti anche

- New Classical EconomicsssDocumento12 pagineNew Classical Economicsssfilip.porebski69Nessuna valutazione finora

- Cases in Economic Development: Projects, Policies and StrategiesDa EverandCases in Economic Development: Projects, Policies and StrategiesValutazione: 3 su 5 stelle3/5 (1)

- pricingWPM3 PDFDocumento78 paginepricingWPM3 PDFNicusor DragoiuNessuna valutazione finora

- Bureaucratic Failure and Public ExpenditureDa EverandBureaucratic Failure and Public ExpenditureNessuna valutazione finora

- 1757 - Islamic BankingDocumento38 pagine1757 - Islamic BankinghammadNessuna valutazione finora

- A Bank Asset and Liability (Kiemba, 1983)Documento60 pagineA Bank Asset and Liability (Kiemba, 1983)BrunéNessuna valutazione finora

- Fundamentals of Public Relations: Professional Guidelines, Concepts and IntegrationsDa EverandFundamentals of Public Relations: Professional Guidelines, Concepts and IntegrationsValutazione: 4.5 su 5 stelle4.5/5 (2)

- External Debt of States Concept, Structure, IndicatorsDocumento14 pagineExternal Debt of States Concept, Structure, IndicatorslidibarvNessuna valutazione finora

- Global Financial CrisisDocumento47 pagineGlobal Financial CrisisArul DassNessuna valutazione finora

- b10086031 PDFDocumento172 pagineb10086031 PDFCarlosNessuna valutazione finora

- Burlington EconomyDocumento13 pagineBurlington EconomyChuck MorseNessuna valutazione finora

- Will The Dow Reach 30000 by 2015 0809Documento8 pagineWill The Dow Reach 30000 by 2015 0809Andre SilvaNessuna valutazione finora

- Merger Is Defined As The Combination of Two RelativelyDocumento16 pagineMerger Is Defined As The Combination of Two RelativelyPawar SachinNessuna valutazione finora

- Trade and Economic DevelopmentDocumento18 pagineTrade and Economic DevelopmentFridayNessuna valutazione finora

- Sistemas de Innovación: Una Comparación Entre Japón Y México'Documento32 pagineSistemas de Innovación: Una Comparación Entre Japón Y México'JavierDhi MBNessuna valutazione finora

- 07 - Chapter 1Documento39 pagine07 - Chapter 1Geetha SaranyaNessuna valutazione finora

- The Corporate Governance of BanksDocumento56 pagineThe Corporate Governance of BankspriyankafreshNessuna valutazione finora

- 10.7312 Dahl91482-001Documento2 pagine10.7312 Dahl91482-001Amee KananiNessuna valutazione finora

- Entrepreneurship DevelopmentDocumento10 pagineEntrepreneurship DevelopmentSanjay shuklaNessuna valutazione finora

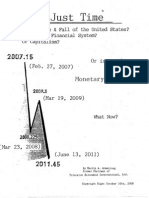

- Its Just Time Martin ArmstrongDocumento77 pagineIts Just Time Martin ArmstrongMarty MahNessuna valutazione finora

- Theories of Strategic PlanningDocumento36 pagineTheories of Strategic Planningjoseph ronillo virayNessuna valutazione finora

- Can Chinese Companies Live Up To Investor ExpectationsDocumento7 pagineCan Chinese Companies Live Up To Investor ExpectationsSrinivas RaghavanNessuna valutazione finora

- DC History Shaw MiccoNews MLKDocumento3 pagineDC History Shaw MiccoNews MLKMm InshawNessuna valutazione finora

- HRA CHR IV A2010 005 EO No.003 Discriminatory or Rights Based CHR Advisory On The Local Ordinance by The City of ManilaDocumento5 pagineHRA CHR IV A2010 005 EO No.003 Discriminatory or Rights Based CHR Advisory On The Local Ordinance by The City of ManilaKal-El Von Li YapNessuna valutazione finora

- 1 Paul R. Krugman, Maurice Obstfeld - International Economics - Theory and Policy (8th Edition) (2009) - 29-37Documento9 pagine1 Paul R. Krugman, Maurice Obstfeld - International Economics - Theory and Policy (8th Edition) (2009) - 29-37Khairunnisa ArdhiNessuna valutazione finora

- Health Care Industry External AnalysisDocumento12 pagineHealth Care Industry External AnalysisJa RedNessuna valutazione finora

- Accounting and The Construction of The Governable PersonDocumento31 pagineAccounting and The Construction of The Governable PersonPascalis HwangNessuna valutazione finora

- This SchemeDocumento9 pagineThis Schemeshashi shekhar dixitNessuna valutazione finora

- Burlington's Unbriddled GrowthDocumento14 pagineBurlington's Unbriddled GrowthChuck MorseNessuna valutazione finora

- What The Age Composition of Migrants Can Tell Us (1982)Documento36 pagineWhat The Age Composition of Migrants Can Tell Us (1982)Luis Javier CastroNessuna valutazione finora

- Gold Commission Report Annex CDocumento6 pagineGold Commission Report Annex Crangak2004Nessuna valutazione finora

- Aos93-991611991 (VERA)Documento7 pagineAos93-991611991 (VERA)Jeffri SuhendarNessuna valutazione finora

- 198420Documento16 pagine198420Nadia DivandraNessuna valutazione finora

- Spectre of InflationDocumento3 pagineSpectre of InflationBalasubramanian BhaskaranNessuna valutazione finora

- British Leyland: What The Prime Minister Thought.Documento123 pagineBritish Leyland: What The Prime Minister Thought.danielharrison1100% (2)

- SkyTrain, WCE 2015 Business PlanDocumento22 pagineSkyTrain, WCE 2015 Business PlanBob MackinNessuna valutazione finora

- Reactive Power Generation and Control by Thyristor CircuitsDocumento11 pagineReactive Power Generation and Control by Thyristor Circuitsrakeshee2007Nessuna valutazione finora

- 22 Financial Management TheoryDocumento109 pagine22 Financial Management TheoryVinay BabuNessuna valutazione finora

- Budgetary Control and Organizational PersonsDocumento12 pagineBudgetary Control and Organizational PersonsPatrick P. ParconNessuna valutazione finora

- "Grameen Bank in India How Helpful ItDocumento74 pagine"Grameen Bank in India How Helpful ItVipul TandonNessuna valutazione finora

- Rosicrucian Manual (1918) .Documento40 pagineRosicrucian Manual (1918) .Lagduf100% (2)

- A Reasonable Method To Estimate Lossof Labor Productivity Dueto OvertimeDocumento11 pagineA Reasonable Method To Estimate Lossof Labor Productivity Dueto OvertimeEmadNessuna valutazione finora

- Methods.: W A S Dependent UponDocumento4 pagineMethods.: W A S Dependent UponirhamsyahNessuna valutazione finora

- CH 10 Metall Flowsheet DVPMNTDocumento18 pagineCH 10 Metall Flowsheet DVPMNTxchadxNessuna valutazione finora

- Handbook On Housing - FSI - Crowding - Densities PDFDocumento53 pagineHandbook On Housing - FSI - Crowding - Densities PDFSaloni MishuNessuna valutazione finora

- Isaak Illich Rubin-Essays On Marx's Theory of ValueDocumento301 pagineIsaak Illich Rubin-Essays On Marx's Theory of Valuehegelhegel100% (1)

- LICMF Monthly Income Plan (Earlier Dhanavarsha - 12) : An Open Ended Income Scheme With No Assured ReturnsDocumento4 pagineLICMF Monthly Income Plan (Earlier Dhanavarsha - 12) : An Open Ended Income Scheme With No Assured ReturnsSaptha GiriNessuna valutazione finora

- Mathematics of Relativity Lecture NotesDocumento141 pagineMathematics of Relativity Lecture Notesmaese_obsesivoNessuna valutazione finora

- Jean Baudrillard - World Debt and Parallel UniverseDocumento5 pagineJean Baudrillard - World Debt and Parallel Universeakrobata1100% (1)

- International Federation of Red Cross and Red Crescent SocietiesDocumento23 pagineInternational Federation of Red Cross and Red Crescent SocietiesJoumana Ben YounesNessuna valutazione finora

- University of California, San DiegoDocumento24 pagineUniversity of California, San DiegoStevensNessuna valutazione finora

- 1968-02-28 The Enterprise RomanDocumento24 pagine1968-02-28 The Enterprise RomanRomulus Historical NewspapersNessuna valutazione finora

- Management FunctionDocumento8 pagineManagement FunctionCHLOE WONGNessuna valutazione finora

- What Is Global Governance? (Lawrence Finkelstein)Documento6 pagineWhat Is Global Governance? (Lawrence Finkelstein)Mayrlon CarlosNessuna valutazione finora

- Creating Strategic WindowsDocumento7 pagineCreating Strategic WindowsDhawal RathorNessuna valutazione finora

- Angle Hole Drilling With Large Blast Hole Drills: So That The Form in Which It Appears Here Is Not NecessarilyDocumento7 pagineAngle Hole Drilling With Large Blast Hole Drills: So That The Form in Which It Appears Here Is Not NecessarilyAlexis MaronNessuna valutazione finora

- Acct1-Reference1-Chapter 1 PDFDocumento16 pagineAcct1-Reference1-Chapter 1 PDFPaul Brian BumanlagNessuna valutazione finora

- O' Connor, James. La Crisis Fiscal Del Estado. Ediciones Península. 1994. Introducción.Documento44 pagineO' Connor, James. La Crisis Fiscal Del Estado. Ediciones Península. 1994. Introducción.Joan Díaz100% (1)

- Portfolio Credit RiskDocumento37 paginePortfolio Credit RisksgjatharNessuna valutazione finora

- BCBS239 - A Roadmap For Data Governance - 04202016Documento40 pagineBCBS239 - A Roadmap For Data Governance - 04202016sgjathar100% (3)

- Prudential Norms IracDocumento26 paginePrudential Norms IracsgjatharNessuna valutazione finora

- Insolvency and Bankruptcy Board of India 7 Floor, Mayur Bhawan, Connaught Place, New Delhi-110001 CircularDocumento3 pagineInsolvency and Bankruptcy Board of India 7 Floor, Mayur Bhawan, Connaught Place, New Delhi-110001 CircularsgjatharNessuna valutazione finora

- Biograph of CTO PDFDocumento2 pagineBiograph of CTO PDFsgjatharNessuna valutazione finora

- IGNOU PHD Information BrochureDocumento62 pagineIGNOU PHD Information BrochuresgjatharNessuna valutazione finora

- AnaCredit Manual Part II Datasets and Data Attributes - enDocumento275 pagineAnaCredit Manual Part II Datasets and Data Attributes - ensgjatharNessuna valutazione finora

- Blockchain:: A Revolutionary Change or Not?Documento6 pagineBlockchain:: A Revolutionary Change or Not?sgjatharNessuna valutazione finora

- Bob Disclosure March 2016Documento36 pagineBob Disclosure March 2016sgjatharNessuna valutazione finora

- AnaCredit Manual Part III Case Studies - enDocumento124 pagineAnaCredit Manual Part III Case Studies - ensgjatharNessuna valutazione finora

- psl12 PDFDocumento2 paginepsl12 PDFsgjatharNessuna valutazione finora

- Annual Report 2001-02Documento41 pagineAnnual Report 2001-02sgjatharNessuna valutazione finora

- Bob Basel 3 Pillar 3 DisclosuresDocumento36 pagineBob Basel 3 Pillar 3 DisclosuressgjatharNessuna valutazione finora

- National Housing Bank: Annual ReportDocumento31 pagineNational Housing Bank: Annual ReportsgjatharNessuna valutazione finora

- Training Programme For Housing Finance Companies NewdelhiDocumento1 paginaTraining Programme For Housing Finance Companies NewdelhisgjatharNessuna valutazione finora

- International Financial Regulation: The Quiet RevolutionDocumento15 pagineInternational Financial Regulation: The Quiet RevolutionsgjatharNessuna valutazione finora

- Report On Trend & Progress of Housing in India, June 2002Documento56 pagineReport On Trend & Progress of Housing in India, June 2002sgjatharNessuna valutazione finora

- Grp15 Entrep ReflectionDocumento9 pagineGrp15 Entrep ReflectionFaker MejiaNessuna valutazione finora

- Jaipur National University: Dainik Bhaskar Jid Karo Duniya BadloDocumento33 pagineJaipur National University: Dainik Bhaskar Jid Karo Duniya BadloAkkivjNessuna valutazione finora

- Calculation of Depreciation As Per Income Tax ActDocumento12 pagineCalculation of Depreciation As Per Income Tax Act24.7upskill Lakshmi V100% (1)

- Director Ecommerce Software Development in United States Resume Brendan MoranDocumento2 pagineDirector Ecommerce Software Development in United States Resume Brendan MoranBrendan MoranNessuna valutazione finora

- Generating Revenue and Economic DevelopmentDocumento6 pagineGenerating Revenue and Economic DevelopmentialnabahinNessuna valutazione finora

- 79MW Solar Cash Flow enDocumento1 pagina79MW Solar Cash Flow enBrian Moyo100% (1)

- ReportDocumento34 pagineReportTahirish Abbasi50% (2)

- An Introduction To The Supply Chain Council's SCOR MethodologyDocumento17 pagineAn Introduction To The Supply Chain Council's SCOR MethodologyLuis Andres Clavel Diaz100% (1)

- Child Care Business PlanDocumento15 pagineChild Care Business Plandeepakpinksurat100% (5)

- Kantar Asia Brand Footprint 2020 Final enDocumento81 pagineKantar Asia Brand Footprint 2020 Final enThi TranNessuna valutazione finora

- IFI Banking TranscriptDocumento21 pagineIFI Banking TranscriptAnonymous NeRBrZyAUbNessuna valutazione finora

- Executive SummaryDocumento56 pagineExecutive Summarybooksstrategy100% (1)

- Tax Planning CasesDocumento68 pagineTax Planning CasesHomework PingNessuna valutazione finora

- Money in The Nation's EconomyDocumento18 pagineMoney in The Nation's EconomyAnne Gatchalian67% (3)

- D4Documento6 pagineD4crap talkNessuna valutazione finora

- Ian Marcouse - Marie Brewer - Andrew Hammond - AQA Business Studies For AS - Revision Guide-Hodder Education (2010)Documento127 pagineIan Marcouse - Marie Brewer - Andrew Hammond - AQA Business Studies For AS - Revision Guide-Hodder Education (2010)Talisson BonfimNessuna valutazione finora

- BSBSUS211 - Assessment Task 1Documento7 pagineBSBSUS211 - Assessment Task 1Anzel Anzel100% (1)

- Agreement JHT GLOBAL SDN BHDDocumento2 pagineAgreement JHT GLOBAL SDN BHDadynamicglobalNessuna valutazione finora

- This Agreement, Was Made in 24/02/2021 Between:: Unified Employment ContractDocumento9 pagineThis Agreement, Was Made in 24/02/2021 Between:: Unified Employment ContractMajdy Al harbiNessuna valutazione finora

- Crompton Greaves FansDocumento1 paginaCrompton Greaves FansKushal AkbariNessuna valutazione finora

- Pinku 123Documento91 paginePinku 123bharat sachdevaNessuna valutazione finora

- Understanding Results Analysis For WIP: Introduction and Configuration GuideDocumento3 pagineUnderstanding Results Analysis For WIP: Introduction and Configuration GuidegildlreiNessuna valutazione finora

- GRIR Leading Practices v3Documento5 pagineGRIR Leading Practices v3Shabnam MacanmakerNessuna valutazione finora

- Mahila Samman Savings Certificate 2023 - FAQsDocumento3 pagineMahila Samman Savings Certificate 2023 - FAQsketanaurangabad3733Nessuna valutazione finora

- Economic Analysis For ManagersDocumento6 pagineEconomic Analysis For ManagersSaad NiaziNessuna valutazione finora

- Introduction To Predictive Analytics: FICO Solutions EducationDocumento51 pagineIntroduction To Predictive Analytics: FICO Solutions EducationSumit RampuriaNessuna valutazione finora

- The Evolution of Professional SellingDocumento4 pagineThe Evolution of Professional SellingSabaNessuna valutazione finora

- Abrams Company Case Study - MADocumento2 pagineAbrams Company Case Study - MAMuhammad Zakky AlifNessuna valutazione finora

- George Oakes LTD: GOL Online StoreDocumento3 pagineGeorge Oakes LTD: GOL Online StoreSatishElReyNessuna valutazione finora

- Student Declaration: I, Mohit Yadav Student of MBA IV From DIMS, Meerut Here by Declares That The ProjectDocumento104 pagineStudent Declaration: I, Mohit Yadav Student of MBA IV From DIMS, Meerut Here by Declares That The ProjectSumbal JameelNessuna valutazione finora

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisDa EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisValutazione: 5 su 5 stelle5/5 (6)

- Creating Shareholder Value: A Guide For Managers And InvestorsDa EverandCreating Shareholder Value: A Guide For Managers And InvestorsValutazione: 4.5 su 5 stelle4.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDa EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaValutazione: 4.5 su 5 stelle4.5/5 (14)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNDa Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNValutazione: 4.5 su 5 stelle4.5/5 (3)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingDa EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingValutazione: 4.5 su 5 stelle4.5/5 (17)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialDa EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialValutazione: 4.5 su 5 stelle4.5/5 (32)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDa EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaValutazione: 3.5 su 5 stelle3.5/5 (8)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthDa EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthValutazione: 4 su 5 stelle4/5 (20)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelDa Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNessuna valutazione finora

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursDa EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursValutazione: 4.5 su 5 stelle4.5/5 (8)

- Value: The Four Cornerstones of Corporate FinanceDa EverandValue: The Four Cornerstones of Corporate FinanceValutazione: 4.5 su 5 stelle4.5/5 (18)

- Finance Basics (HBR 20-Minute Manager Series)Da EverandFinance Basics (HBR 20-Minute Manager Series)Valutazione: 4.5 su 5 stelle4.5/5 (32)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamDa EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNessuna valutazione finora

- Mind over Money: The Psychology of Money and How to Use It BetterDa EverandMind over Money: The Psychology of Money and How to Use It BetterValutazione: 4 su 5 stelle4/5 (24)

- Financial Risk Management: A Simple IntroductionDa EverandFinancial Risk Management: A Simple IntroductionValutazione: 4.5 su 5 stelle4.5/5 (7)

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsDa EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsValutazione: 5 su 5 stelle5/5 (1)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsDa EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsNessuna valutazione finora

- Product-Led Growth: How to Build a Product That Sells ItselfDa EverandProduct-Led Growth: How to Build a Product That Sells ItselfValutazione: 5 su 5 stelle5/5 (1)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Da EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Valutazione: 4 su 5 stelle4/5 (5)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistDa EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistValutazione: 4 su 5 stelle4/5 (32)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursDa EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursValutazione: 4.5 su 5 stelle4.5/5 (34)

- How to Measure Anything: Finding the Value of Intangibles in BusinessDa EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessValutazione: 3.5 su 5 stelle3.5/5 (4)

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondDa EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondNessuna valutazione finora