Potrebbero piacerti anche

- 1209 Household Del Ever Aging DynanDocumento23 pagine1209 Household Del Ever Aging Dynanrichardck50Nessuna valutazione finora

- Breakfast With Dave 010511Documento15 pagineBreakfast With Dave 010511richardck50Nessuna valutazione finora

- Breakfast With Dave 122010Documento8 pagineBreakfast With Dave 122010richardck50Nessuna valutazione finora

- Breakfast With Dave 122310Documento9 pagineBreakfast With Dave 122310richardck50Nessuna valutazione finora

- Mwo 121010Documento10 pagineMwo 121010richardck50Nessuna valutazione finora

- Economics and National SecurityDocumento26 pagineEconomics and National Securityrichardck50Nessuna valutazione finora

- Breakfast With Dave 110210Documento5 pagineBreakfast With Dave 110210richardck50Nessuna valutazione finora

- GSA SanfranpresentationDocumento13 pagineGSA Sanfranpresentationrichardck50Nessuna valutazione finora

- Lunch With Dave 121010Documento9 pagineLunch With Dave 121010richardck50Nessuna valutazione finora

- Breakfast With Dave 112210Documento15 pagineBreakfast With Dave 112210richardck50Nessuna valutazione finora

- The Moment of Truth - Report of The National Commission On Fiscal Responsibility and ReformDocumento59 pagineThe Moment of Truth - Report of The National Commission On Fiscal Responsibility and ReformForeclosure FraudNessuna valutazione finora

- Breakfast With Dave 20100928Documento8 pagineBreakfast With Dave 20100928marketpanicNessuna valutazione finora

- Lunch With Dave 120710Documento16 pagineLunch With Dave 120710richardck50Nessuna valutazione finora

- Breakfast With Dave 111110Documento9 pagineBreakfast With Dave 111110richardck50Nessuna valutazione finora

- Japanese Monetary Policy: A Case of Self-Induced Paralysis?Documento27 pagineJapanese Monetary Policy: A Case of Self-Induced Paralysis?richardck50Nessuna valutazione finora

- Asset Allocation: Fall 2010: Olume CtoberDocumento30 pagineAsset Allocation: Fall 2010: Olume Ctoberrichardck50Nessuna valutazione finora

- The German Mark Had Significant Rallies On Its Way To Zero: Continental Capital Advisors, LLC October 29, 2010Documento2 pagineThe German Mark Had Significant Rallies On Its Way To Zero: Continental Capital Advisors, LLC October 29, 2010richardck50Nessuna valutazione finora

- Third Q Uarter R Eport 2010Documento16 pagineThird Q Uarter R Eport 2010richardck50Nessuna valutazione finora

- Oct 2110Documento2 pagineOct 2110richardck50Nessuna valutazione finora

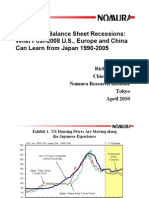

- NOMURA Research PresentationDocumento27 pagineNOMURA Research PresentationSantiago Cueto100% (1)

- Government Policy and The Markets:: Prepare For Some Big ChangesDocumento22 pagineGovernment Policy and The Markets:: Prepare For Some Big Changesrichardck50Nessuna valutazione finora

- HindeSight Investor Letter October 2010 The World Monetary EarthquakeDocumento27 pagineHindeSight Investor Letter October 2010 The World Monetary Earthquakerichardck50Nessuna valutazione finora

- Breakfast With Dave 100410Documento13 pagineBreakfast With Dave 100410richardck50Nessuna valutazione finora

- Emerging Market Uprising:: What It Means For InvestorsDocumento12 pagineEmerging Market Uprising:: What It Means For Investorsbi11yNessuna valutazione finora

- Lunch With Dave 101510Documento10 pagineLunch With Dave 101510richardck50Nessuna valutazione finora

- Andrew Lo PresentationDocumento23 pagineAndrew Lo Presentationrichardck50100% (1)

- Pushing On A String Pushing On A String Let's Shift The Focus An Invitation To An Inflation Party Ten Years and Counting by John MauldinDocumento10 paginePushing On A String Pushing On A String Let's Shift The Focus An Invitation To An Inflation Party Ten Years and Counting by John Mauldinrichardck50Nessuna valutazione finora

- NapierDocumento14 pagineNapierrichardck50Nessuna valutazione finora

- U.S. Government Debt: The Upward Spiral Continues: Olume EptemberDocumento23 pagineU.S. Government Debt: The Upward Spiral Continues: Olume Eptemberrichardck50Nessuna valutazione finora

- Breakfast With Dave 092010Documento9 pagineBreakfast With Dave 092010richardck50Nessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)