Potrebbero piacerti anche

- Accounting For Ijarah TransactionDocumento3 pagineAccounting For Ijarah Transactiontiffada86Nessuna valutazione finora

- Accounting For MusharakahDocumento10 pagineAccounting For MusharakahAthira HusnaNessuna valutazione finora

- Financial Accounting I SemesterDocumento25 pagineFinancial Accounting I SemesterBhaskar KrishnappaNessuna valutazione finora

- Ijarah 4 Month-CompleteDocumento62 pagineIjarah 4 Month-CompleteHasan Irfan SiddiquiNessuna valutazione finora

- AAOIFI - Introduction: 2-How AAOIFI Standards Support Islamic Finance IndustryDocumento3 pagineAAOIFI - Introduction: 2-How AAOIFI Standards Support Islamic Finance Industryshahidameen2Nessuna valutazione finora

- Ijarah and Mudharabah ExerciseDocumento3 pagineIjarah and Mudharabah ExerciseAhmadNajmi100% (1)

- Accounting For SalamDocumento19 pagineAccounting For SalamVani IndrawatiNessuna valutazione finora

- Unit 7AccountingforMurabaha&AmpDocumento27 pagineUnit 7AccountingforMurabaha&AmpSon Go Han0% (1)

- IBF 6250 Accounting For Islamic Financial Institutions Course Outline 2018Documento5 pagineIBF 6250 Accounting For Islamic Financial Institutions Course Outline 2018Muhammad SyamilNessuna valutazione finora

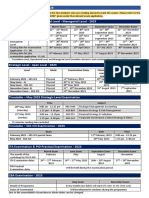

- CMA Sri Lanka Examination Calendar - 2023 - Updated - 07!03!2023Documento1 paginaCMA Sri Lanka Examination Calendar - 2023 - Updated - 07!03!2023chamila2345Nessuna valutazione finora

- Accounting For MurabahaDocumento10 pagineAccounting For MurabahanooramyNessuna valutazione finora

- Bba 4 Semester (Morning) SESSION 2014-2018 Submitted byDocumento11 pagineBba 4 Semester (Morning) SESSION 2014-2018 Submitted byAnonymous qBJv2A8RANessuna valutazione finora

- Lecture 10 (A) - Al IJARAHDocumento39 pagineLecture 10 (A) - Al IJARAHAngela MaymayNessuna valutazione finora

- Compare The Characteristic of Islamic Accounting Versus ConventionalDocumento13 pagineCompare The Characteristic of Islamic Accounting Versus ConventionalHafiz BajauNessuna valutazione finora

- Salam and IstisnaDocumento24 pagineSalam and IstisnaM Fani MalikNessuna valutazione finora

- Solutions Quiz 1 and Quiz 2Documento9 pagineSolutions Quiz 1 and Quiz 2BatrisyiaNessuna valutazione finora

- Ibf Case StudyDocumento17 pagineIbf Case StudyAyesha HamidNessuna valutazione finora

- Islamic Accounting AssignmentDocumento2 pagineIslamic Accounting AssignmentAhmad Saifuddin Che AbdullahNessuna valutazione finora

- Accounting For Musyarakah FinancingDocumento16 pagineAccounting For Musyarakah FinancingHadyan AntoroNessuna valutazione finora

- Fair Value Adjustment and Consolidation Adjustment Week 2Documento9 pagineFair Value Adjustment and Consolidation Adjustment Week 2Omolaja IbukunNessuna valutazione finora

- MR Khairul Nizam (AAOIFI - Governance and Auditing Standards) PDFDocumento46 pagineMR Khairul Nizam (AAOIFI - Governance and Auditing Standards) PDFisyrafhakim2314Nessuna valutazione finora

- Islamic BK CH 3 PDFDocumento27 pagineIslamic BK CH 3 PDFAA BB MMNessuna valutazione finora

- Topic 4Documento53 pagineTopic 4ShaikhaAlnoaimiNessuna valutazione finora

- Murabaha Part 1Documento40 pagineMurabaha Part 1sjawaidiqbal100% (3)

- Case Studies For Discussion PDF For IBFDocumento16 pagineCase Studies For Discussion PDF For IBFAmna Naseer100% (1)

- Chap 3 True FalseDocumento24 pagineChap 3 True FalseSaadat ShaikhNessuna valutazione finora

- 3 Underwriting of Shares PDFDocumento8 pagine3 Underwriting of Shares PDFSangam NeupaneNessuna valutazione finora

- Elements of Contracts, Form (Sighah) : Chapter # 2Documento10 pagineElements of Contracts, Form (Sighah) : Chapter # 2ادیبہ اشفاقNessuna valutazione finora

- Financial System of BangladeshDocumento2 pagineFinancial System of BangladeshFardin Ahmed MugdhoNessuna valutazione finora

- Islamic AccountingDocumento9 pagineIslamic AccountingMohamed QubatiNessuna valutazione finora

- Aaoifi PDFDocumento6 pagineAaoifi PDFInas BennaniNessuna valutazione finora

- Topic 1 - Accounting For Issue of Shares and DebenturesDocumento64 pagineTopic 1 - Accounting For Issue of Shares and DebenturesJustineNessuna valutazione finora

- CH 3 Accounting For Mudharabah Financing 1Documento32 pagineCH 3 Accounting For Mudharabah Financing 1Yusuf Hussein40% (5)

- Bai As-Salam and Istisna'Documento26 pagineBai As-Salam and Istisna'Angela MaymayNessuna valutazione finora

- How To Prepare Realisation Account: AssetsDocumento1 paginaHow To Prepare Realisation Account: Assetsmichael odiemboNessuna valutazione finora

- Bay' At-Tawarruq Vs Bay' Al-InahDocumento3 pagineBay' At-Tawarruq Vs Bay' Al-InahIZZAH ZAHINNessuna valutazione finora

- WaqfDocumento17 pagineWaqfDeepak SharmaNessuna valutazione finora

- Transaction CycleDocumento6 pagineTransaction CycleRachamalla KrishnareddyNessuna valutazione finora

- RIBA and It's TypesDocumento10 pagineRIBA and It's Typesfaisalconsultant100% (2)

- CHAPTER 1 (STRUCTuRE OF MALAYSIAN FINANCIAL SYSTEM)Documento13 pagineCHAPTER 1 (STRUCTuRE OF MALAYSIAN FINANCIAL SYSTEM)han guzelNessuna valutazione finora

- Essentials of Islamic Finance: Final Quiz Fall 2012 AnswersDocumento2 pagineEssentials of Islamic Finance: Final Quiz Fall 2012 Answersshan100% (1)

- Diminishing Musharaka IjarahBasedDocumento22 pagineDiminishing Musharaka IjarahBasedArsalan AqeeqNessuna valutazione finora

- Weightage Meaning & Factors, Calculation & Techniques For Distribution of Profit Under Mudaraba System112Documento4 pagineWeightage Meaning & Factors, Calculation & Techniques For Distribution of Profit Under Mudaraba System112MD. ANWAR UL HAQUENessuna valutazione finora

- Wakala DepositDocumento1 paginaWakala DepositSolomon TekalignNessuna valutazione finora

- MFRS 124 Related Party Disclosure (RPD)Documento3 pagineMFRS 124 Related Party Disclosure (RPD)NURUL FAEIZAH BINTI AHMAD ANWAR / UPMNessuna valutazione finora

- This Study Resource Was: Murabahah QuizDocumento4 pagineThis Study Resource Was: Murabahah QuizMuhammad AbdullahNessuna valutazione finora

- Company Law Test 7Documento3 pagineCompany Law Test 7Anjali KotadiaNessuna valutazione finora

- Cases Review Affin Bank BHD V Zulkifli Bin Abdullah (2006) 3 MLJ 67 High Court, Kuala Lumpur Abdul Wahab Patail J 1. FactsDocumento6 pagineCases Review Affin Bank BHD V Zulkifli Bin Abdullah (2006) 3 MLJ 67 High Court, Kuala Lumpur Abdul Wahab Patail J 1. FactsMuhammad DenialNessuna valutazione finora

- BFD NotesDocumento84 pagineBFD NotesFarukh NaveedNessuna valutazione finora

- AFS2033 Lecture 10 Salam AccountingDocumento22 pagineAFS2033 Lecture 10 Salam AccountingAna FienaNessuna valutazione finora

- On Bank AuditDocumento101 pagineOn Bank Auditrinky123123100% (4)

- Salmabad, Kingdom of Bahrain College of Administrative and Financial Sciences Project Work InstructionsDocumento8 pagineSalmabad, Kingdom of Bahrain College of Administrative and Financial Sciences Project Work InstructionshamzaNessuna valutazione finora

- PES Question-Accounting Exercise 2.1 SalamDocumento11 paginePES Question-Accounting Exercise 2.1 SalamSolomon Tekalign100% (2)

- Al Ijarah TashghiliyahDocumento5 pagineAl Ijarah TashghiliyahPolkapolka DotNessuna valutazione finora

- VouchingDocumento9 pagineVouchingaupaup100% (2)

- MusharakaDocumento29 pagineMusharakaNauman AminNessuna valutazione finora

- MGA3033 Course Outline OBE 1092013Documento9 pagineMGA3033 Course Outline OBE 1092013Nur FahanaNessuna valutazione finora

- FINA 615 Islamic Financial Contracts - IjarahDocumento22 pagineFINA 615 Islamic Financial Contracts - IjarahFBusinessNessuna valutazione finora

- Chapter 10.accounting For IjarahDocumento46 pagineChapter 10.accounting For Ijarahhasan jabrNessuna valutazione finora

- Chapter 5 Ijarah 16012022 061036pmDocumento12 pagineChapter 5 Ijarah 16012022 061036pmYusra Rehman KhanNessuna valutazione finora

- National Cardiovascular Centre Harapan Kita JULY, 15, 2019Documento30 pagineNational Cardiovascular Centre Harapan Kita JULY, 15, 2019Aya BeautycareNessuna valutazione finora

- 007 City of Baguio vs. NAWASADocumento13 pagine007 City of Baguio vs. NAWASARonald MorenoNessuna valutazione finora

- Bmsa Book With CoverDocumento251 pagineBmsa Book With CoverHurol Samuel100% (7)

- VSM TrainingDocumento90 pagineVSM Trainingjoaoalcada100% (1)

- Pearl ContinentalDocumento12 paginePearl Continentalcool_n_hunky2005100% (3)

- Attorneys 2007Documento12 pagineAttorneys 2007kawallaceNessuna valutazione finora

- Financial Market and Institutions Ch16Documento8 pagineFinancial Market and Institutions Ch16kellyNessuna valutazione finora

- 100 Project Manager Interview QuestionsDocumento4 pagine100 Project Manager Interview Questionsadon970% (1)

- JDEtips Article E1PagesCreationDocumento20 pagineJDEtips Article E1PagesCreationValdir AraujoNessuna valutazione finora

- Market Penetration of Maggie NoodelsDocumento10 pagineMarket Penetration of Maggie Noodelsapi-3765623100% (1)

- UPS Case StudyDocumento2 pagineUPS Case StudyCharysa Januarizka50% (2)

- Which Public Goods Should Be Public/privateDocumento12 pagineWhich Public Goods Should Be Public/privateRozyNessuna valutazione finora

- Monetary Policy of India - WikipediaDocumento4 pagineMonetary Policy of India - Wikipediaambikesh008Nessuna valutazione finora

- Ejb3.0 Simplified APIDocumento6 pagineEjb3.0 Simplified APIRushabh ParekhNessuna valutazione finora

- Amity School of Engineering & Technology: B. Tech. (MAE), V Semester Rdbms Sunil VyasDocumento13 pagineAmity School of Engineering & Technology: B. Tech. (MAE), V Semester Rdbms Sunil VyasJose AntonyNessuna valutazione finora

- Fyp ProjectDocumento5 pagineFyp ProjectUsman PashaNessuna valutazione finora

- The Basics: Statement of Assets, Liabilities, and Net Worth: What Is A Saln?Documento7 pagineThe Basics: Statement of Assets, Liabilities, and Net Worth: What Is A Saln?Ren Irene D MacatangayNessuna valutazione finora

- DOLE 2015 Annual Report Ulat Sa Mga Boss (Philippine Department of Labor and Employment)Documento212 pagineDOLE 2015 Annual Report Ulat Sa Mga Boss (Philippine Department of Labor and Employment)Nora O. GamoloNessuna valutazione finora

- Brief Overview of APPLDocumento2 pagineBrief Overview of APPLRashedul Islam BappyNessuna valutazione finora

- Data Mexico EdcDocumento12 pagineData Mexico EdcDaniel Eduardo Arriaga JiménezNessuna valutazione finora

- Application of Digital MarketingDocumento72 pagineApplication of Digital MarketingSurajit SarbabidyaNessuna valutazione finora

- Jay Abraham May 2006 Presentation SlidesDocumento169 pagineJay Abraham May 2006 Presentation SlidesLeon Van Tubbergh100% (4)

- CH 5 Answers To Homework AssignmentsDocumento13 pagineCH 5 Answers To Homework AssignmentsJan Spanton100% (1)

- LA Metro - 608Documento4 pagineLA Metro - 608cartographicaNessuna valutazione finora

- Canto Cumulus: What's New?: Product InformationDocumento12 pagineCanto Cumulus: What's New?: Product InformationTeppo TestaajaNessuna valutazione finora

- Management 10th Edition Daft Test BankDocumento34 pagineManagement 10th Edition Daft Test Bankpatrickpandoradb6i100% (26)

- Labor Bar Examination Questions 2018Documento34 pagineLabor Bar Examination Questions 2018xiadfreakyNessuna valutazione finora

- Strategic Management IbsDocumento497 pagineStrategic Management IbsGARGI CHAKRABORTYNessuna valutazione finora

- Webinar Manajemen Keuangan PerusahaanDocumento69 pagineWebinar Manajemen Keuangan PerusahaanDias CandrikaNessuna valutazione finora

- Sip ReportDocumento114 pagineSip Reportprincy chauhanNessuna valutazione finora