Potrebbero piacerti anche

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Deposit Refund Agreement (Template)Documento2 pagineDeposit Refund Agreement (Template)LR FNessuna valutazione finora

- Reorganizing Philippines Ministry of Transportation and CommunicationsDocumento13 pagineReorganizing Philippines Ministry of Transportation and CommunicationsLR FNessuna valutazione finora

- Executive Order No. 109Documento3 pagineExecutive Order No. 109Ian HatolNessuna valutazione finora

- Executive Order No. 125-ADocumento7 pagineExecutive Order No. 125-ALR FNessuna valutazione finora

- Eo 93Documento2 pagineEo 93LR FNessuna valutazione finora

- Affidavit Change Color Motor VehicleDocumento1 paginaAffidavit Change Color Motor VehicleLR FNessuna valutazione finora

- IRR of RA 9295 2014 Amendments - Domestic Shipping Development ActDocumento42 pagineIRR of RA 9295 2014 Amendments - Domestic Shipping Development ActIrene Balmes-LomibaoNessuna valutazione finora

- Opening Water Transport IndustryDocumento6 pagineOpening Water Transport IndustryLR FNessuna valutazione finora

- Quitclaim Affidavit ReleaseDocumento2 pagineQuitclaim Affidavit ReleaseLR FNessuna valutazione finora

- Affidavit of Loss of PassportDocumento1 paginaAffidavit of Loss of PassportPlan Can JoxNessuna valutazione finora

- 2014-2017 Bar TaxationDocumento41 pagine2014-2017 Bar TaxationLR F0% (1)

- Rules Implementing Code of Conduct for Public OfficialsDocumento18 pagineRules Implementing Code of Conduct for Public OfficialsicebaguilatNessuna valutazione finora

- Begun and Held Metro Manila, On Monday, The Twerity Third of July, T W o Thousand SevenDocumento33 pagineBegun and Held Metro Manila, On Monday, The Twerity Third of July, T W o Thousand SevenSusielyn Anne Tumamao AngobungNessuna valutazione finora

- PALE Current Judicial Ethics CasesDocumento52 paginePALE Current Judicial Ethics CasesLR F100% (1)

- Special Proceedingss Habeas Corpus BarDocumento3 pagineSpecial Proceedingss Habeas Corpus BarLR FNessuna valutazione finora

- Torts Civil Liability in Criminal CasesDocumento2 pagineTorts Civil Liability in Criminal CasesLR FNessuna valutazione finora

- Affidavit of Loss Not For SaleDocumento1 paginaAffidavit of Loss Not For SaleLR FNessuna valutazione finora

- San Beda College of LawDocumento36 pagineSan Beda College of LawVladimir ReyesNessuna valutazione finora

- Canons 17-19 CasesDocumento33 pagineCanons 17-19 CasesLR FNessuna valutazione finora

- LMC - Boundary Dispute CasesDocumento12 pagineLMC - Boundary Dispute CasesLR FNessuna valutazione finora

- Transportation Law Case DigestDocumento38 pagineTransportation Law Case DigestLR FNessuna valutazione finora

- Villanueva Vs DomingoDocumento8 pagineVillanueva Vs Domingozpuse_wtpNessuna valutazione finora

- Taxation Cases 2bDocumento130 pagineTaxation Cases 2bLR FNessuna valutazione finora

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocumento7 pagineBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledLR FNessuna valutazione finora

- Sales Civil Law Memory AidDocumento4 pagineSales Civil Law Memory AidLR FNessuna valutazione finora

- Ra 7160 IrrDocumento263 pagineRa 7160 IrrAlvaro Garingo100% (21)

- Sales Civil Law Memory AidDocumento4 pagineSales Civil Law Memory AidLR FNessuna valutazione finora

- Supreme Court decisions on effect and application of lawsDocumento65 pagineSupreme Court decisions on effect and application of lawsAmicus CuriaeNessuna valutazione finora

- Legal Medicine-Judicial-AffidavitDocumento10 pagineLegal Medicine-Judicial-AffidavitLR FNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- ERC vs. Commissioner Fe B. BarinDocumento2 pagineERC vs. Commissioner Fe B. BarinNN DDLNessuna valutazione finora

- 18-National Power Corp. v. Province of Quezon GR No 171586Documento11 pagine18-National Power Corp. v. Province of Quezon GR No 171586ryanmeinNessuna valutazione finora

- Maceda Vs MacaraigDocumento3 pagineMaceda Vs MacaraigAnonymous 5MiN6I78I0100% (2)

- 06.04 National Power Corporation vs. VeraDocumento8 pagine06.04 National Power Corporation vs. VeragabbyborNessuna valutazione finora

- NPC and Growth Link Dispute Over Alleged Defective Engine PartsDocumento179 pagineNPC and Growth Link Dispute Over Alleged Defective Engine PartsNoel SincoNessuna valutazione finora

- Philippine Sinter Corporation and Phividec Industrial Authority Vs Cagayan Electric Power and Light Co IncDocumento1 paginaPhilippine Sinter Corporation and Phividec Industrial Authority Vs Cagayan Electric Power and Light Co IncJa Ru100% (2)

- NPC v. City of Cabanatuan-DigestDocumento2 pagineNPC v. City of Cabanatuan-DigestMartel John Milo100% (1)

- Republic of The Philippines - Energy Regulatory CommissionDocumento13 pagineRepublic of The Philippines - Energy Regulatory CommissionKhenan James NarismaNessuna valutazione finora

- ERC Cases Filed in 2020 SummaryDocumento347 pagineERC Cases Filed in 2020 SummaryMarc ValenciaNessuna valutazione finora

- JD Case Digest in Introduction To Law FINAL TERMDocumento20 pagineJD Case Digest in Introduction To Law FINAL TERMevangeline san joseNessuna valutazione finora

- Eduardo F Hernandez Et Al Vs National Power CorporationDocumento12 pagineEduardo F Hernandez Et Al Vs National Power CorporationMariel D. PortilloNessuna valutazione finora

- NPC vs. QuezonDocumento11 pagineNPC vs. QuezonSjaneyNessuna valutazione finora

- Doe Circular No. Dc2009!05!0008Documento33 pagineDoe Circular No. Dc2009!05!0008Cathy FongNessuna valutazione finora

- Acronyms by The Philippine GovernmentDocumento7 pagineAcronyms by The Philippine GovernmentBAROTEA Cressia Mhay G.Nessuna valutazione finora

- Alalayan v. National Power Corporation, 1968Documento6 pagineAlalayan v. National Power Corporation, 1968Hannief Ampa21Nessuna valutazione finora

- Hydroelectric Power Plants in The Philippines: Boado, Airah Joy M. Gole Cruz, Naomi Aira D Lagasca, Venus Glenda SDocumento33 pagineHydroelectric Power Plants in The Philippines: Boado, Airah Joy M. Gole Cruz, Naomi Aira D Lagasca, Venus Glenda SNaomi Aira Gole CruzNessuna valutazione finora

- PSALM v. CIR GR 198146 August 8, 2017 Case DigestDocumento3 paginePSALM v. CIR GR 198146 August 8, 2017 Case Digestbeingme2Nessuna valutazione finora

- 300MW Coal Power Plant in Davao Inaugurated PDFDocumento5 pagine300MW Coal Power Plant in Davao Inaugurated PDFAlan P. MangalimanNessuna valutazione finora

- Philippine Sinter Corp v. Cagayan Electric Power and Light Co. Inc., G.R. No. 127371 (2002) )Documento2 paginePhilippine Sinter Corp v. Cagayan Electric Power and Light Co. Inc., G.R. No. 127371 (2002) )Keyan Motol0% (1)

- CTA Rules Semirara Mining Corporation Entitled to VAT RefundDocumento7 pagineCTA Rules Semirara Mining Corporation Entitled to VAT Refundnathalie velasquezNessuna valutazione finora

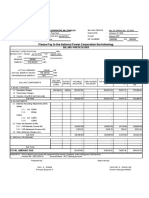

- Please Pay To The National Power Corporation The Following:: Billing ParticularsDocumento5 paginePlease Pay To The National Power Corporation The Following:: Billing ParticularsJaapar HassanNessuna valutazione finora

- Bangus Fry Fisherfolk v. Hon. Lanzanas, G.R. No. 131442, 10 July 2003Documento4 pagineBangus Fry Fisherfolk v. Hon. Lanzanas, G.R. No. 131442, 10 July 2003Angelette BulacanNessuna valutazione finora

- Case Digest - Art10, Public CorpDocumento7 pagineCase Digest - Art10, Public Corpcabby17Nessuna valutazione finora

- Maceda vs. MacaraigDocumento2 pagineMaceda vs. MacaraigJoseph DimalantaNessuna valutazione finora

- Trial court cannot interfere with decision of co-equal administrative bodyDocumento1 paginaTrial court cannot interfere with decision of co-equal administrative bodyShaira Mae CuevillasNessuna valutazione finora

- Case Digest: SURNECO v. ERC: ISSUE: Whether or Not The CA Erred in Affirming The ERC DecisionDocumento4 pagineCase Digest: SURNECO v. ERC: ISSUE: Whether or Not The CA Erred in Affirming The ERC DecisionEscanor GrandineNessuna valutazione finora

- 029 FREGILLANA Alalayan v. National Power CorporationDocumento1 pagina029 FREGILLANA Alalayan v. National Power CorporationCarissa CruzNessuna valutazione finora

- National Power Corporation Vs Provincial Government of BataanDocumento2 pagineNational Power Corporation Vs Provincial Government of BataanRachel LeachonNessuna valutazione finora

- Epira Law - Google SearchDocumento1 paginaEpira Law - Google SearchErnesto ButawanNessuna valutazione finora

- Bangus Fry Fisherfolk v. Lanzanas G.R. No. 131442Documento7 pagineBangus Fry Fisherfolk v. Lanzanas G.R. No. 131442Jojie FriasNessuna valutazione finora