Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- Hall of FameDocumento4 pagineHall of Famelittleredribbons83% (12)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Benefits AccountingDocumento4 pagineBenefits AccountingJulian Christopher Torcuator50% (2)

- Pre Qualification Form - Electrical ItemsDocumento16 paginePre Qualification Form - Electrical Itemssahuharish_gNessuna valutazione finora

- SegmentationDocumento5 pagineSegmentationChahatBhattiAli75% (4)

- Political Economics - NotesDocumento3 paginePolitical Economics - Notesdittman1430Nessuna valutazione finora

- International EconomicsDocumento1 paginaInternational Economicsdittman1430Nessuna valutazione finora

- Political Economics - NotesDocumento3 paginePolitical Economics - Notesdittman1430Nessuna valutazione finora

- Final Portfolio: English 150 Section 800Documento30 pagineFinal Portfolio: English 150 Section 800dittman1430Nessuna valutazione finora

- Writing Prompt FourDocumento2 pagineWriting Prompt Fourdittman1430Nessuna valutazione finora

- Wine Study AnalysisDocumento18 pagineWine Study Analysisdittman1430Nessuna valutazione finora

- Syllabus QuestionsDocumento3 pagineSyllabus Questionsdittman1430Nessuna valutazione finora

- BOB Airplanes Piano Sheet Music FreeDocumento2 pagineBOB Airplanes Piano Sheet Music Freedittman1430Nessuna valutazione finora

- Savant SyndromeDocumento7 pagineSavant Syndromedittman1430Nessuna valutazione finora

- Syllabus QuestionsDocumento3 pagineSyllabus Questionsdittman1430Nessuna valutazione finora

- Discussion Document CollegeDocumento5 pagineDiscussion Document Collegedittman1430Nessuna valutazione finora

- Ten Writing Principles by Greg DittmanDocumento2 pagineTen Writing Principles by Greg Dittmandittman1430Nessuna valutazione finora

- WP 3Documento2 pagineWP 3dittman1430Nessuna valutazione finora

- Discussion Document CollegeDocumento5 pagineDiscussion Document Collegedittman1430Nessuna valutazione finora

- Signing of The Declaration of IndependenceDocumento5 pagineSigning of The Declaration of Independencedittman1430Nessuna valutazione finora

- Latin AmericaDocumento13 pagineLatin Americadittman1430Nessuna valutazione finora

- Savant SyndromeDocumento7 pagineSavant Syndromedittman1430Nessuna valutazione finora

- Chapter 8 Part 1Documento86 pagineChapter 8 Part 1dittman1430Nessuna valutazione finora

- Savant SyndromeDocumento7 pagineSavant Syndromedittman1430Nessuna valutazione finora

- ACL Tears - Percentage by SportDocumento12 pagineACL Tears - Percentage by Sportdittman1430Nessuna valutazione finora

- Why I WriteDocumento3 pagineWhy I Writedittman1430Nessuna valutazione finora

- Memorandum: To: From: Date: ReDocumento1 paginaMemorandum: To: From: Date: Redittman1430Nessuna valutazione finora

- ACL Tears - Percentage by SportDocumento12 pagineACL Tears - Percentage by Sportdittman1430Nessuna valutazione finora

- Final Fantasy X 2 1000 Words-C-Major Sheet MusicDocumento3 pagineFinal Fantasy X 2 1000 Words-C-Major Sheet Musicdittman1430Nessuna valutazione finora

- Final Fantasy X 2 1000 Words-C-Major Sheet MusicDocumento3 pagineFinal Fantasy X 2 1000 Words-C-Major Sheet Musicdittman1430Nessuna valutazione finora

- Chapter 14 Practice Test AnswersDocumento3 pagineChapter 14 Practice Test Answersdittman1430Nessuna valutazione finora

- AP Psych Unit 4 VocabDocumento3 pagineAP Psych Unit 4 Vocabdittman1430Nessuna valutazione finora

- AP Psychology Unit 8BDocumento1 paginaAP Psychology Unit 8Bdittman1430Nessuna valutazione finora

- Managing Small Projects PDFDocumento4 pagineManaging Small Projects PDFJ. ZhouNessuna valutazione finora

- Pilipinas Shell Petroleum Corporation: SHLPHDocumento17 paginePilipinas Shell Petroleum Corporation: SHLPHIsis Normagne PascualNessuna valutazione finora

- DissolutionDocumento2 pagineDissolutionReniva KhingNessuna valutazione finora

- Sambhav 2023Documento8 pagineSambhav 2023prachi singhNessuna valutazione finora

- Solved Question Rhodes CorporationDocumento4 pagineSolved Question Rhodes CorporationBilalTariqNessuna valutazione finora

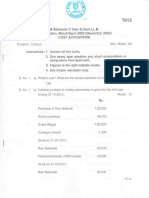

- 3rd Sem Cost Accounting Apr 2023Documento8 pagine3rd Sem Cost Accounting Apr 2023Chandan GNessuna valutazione finora

- Human Resource ManagementDocumento66 pagineHuman Resource ManagementMwanza MaliiNessuna valutazione finora

- Sobha Windsor Launch Pricelist R0 Feb 19, 2020 To S&MDocumento22 pagineSobha Windsor Launch Pricelist R0 Feb 19, 2020 To S&Mvineet dumirNessuna valutazione finora

- Strategic Capacity PlanningDocumento12 pagineStrategic Capacity PlanningFariah Ahsan RashaNessuna valutazione finora

- Death of Big LawDocumento55 pagineDeath of Big Lawmaxxwe11Nessuna valutazione finora

- Chapter 3: R.A. 9520 Cooperative Code of The Phillipines 2008Documento33 pagineChapter 3: R.A. 9520 Cooperative Code of The Phillipines 2008Alzcareen Erie LiwayanNessuna valutazione finora

- ch03 Sum PDFDocumento14 paginech03 Sum PDFOona NiallNessuna valutazione finora

- Quick Response LogisticsDocumento18 pagineQuick Response LogisticsPrasad Chandran100% (7)

- A Study On Customer Preference Towards Brand FactoryDocumento21 pagineA Study On Customer Preference Towards Brand FactoryH.Arokiaraj100% (2)

- Bank Mergers & Acquisitions in Central Eastern EuropeDocumento96 pagineBank Mergers & Acquisitions in Central Eastern Europefumata23415123451Nessuna valutazione finora

- Challenges and Pathways For Brazilian Mining Sustainability - 2021Documento12 pagineChallenges and Pathways For Brazilian Mining Sustainability - 2021MariaLuciaMendiolaMonsanteNessuna valutazione finora

- Unit OneDocumento19 pagineUnit OnePree ThiNessuna valutazione finora

- Monthly Digest Dec 2013Documento134 pagineMonthly Digest Dec 2013innvolNessuna valutazione finora

- SM ProjectDocumento31 pagineSM ProjectHrushikeish ShindeNessuna valutazione finora

- The Compact For Responsive and Responsible Leadership: A Roadmap For Sustainable Long-Term Growth and OpportunityDocumento1 paginaThe Compact For Responsive and Responsible Leadership: A Roadmap For Sustainable Long-Term Growth and OpportunityMiguel AugustoNessuna valutazione finora

- A Survey Paper - PM 1.0Documento5 pagineA Survey Paper - PM 1.0Aswin KrishnanNessuna valutazione finora

- Unit 1 Final PresentationDocumento111 pagineUnit 1 Final PresentationVandana SharmaNessuna valutazione finora

- Financial Planning and Budgets: Presented By: Rose Ann C. Paramio, Cpa, MbaDocumento44 pagineFinancial Planning and Budgets: Presented By: Rose Ann C. Paramio, Cpa, MbaAki StephyNessuna valutazione finora

- 2023 Budget Ordinance First ReadingDocumento3 pagine2023 Budget Ordinance First ReadinginforumdocsNessuna valutazione finora

- Bo SungDocumento10 pagineBo SungYên Khuê TrầnNessuna valutazione finora

- LifebuoyDocumento10 pagineLifebuoyJyoti JangidNessuna valutazione finora

- WRITING SUMMER 2021 - Pie Chart & Table - CT2.21Documento13 pagineWRITING SUMMER 2021 - Pie Chart & Table - CT2.21farm 3 chi diNessuna valutazione finora