Potrebbero piacerti anche

- Gift Card With Pin - Numbr - Google SearchDocumento1 paginaGift Card With Pin - Numbr - Google SearchOluwaseyifunmi RichardNessuna valutazione finora

- Fight Online Scams with CautionDocumento7 pagineFight Online Scams with CautionNamnam Dela CruzNessuna valutazione finora

- Ecommerce in Today'S MarketDocumento7 pagineEcommerce in Today'S MarketDileepHaraniNessuna valutazione finora

- Tutorial Apply For Benefits Online TWCDocumento28 pagineTutorial Apply For Benefits Online TWCThuy PhamNessuna valutazione finora

- Government of Andhra Pradesh C.T.Department: Form of Way Bill Form X or Form 600Documento3 pagineGovernment of Andhra Pradesh C.T.Department: Form of Way Bill Form X or Form 600Arjun B Menon100% (1)

- South Carolina Realtor Residential Lease Agreement PDFDocumento8 pagineSouth Carolina Realtor Residential Lease Agreement PDFAnonymous gcGQ9ixNessuna valutazione finora

- Hushpuppi and Assoc.Documento69 pagineHushpuppi and Assoc.Modestus Ogbuka100% (1)

- How to link your myGov to your tax and superDocumento12 pagineHow to link your myGov to your tax and superLeksonNessuna valutazione finora

- ScamDocumento59 pagineScamClara McGrenardNessuna valutazione finora

- Application Fornat 2011Documento4 pagineApplication Fornat 2011Krishna AnumalasettyNessuna valutazione finora

- CA, Drivers Licence Renewal Confirmation.Documento3 pagineCA, Drivers Licence Renewal Confirmation.LSOrGrimNessuna valutazione finora

- Buying A Real Estate Property or LandDocumento5 pagineBuying A Real Estate Property or LandMay YellowNessuna valutazione finora

- BankDocumento2 pagineBankNeko CortesNessuna valutazione finora

- e-Ticket Itinerary & ReceiptDocumento9 paginee-Ticket Itinerary & ReceiptZatete TeahNessuna valutazione finora

- Promote Cultural Collaboration GrantsDocumento38 paginePromote Cultural Collaboration Grantsmuhamad erfanNessuna valutazione finora

- Online BankingDocumento13 pagineOnline BankingHarmanSinghNessuna valutazione finora

- Grant Verification FormDocumento2 pagineGrant Verification FormRafaela LopesNessuna valutazione finora

- Advance Fee Fraud and BanksDocumento10 pagineAdvance Fee Fraud and Banksbudi626Nessuna valutazione finora

- Google Voice - AntDocumento307 pagineGoogle Voice - AntDig81767Nessuna valutazione finora

- Lottery Bill 1Documento33 pagineLottery Bill 1the kingfishNessuna valutazione finora

- Scam Fraud: Prepared by S.Vinoth Martin Final - ITDocumento21 pagineScam Fraud: Prepared by S.Vinoth Martin Final - ITmaakkaNessuna valutazione finora

- Synaway Construction & Projects Pty Ltd letter of good standing not generated due to outstanding balanceDocumento1 paginaSynaway Construction & Projects Pty Ltd letter of good standing not generated due to outstanding balanceThabisoNessuna valutazione finora

- Goods and Services Tax Refund Tutorial PDFDocumento27 pagineGoods and Services Tax Refund Tutorial PDFMOHANNessuna valutazione finora

- Nanny Contract For Services: (Parents Of) of ("The Employer") and of ("The Nanny")Documento7 pagineNanny Contract For Services: (Parents Of) of ("The Employer") and of ("The Nanny")Catherine MifsudNessuna valutazione finora

- Collateral Loan Info PDFDocumento8 pagineCollateral Loan Info PDFcasmith43Nessuna valutazione finora

- Car Wrap Scam Kelloggs AgreementDocumento1 paginaCar Wrap Scam Kelloggs AgreementAnonymous NbMQ9Ymq100% (1)

- How To Write A CheckDocumento1 paginaHow To Write A CheckKushal Agarwal100% (1)

- TQ Pitch: ExcellentDocumento8 pagineTQ Pitch: ExcellentMuhammad ArifNessuna valutazione finora

- MR Joe Peter Grant. Foreign Transfer Manager Google Promotion Award Team Tel: +44-703-596-8841Documento2 pagineMR Joe Peter Grant. Foreign Transfer Manager Google Promotion Award Team Tel: +44-703-596-8841Fouad OuazzaniNessuna valutazione finora

- CHATTING FORMAT - txt-1Documento1 paginaCHATTING FORMAT - txt-1Darren FarmerNessuna valutazione finora

- B.TECH. Ist Yr TIMETABLE ODD SEMESTER 2019, JIIT-128 (Effective From 28/08/2019)Documento2 pagineB.TECH. Ist Yr TIMETABLE ODD SEMESTER 2019, JIIT-128 (Effective From 28/08/2019)JayantNessuna valutazione finora

- Bank DetailsDocumento5 pagineBank DetailsManish SriNessuna valutazione finora

- Summary of Accounting EntriesDocumento7 pagineSummary of Accounting EntriesABINASHNessuna valutazione finora

- Applying For Unemployment BenefitsDocumento31 pagineApplying For Unemployment BenefitsChris StoneNessuna valutazione finora

- Business Plan FormatDocumento32 pagineBusiness Plan FormatShailja DixitNessuna valutazione finora

- Craigslist Killer ManuscriptDocumento18 pagineCraigslist Killer ManuscriptElsie de DiosNessuna valutazione finora

- How To Load Amore Prepaid Card - Google SearchDocumento1 paginaHow To Load Amore Prepaid Card - Google SearchDanny MontanaNessuna valutazione finora

- EI Fund Transfer Intnl TT Form V3.0Documento1 paginaEI Fund Transfer Intnl TT Form V3.0Tosin SimeonNessuna valutazione finora

- Tenancy Application Information: Please Enclose With Your ApplicationDocumento4 pagineTenancy Application Information: Please Enclose With Your ApplicationHasnainLakhaNessuna valutazione finora

- Facebook Subpoena / Search Warrant GuidelinesDocumento5 pagineFacebook Subpoena / Search Warrant Guidelinesjascot_okNessuna valutazione finora

- Scam - CZ - Analyzing 419 Threat and ScamsDocumento39 pagineScam - CZ - Analyzing 419 Threat and Scamsauwa lisaNessuna valutazione finora

- Mega Millions Scam FB Posting With Notes PDFDocumento4 pagineMega Millions Scam FB Posting With Notes PDFCorbin CarpenterNessuna valutazione finora

- Yahoo! MSN NotificationDocumento2 pagineYahoo! MSN NotificationTahmidur RahmanNessuna valutazione finora

- DHHS Information Asset Register Extract 11 Jan 2018Documento260 pagineDHHS Information Asset Register Extract 11 Jan 2018Wadi Ouallen100% (1)

- Naija Crypto Community and Updates Tutorials1Documento25 pagineNaija Crypto Community and Updates Tutorials1Ajayi Samuel OpeyemiNessuna valutazione finora

- Tting Phone NumbersDocumento2 pagineTting Phone NumbersThomas CNessuna valutazione finora

- Dpa Begginer Guide 1Documento9 pagineDpa Begginer Guide 1NEXUS RivasticoNessuna valutazione finora

- Developing A Next-of-Kin Involvement Guide in Cancer Care - Results From A Consensus ProcessDocumento11 pagineDeveloping A Next-of-Kin Involvement Guide in Cancer Care - Results From A Consensus Processshaznay delacruzNessuna valutazione finora

- Special Report: "10 Dodgy Internet Scams That You Must Avoid"Documento8 pagineSpecial Report: "10 Dodgy Internet Scams That You Must Avoid"Adi ProphecyNessuna valutazione finora

- Melvyn Hiller v. Securities and Exchange Commission, 429 F.2d 856, 2d Cir. (1970)Documento5 pagineMelvyn Hiller v. Securities and Exchange Commission, 429 F.2d 856, 2d Cir. (1970)Scribd Government DocsNessuna valutazione finora

- Billing DoCUMENTSDocumento27 pagineBilling DoCUMENTSRyan Jay CagumbayNessuna valutazione finora

- Payment MethodDocumento19 paginePayment MethodOliviaDuchess100% (1)

- Online Banking - FIN464Documento58 pagineOnline Banking - FIN464Pavel093Nessuna valutazione finora

- 7 Best Places To Meet Single Women (2023)Documento9 pagine7 Best Places To Meet Single Women (2023)RasheedAladdinNGuiomalaNessuna valutazione finora

- BitcoinDocumento6 pagineBitcoinSakib AhmedNessuna valutazione finora

- Bank CreditsDocumento11 pagineBank CreditsAlexander DeckerNessuna valutazione finora

- House Contract PDFDocumento8 pagineHouse Contract PDFShannonBradenNessuna valutazione finora

- Ebooks of Medicine 6of4Documento7 pagineEbooks of Medicine 6of4the1uploaderNessuna valutazione finora

- Millions of Fake Accounts That Drowning and Burying Wells FargoDocumento67 pagineMillions of Fake Accounts That Drowning and Burying Wells Fargothe1uploaderNessuna valutazione finora

- Securities Industry in IndonesiaDocumento139 pagineSecurities Industry in Indonesiathe1uploaderNessuna valutazione finora

- Ebooks of Medicine 6of6Documento10 pagineEbooks of Medicine 6of6the1uploaderNessuna valutazione finora

- International Banking and Financial Markets DevelopmentDocumento174 pagineInternational Banking and Financial Markets Developmentthe1uploaderNessuna valutazione finora

- Print Your Own Money, Your Crypto-Based MoneyDocumento196 paginePrint Your Own Money, Your Crypto-Based Moneythe1uploaderNessuna valutazione finora

- Ebooks of Medicine 6of3Documento7 pagineEbooks of Medicine 6of3the1uploaderNessuna valutazione finora

- Ebooks of Medicine 6of5Documento7 pagineEbooks of Medicine 6of5the1uploaderNessuna valutazione finora

- Ebooks of Medicine 6of1Documento7 pagineEbooks of Medicine 6of1the1uploaderNessuna valutazione finora

- Inflation Management in IndonesiaDocumento44 pagineInflation Management in Indonesiathe1uploaderNessuna valutazione finora

- SuisseWin BackpacksDocumento12 pagineSuisseWin Backpacksthe1uploaderNessuna valutazione finora

- IDX Monthly Statistics: May 2017Documento116 pagineIDX Monthly Statistics: May 2017the1uploaderNessuna valutazione finora

- Ebooks of Medicine 6of2Documento7 pagineEbooks of Medicine 6of2the1uploaderNessuna valutazione finora

- SEC Tesla Klage Gov - Uscourts.nysd.501881.1.0Documento9 pagineSEC Tesla Klage Gov - Uscourts.nysd.501881.1.0the1uploaderNessuna valutazione finora

- Asset Bubble: The Causalities and Its LimiterDocumento46 pagineAsset Bubble: The Causalities and Its Limiterthe1uploaderNessuna valutazione finora

- Millions of Fake Accounts That Drowning and Burying Wells FargoDocumento67 pagineMillions of Fake Accounts That Drowning and Burying Wells Fargothe1uploaderNessuna valutazione finora

- Windows Explorer Has Stopped WorkingDocumento53 pagineWindows Explorer Has Stopped Workingthe1uploaderNessuna valutazione finora

- Transfer Pricing in IndonesiaDocumento149 pagineTransfer Pricing in Indonesiathe1uploader0% (1)

- KMS, Artificial Intelligence, & The Economist 20150509Documento47 pagineKMS, Artificial Intelligence, & The Economist 20150509the1uploaderNessuna valutazione finora

- Daftar Akreditasi Program Studi & Direktori Perguruan Tinggi Di Indonesia, Sept. 2015Documento101 pagineDaftar Akreditasi Program Studi & Direktori Perguruan Tinggi Di Indonesia, Sept. 2015the1uploader100% (2)

- Behind The Libor Scandal, 20120710Documento1 paginaBehind The Libor Scandal, 20120710the1uploaderNessuna valutazione finora

- Energy Industry in Indonesia & World's Renewable EnergyDocumento12 pagineEnergy Industry in Indonesia & World's Renewable Energythe1uploaderNessuna valutazione finora

- Microeconomics and Policy AnalysisDocumento6 pagineMicroeconomics and Policy Analysisthe1uploaderNessuna valutazione finora

- Advanced MicroeconomicsDocumento13 pagineAdvanced Microeconomicsthe1uploaderNessuna valutazione finora

- Money Creation in The Modern Economy Bank EnglandDocumento14 pagineMoney Creation in The Modern Economy Bank Englandbreakingthesilence100% (1)

- EU Implementation of Basel IIIDocumento59 pagineEU Implementation of Basel IIIthe1uploaderNessuna valutazione finora

- Basel I, Basel II, and Emerging Markets A Nontechnical Analysis 052008Documento18 pagineBasel I, Basel II, and Emerging Markets A Nontechnical Analysis 052008Santosh KadamNessuna valutazione finora

- Oracle V Google API OrderDocumento41 pagineOracle V Google API OrderflohmannNessuna valutazione finora

- Merchant Web Services API Customer Information Manager (CIM) SOAP GuideDocumento91 pagineMerchant Web Services API Customer Information Manager (CIM) SOAP Guidethe1uploaderNessuna valutazione finora

- Defining and Establishing Insolvency in AustraliaDocumento8 pagineDefining and Establishing Insolvency in AustraliaMNessuna valutazione finora

- The Risk-Return Tradeoff Is The Principle That Potential Return Rises With An Increase in RiskDocumento5 pagineThe Risk-Return Tradeoff Is The Principle That Potential Return Rises With An Increase in Riskjoshua0% (1)

- 2020 Vision11Documento98 pagine2020 Vision11derektennant100% (2)

- Reporter No. 4 - Pdic LawDocumento47 pagineReporter No. 4 - Pdic LawJi YuNessuna valutazione finora

- Scps FinanceDocumento19 pagineScps FinanceIsaac BernsteinNessuna valutazione finora

- Financial Check Up FormsDocumento10 pagineFinancial Check Up FormsJoshelle B. BanciloNessuna valutazione finora

- Test Sample 3 Law On SalesDocumento10 pagineTest Sample 3 Law On SalesDarlene SarcinoNessuna valutazione finora

- All SD PacDocumento5 pagineAll SD PacPat PowersNessuna valutazione finora

- Central Visayas Finance Corp v Spouses Adlawan ruling on deficiency judgmentDocumento1 paginaCentral Visayas Finance Corp v Spouses Adlawan ruling on deficiency judgmentKristel Alyssa MarananNessuna valutazione finora

- Account Statement From 29 Jul 2020 To 31 Jul 2020Documento1 paginaAccount Statement From 29 Jul 2020 To 31 Jul 2020Ashwin PrajapatiNessuna valutazione finora

- Πιστωτική Κάρτα -ΕργασίαDocumento97 pagineΠιστωτική Κάρτα -ΕργασίαVivian KarkNessuna valutazione finora

- TaxDocumento11 pagineTaxFreak'n HellNessuna valutazione finora

- Credit DigestsDocumento22 pagineCredit Digestsjojazz74Nessuna valutazione finora

- ING Bank Annual Report 2015: A step aheadDocumento286 pagineING Bank Annual Report 2015: A step aheadJasper Laarmans Teixeira de MattosNessuna valutazione finora

- Ra 9267Documento8 pagineRa 9267Cedric VanguardiaNessuna valutazione finora

- CGTMSE - Claim Lodgment Part-IIDocumento10 pagineCGTMSE - Claim Lodgment Part-IISunil KumarNessuna valutazione finora

- Industrial FinanceDocumento11 pagineIndustrial Financedesaijpr90% (10)

- Pinnacle Part 2Documento1 paginaPinnacle Part 2Eneng Shofa ShopurohNessuna valutazione finora

- Research - Criminal - Elements of EstafaDocumento10 pagineResearch - Criminal - Elements of EstafaJunnieson BonielNessuna valutazione finora

- Capital Code Consultant Private Limited decoded business valueDocumento2 pagineCapital Code Consultant Private Limited decoded business valueKiran MaliNessuna valutazione finora

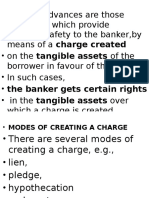

- Mode of Creation ChargeDocumento43 pagineMode of Creation ChargeSaurab JainNessuna valutazione finora

- Time Value of Money: All Rights ReservedDocumento43 pagineTime Value of Money: All Rights ReservedAnonymous f7wV1lQKRNessuna valutazione finora

- Sample-Loan Commitment LetterDocumento3 pagineSample-Loan Commitment LetterJustice Williams100% (1)

- Doug Riddle AFV-A4V PatchedDocumento41 pagineDoug Riddle AFV-A4V PatchedGalina Novahova96% (80)

- Trusts Act, 1882Documento37 pagineTrusts Act, 1882SufiaNessuna valutazione finora

- LEVEL 2 Online Quiz - Answers SET ADocumento10 pagineLEVEL 2 Online Quiz - Answers SET AVincent Larrie MoldezNessuna valutazione finora

- Jaiib - 2 Afb - Quick Book Nov 2017Documento136 pagineJaiib - 2 Afb - Quick Book Nov 2017Chinnadurai Lakshmanan75% (4)

- Gross-Estate-Lecture-January-7-2020 2Documento12 pagineGross-Estate-Lecture-January-7-2020 2jonahNessuna valutazione finora

- My Secured Promissory NoteDocumento4 pagineMy Secured Promissory NotegebannNessuna valutazione finora

- Intl Exchange Bank V Sps BrionesDocumento1 paginaIntl Exchange Bank V Sps BrionesmoniquehadjirulNessuna valutazione finora