Potrebbero piacerti anche

- Asian Mergers and Acquisitions: Riding the WaveDa EverandAsian Mergers and Acquisitions: Riding the WaveValutazione: 4.5 su 5 stelle4.5/5 (2)

- The Embedded Corporation: Corporate Governance and Employment Relations in Japan and the United StatesDa EverandThe Embedded Corporation: Corporate Governance and Employment Relations in Japan and the United StatesNessuna valutazione finora

- Investment Offices Flourish in AsiaDocumento24 pagineInvestment Offices Flourish in Asiagypsie0Nessuna valutazione finora

- The Impact of Shareholder Activism - Cover Story - The Edge MalaysiaDocumento3 pagineThe Impact of Shareholder Activism - Cover Story - The Edge Malaysiaqpmoerzh100% (1)

- Market IntermediariesDocumento70 pagineMarket IntermediariesmallelaindiraNessuna valutazione finora

- Position Paper v1Documento8 paginePosition Paper v1Rohan GuptaNessuna valutazione finora

- (Sony) Presentation Slides 30marchDocumento20 pagine(Sony) Presentation Slides 30marchMelissa LawNessuna valutazione finora

- Oct 2003 ADocumento10 pagineOct 2003 ADines KumarNessuna valutazione finora

- Shareholder Activism in IndiaDocumento11 pagineShareholder Activism in IndiaImpact JournalsNessuna valutazione finora

- McKinsey Emerging Stronger Fitter Faster The Rise of The Asian Corporation v2Documento9 pagineMcKinsey Emerging Stronger Fitter Faster The Rise of The Asian Corporation v2Quynh NguyenNessuna valutazione finora

- Leadership in A Rapidly Changing World: How Businesses in India Are Reframing SuccessDocumento28 pagineLeadership in A Rapidly Changing World: How Businesses in India Are Reframing SuccessjvbakshiNessuna valutazione finora

- Kaushik Basu 2009 China and India Economic and Political WeeklyDocumento13 pagineKaushik Basu 2009 China and India Economic and Political WeeklyAman Mohapatra50% (2)

- Japan Is Changing Its Views On Entrepreneurship, and That Could Be Good For Start-UpsDocumento3 pagineJapan Is Changing Its Views On Entrepreneurship, and That Could Be Good For Start-UpsPhongg ĐụtNessuna valutazione finora

- The Informal Economyin UlaanbaatarDocumento42 pagineThe Informal Economyin UlaanbaatarBaigalmaa NyamtserenNessuna valutazione finora

- FYSE China Social Enterprise Report 2012Documento40 pagineFYSE China Social Enterprise Report 2012Alexandre QuintãoNessuna valutazione finora

- Cover Story - Private Equity Changing Capital Market LandscapeDocumento3 pagineCover Story - Private Equity Changing Capital Market LandscapeWei Cong TanNessuna valutazione finora

- The Fourth Wheel 2017Documento75 pagineThe Fourth Wheel 2017Handcrafting BeautiesNessuna valutazione finora

- (Sony) Position Paper FINALDocumento18 pagine(Sony) Position Paper FINALMelissa LawNessuna valutazione finora

- Factors Affecting Stratups Innovation and GrowthDocumento9 pagineFactors Affecting Stratups Innovation and GrowthKalkidan Admasu AyalewNessuna valutazione finora

- Legal Framework For Startups in PakistanDocumento11 pagineLegal Framework For Startups in PakistanNida Rehman KhanNessuna valutazione finora

- PhilippinesDocumento12 paginePhilippinesPablo MatosasNessuna valutazione finora

- The Rise of The Chinese Unicorn An Exploratory Study of Unicorn Companies in ChinaDocumento16 pagineThe Rise of The Chinese Unicorn An Exploratory Study of Unicorn Companies in ChinaDulanji PiumiNessuna valutazione finora

- China's Competitiveness Case Study LenovoDocumento44 pagineChina's Competitiveness Case Study LenovomanchorusNessuna valutazione finora

- 6889-Article Text-20050-1-10-20160129Documento15 pagine6889-Article Text-20050-1-10-20160129Badass BadassNessuna valutazione finora

- Emerging Market Strategy: Organization - General Electric Country - EthopiaDocumento34 pagineEmerging Market Strategy: Organization - General Electric Country - EthopiaHardeep SinghNessuna valutazione finora

- India2011 Brochure 18Documento6 pagineIndia2011 Brochure 18Deepali JetleyNessuna valutazione finora

- Project Report ON "Investment Banking On HSBC"Documento54 pagineProject Report ON "Investment Banking On HSBC"Ajit JainNessuna valutazione finora

- Initial Findings: What Difference Do Cooperatives Make?: Philippines Country StudyDocumento10 pagineInitial Findings: What Difference Do Cooperatives Make?: Philippines Country StudyMary JustineNessuna valutazione finora

- In - Fin - Nitie: Financial InclusionDocumento31 pagineIn - Fin - Nitie: Financial InclusionMeera MohanNessuna valutazione finora

- MNC721 Assignment PMMDocumento14 pagineMNC721 Assignment PMMphonemyint myatNessuna valutazione finora

- IB Directory 2010Documento73 pagineIB Directory 2010Ruchik Doshi0% (1)

- RPR 2009 1Documento350 pagineRPR 2009 1AVINASH KUMAR SINGHNessuna valutazione finora

- CG Japan PDFDocumento43 pagineCG Japan PDFAtabur RahmanNessuna valutazione finora

- Funding To Growing StartupDocumento11 pagineFunding To Growing StartupHerta SteinfeldNessuna valutazione finora

- Growth and Development Notes 20Documento5 pagineGrowth and Development Notes 20pancakes101bimboNessuna valutazione finora

- The Indian Startup Ecosystem: Drivers, Challenges and Pillars of SupportDocumento55 pagineThe Indian Startup Ecosystem: Drivers, Challenges and Pillars of SupportVijay KumarNessuna valutazione finora

- You Can Do This Ange Trust HimDocumento74 pagineYou Can Do This Ange Trust Himjuzzcam.14Nessuna valutazione finora

- Ly 2020Documento18 pagineLy 2020Rakibul HasanNessuna valutazione finora

- Nomura Research TeamDocumento20 pagineNomura Research TeamYeli LiuNessuna valutazione finora

- AsianInvestor - Asia's 25 Most Influential People in Private EquityDocumento8 pagineAsianInvestor - Asia's 25 Most Influential People in Private EquityMayank AggarwalNessuna valutazione finora

- All About Investments: Foreign Direct Investments in The PhilippinesDocumento2 pagineAll About Investments: Foreign Direct Investments in The PhilippinesDaphney DeeNessuna valutazione finora

- Activist Investing in Europe 2017Documento12 pagineActivist Investing in Europe 2017Megha GuptaNessuna valutazione finora

- Research and Analysis On Herd Behavior of Individual InvestorsDocumento5 pagineResearch and Analysis On Herd Behavior of Individual InvestorsThuy LaNessuna valutazione finora

- Artikel 5 (Luh Sukarini)Documento4 pagineArtikel 5 (Luh Sukarini)Luhh SukarhyniNessuna valutazione finora

- Organizational Factors Affecting Operational Efficiency in The Tourism Business in ThailandDocumento4 pagineOrganizational Factors Affecting Operational Efficiency in The Tourism Business in ThailandInternational Journal of Innovative Science and Research TechnologyNessuna valutazione finora

- Kauffman Index 2017: Growth Entrepreneurship Metropolitan Area and City TrendsDocumento28 pagineKauffman Index 2017: Growth Entrepreneurship Metropolitan Area and City TrendsThe Ewing Marion Kauffman Foundation100% (1)

- Fukuhmss19acc0183 Oche Acc 3210Documento15 pagineFukuhmss19acc0183 Oche Acc 3210Sunday OcheNessuna valutazione finora

- Iifl Jack - 1-2Documento42 pagineIifl Jack - 1-2Juber FarediwalaNessuna valutazione finora

- 36 - 00 - Business TodayDocumento5 pagine36 - 00 - Business TodayvivoposNessuna valutazione finora

- 1313077291GEM 2003 Global ReportDocumento118 pagine1313077291GEM 2003 Global Reportgian ososNessuna valutazione finora

- Institutional Quality, Financial Development and Investment in Nigeria: An Asymmetric Cointegrating ApproachDocumento9 pagineInstitutional Quality, Financial Development and Investment in Nigeria: An Asymmetric Cointegrating ApproachInternational Journal of Innovative Science and Research TechnologyNessuna valutazione finora

- GCP Initial Japan Startup Ecosystem Report 1700229780Documento21 pagineGCP Initial Japan Startup Ecosystem Report 1700229780satori.effectNessuna valutazione finora

- Corporate Governance Complete ProjectDocumento21 pagineCorporate Governance Complete ProjectEswar Stark100% (1)

- PavimentosDocumento15 paginePavimentosByronNessuna valutazione finora

- Harneet Kaur Project Work 2018-19 - Manjot Kaur BoparaiDocumento40 pagineHarneet Kaur Project Work 2018-19 - Manjot Kaur BoparaiPrateek kumar SahuNessuna valutazione finora

- MC2023071203E 完成稿8381Documento31 pagineMC2023071203E 完成稿8381Eris LNessuna valutazione finora

- Assignment On FTPDocumento45 pagineAssignment On FTPSimranjeet Singh BediNessuna valutazione finora

- Impact Investors in Asia: Characteristics and Preferences for Investing in Social Enterprises in Asia and the PacificDa EverandImpact Investors in Asia: Characteristics and Preferences for Investing in Social Enterprises in Asia and the PacificValutazione: 5 su 5 stelle5/5 (1)

- Playing the Long Game: How to Save the West from Short-TermismDa EverandPlaying the Long Game: How to Save the West from Short-TermismValutazione: 1 su 5 stelle1/5 (1)

- Angel Investing: Insider Secrets to Wealth CreationDa EverandAngel Investing: Insider Secrets to Wealth CreationValutazione: 5 su 5 stelle5/5 (1)

- The Edge Quarz Capital Hedge Fund Manager Writes Open Letter To ESR 14 Nov 2019Documento1 paginaThe Edge Quarz Capital Hedge Fund Manager Writes Open Letter To ESR 14 Nov 2019qpmoerzhNessuna valutazione finora

- The Edge Sabana REIT's Untapped GFA Could Raise NAV As New Tech Park Undergoes AEI 18 Nov 2019Documento2 pagineThe Edge Sabana REIT's Untapped GFA Could Raise NAV As New Tech Park Undergoes AEI 18 Nov 2019qpmoerzhNessuna valutazione finora

- CEREC 01.01.2021 Presentation PDFDocumento34 pagineCEREC 01.01.2021 Presentation PDFqpmoerzhNessuna valutazione finora

- CEREC 2.4 E++.pagesDocumento277 pagineCEREC 2.4 E++.pagesqpmoerzhNessuna valutazione finora

- CEREC 01.01.2021 Presentation PDFDocumento34 pagineCEREC 01.01.2021 Presentation PDFqpmoerzhNessuna valutazione finora

- Quarz Capital Management Open Letter Sabana REIT and ESR Cayman Nov 2019 FINALDocumento6 pagineQuarz Capital Management Open Letter Sabana REIT and ESR Cayman Nov 2019 FINALqpmoerzh100% (1)

- Business Times Ascendas Hospitality Trust Should Merge With Ascott REIT, Says Quarz Capital 25 April 2019Documento2 pagineBusiness Times Ascendas Hospitality Trust Should Merge With Ascott REIT, Says Quarz Capital 25 April 2019qpmoerzhNessuna valutazione finora

- Quarz - Capital Sunningdale TechDocumento23 pagineQuarz - Capital Sunningdale TechqpmoerzhNessuna valutazione finora

- The Edge Quarz Urges Sunningdale To Raise Dividend Distribution To 60% of Core Net Profit 13 Dec 2018Documento2 pagineThe Edge Quarz Urges Sunningdale To Raise Dividend Distribution To 60% of Core Net Profit 13 Dec 2018qpmoerzhNessuna valutazione finora

- Bloomberg Activist Fund Urges Singapore REIT Merger To Boost Value 25 April 2019Documento2 pagineBloomberg Activist Fund Urges Singapore REIT Merger To Boost Value 25 April 2019qpmoerzhNessuna valutazione finora

- Bloomberg Activist Hedge Fund Quarz Sees 40% Upside in Sunningdale 13 Dec 2018Documento1 paginaBloomberg Activist Hedge Fund Quarz Sees 40% Upside in Sunningdale 13 Dec 2018qpmoerzhNessuna valutazione finora

- Quarz Capital Management Open Letter Sunningdale Tech Dec 2018 FINALDocumento4 pagineQuarz Capital Management Open Letter Sunningdale Tech Dec 2018 FINALqpmoerzhNessuna valutazione finora

- Straits Times HG Metal To Undertake Capital Reduction Return Cash To Shareholders 25 Sept 2017Documento1 paginaStraits Times HG Metal To Undertake Capital Reduction Return Cash To Shareholders 25 Sept 2017qpmoerzhNessuna valutazione finora

- QCM HG Metal Manufacturing Limited Presentation 31 May 2017Documento21 pagineQCM HG Metal Manufacturing Limited Presentation 31 May 2017qpmoerzhNessuna valutazione finora

- Lending Club Shares Surge On Brighter EarningsDocumento2 pagineLending Club Shares Surge On Brighter EarningsqpmoerzhNessuna valutazione finora

- Quarz Capital Management CSE Global Presentation FINAL 26th Feb 2018Documento23 pagineQuarz Capital Management CSE Global Presentation FINAL 26th Feb 2018qpmoerzhNessuna valutazione finora

- Activist Insight Dissident Win Proxy Contest at International Healthway 23 Jan 2017Documento1 paginaActivist Insight Dissident Win Proxy Contest at International Healthway 23 Jan 2017qpmoerzhNessuna valutazione finora

- Quarz Capital ASIA Financial Analyst InternDocumento1 paginaQuarz Capital ASIA Financial Analyst InternqpmoerzhNessuna valutazione finora

- QCA Open Letter To LendingClub Board and Management 9 May 2018 FINALDocumento5 pagineQCA Open Letter To LendingClub Board and Management 9 May 2018 FINALqpmoerzhNessuna valutazione finora

- Quarz Capital Management Open Letter To CSE Global FINAL 26th Feb 2018Documento6 pagineQuarz Capital Management Open Letter To CSE Global FINAL 26th Feb 2018qpmoerzhNessuna valutazione finora

- Bloomberg IHC Shareholders Vote To Replace Board As OUE Buys 208m Shares 24 Jan 2017Documento1 paginaBloomberg IHC Shareholders Vote To Replace Board As OUE Buys 208m Shares 24 Jan 2017qpmoerzhNessuna valutazione finora

- Straits Times Activist Investor Targets International Healthway Jan 14 2017Documento2 pagineStraits Times Activist Investor Targets International Healthway Jan 14 2017qpmoerzhNessuna valutazione finora

- Quarz Capital Management International Healthway Corp FINAL Presentation 17 Jan 2017Documento18 pagineQuarz Capital Management International Healthway Corp FINAL Presentation 17 Jan 2017qpmoerzhNessuna valutazione finora

- PR Newswire QCM Open Letter To The Board of Directors of HG Metal 31 May 2017Documento5 paginePR Newswire QCM Open Letter To The Board of Directors of HG Metal 31 May 2017qpmoerzhNessuna valutazione finora

- Barrons This Singaporean Stock Could Be More Than 60% Undervalued 1 June 2017Documento3 pagineBarrons This Singaporean Stock Could Be More Than 60% Undervalued 1 June 2017qpmoerzhNessuna valutazione finora

- Quarz Capital Management PR NEWSWIRE Final Open Letter To International Healthway Corp 13 Jan 2017Documento5 pagineQuarz Capital Management PR NEWSWIRE Final Open Letter To International Healthway Corp 13 Jan 2017qpmoerzhNessuna valutazione finora

- The Gould Standard Capital Crusaders On The March 10 Dec 2015Documento3 pagineThe Gould Standard Capital Crusaders On The March 10 Dec 2015qpmoerzhNessuna valutazione finora

- Must DoDocumento27 pagineMust DoKuldeep SharmaNessuna valutazione finora

- Professional - May 2022Documento186 pagineProfessional - May 2022Jason Baba KwagheNessuna valutazione finora

- Explain (Simply and in Your Own Words) What The Company DoesDocumento8 pagineExplain (Simply and in Your Own Words) What The Company DoesShreyas LakshminarayanNessuna valutazione finora

- Course Outline UGBS 205 2023Documento6 pagineCourse Outline UGBS 205 2023Chocho berly100% (1)

- Lesson 13Documento37 pagineLesson 13fabriNessuna valutazione finora

- Error CorrectionDocumento17 pagineError CorrectionCelina PamintuanNessuna valutazione finora

- Hedge Fund Interview Pitch September 1Documento14 pagineHedge Fund Interview Pitch September 1dorowsjNessuna valutazione finora

- Chua Company Sample Problem (Periodic) DocxDocumento2 pagineChua Company Sample Problem (Periodic) DocxCoolvetica100% (1)

- Final Project On: Punjab National Bank ScamDocumento22 pagineFinal Project On: Punjab National Bank ScamacharyamalvikaNessuna valutazione finora

- Company Law 1 IntroductionDocumento30 pagineCompany Law 1 IntroductionTumwesigyeNessuna valutazione finora

- AE 121 - C28 To C30 - Depreciation and DepletionDocumento66 pagineAE 121 - C28 To C30 - Depreciation and DepletionKendall JennerNessuna valutazione finora

- 06 BSCM v3.2 MasterDocumento54 pagine06 BSCM v3.2 MasterMostafaNessuna valutazione finora

- 601766e1ea0e740022470410-1612146674-COMPED 422 - EXAM 1Documento2 pagine601766e1ea0e740022470410-1612146674-COMPED 422 - EXAM 1Pritz Marc Bautista Morata100% (1)

- Rhode Vs Dock-Hop Co (1920)Documento1 paginaRhode Vs Dock-Hop Co (1920)EM RGNessuna valutazione finora

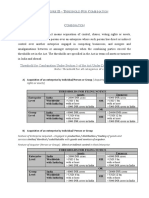

- Annexure II - CombinationDocumento2 pagineAnnexure II - CombinationAVNISH PRAKASHNessuna valutazione finora

- Accounting For Non-Current Assets Held For Sale (RMG 111) - Department of FinanceDocumento4 pagineAccounting For Non-Current Assets Held For Sale (RMG 111) - Department of FinanceDante JulianNessuna valutazione finora

- Accounting 102 Depreciation, Depletion, Revaluation, Impairment Summary QuizDocumento8 pagineAccounting 102 Depreciation, Depletion, Revaluation, Impairment Summary Quizjhean dabatosNessuna valutazione finora

- Cambridge IGCSE: Accounting 0452/12Documento12 pagineCambridge IGCSE: Accounting 0452/12afyNessuna valutazione finora

- Wa0002.Documento3 pagineWa0002.fatimah dinNessuna valutazione finora

- Slides Session 4Documento37 pagineSlides Session 4matthiaskoerner19Nessuna valutazione finora

- Khadija Khan Comapny Law Ist Internal AssessmentDocumento5 pagineKhadija Khan Comapny Law Ist Internal Assessmentkhadija khanNessuna valutazione finora

- PRTC 1st Preboard Solution GuideDocumento48 paginePRTC 1st Preboard Solution GuideAnonymous Lih1laax100% (2)

- Special Income Tax Treatment of Gains and Losses From Dealings in PropertyDocumento52 pagineSpecial Income Tax Treatment of Gains and Losses From Dealings in PropertyAngeliqueGiselleCNessuna valutazione finora

- 2003 CLD 463Documento24 pagine2003 CLD 463Irfan RiazNessuna valutazione finora

- CHEER UP Chapter 13 Gross Profit MethodDocumento7 pagineCHEER UP Chapter 13 Gross Profit MethodaprilNessuna valutazione finora

- SIP Report Bajaj Finserv Updated - NiharikaDocumento44 pagineSIP Report Bajaj Finserv Updated - NiharikaAniket AgrahariNessuna valutazione finora

- Contract Account FormatDocumento3 pagineContract Account FormatVishakh Nag100% (1)

- BSA 1101 - Fundamentals of Accounting 1 & 2Documento13 pagineBSA 1101 - Fundamentals of Accounting 1 & 2Chris MartinezNessuna valutazione finora

- Audit Procedures For Accounts PayableDocumento3 pagineAudit Procedures For Accounts PayableSweet Emme100% (1)

- Advanced Accounting Case Study PDFDocumento7 pagineAdvanced Accounting Case Study PDFAnonymous IpBC61Z100% (1)