Potrebbero piacerti anche

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Electoral System in IndiaDocumento13 pagineElectoral System in IndiaRaghu CkNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- HTMLDocumento8 pagineHTMLRaghu CkNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- Hra Rule 2aDocumento3 pagineHra Rule 2aRaghu CkNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- 07 Chapter 2Documento21 pagine07 Chapter 2Raghu CkNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Competency Mapping TelcoDocumento64 pagineCompetency Mapping TelcoRaghu CkNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Composition Scheme Under GSTDocumento8 pagineComposition Scheme Under GSTRaghu CkNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Basic Concepts of Income Tax ActDocumento14 pagineBasic Concepts of Income Tax ActRaghu CkNessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Bonded Labour in IndiaDocumento16 pagineBonded Labour in IndiaRaghu CkNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Income Tax Changes FY 2017-18Documento22 pagineIncome Tax Changes FY 2017-18soumyaviyer@gmail.comNessuna valutazione finora

- Composition Scheme Short NotesDocumento1 paginaComposition Scheme Short NotesRaghu CkNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- 1Documento11 pagine1thecoltNessuna valutazione finora

- Being As A Team Leader Why You Are Not Looking For Same Kind of Position Instead Why Are You Looking For Associate Level of JobDocumento2 pagineBeing As A Team Leader Why You Are Not Looking For Same Kind of Position Instead Why Are You Looking For Associate Level of JobRaghu CkNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Sa 200 AuditingDocumento32 pagineSa 200 AuditingRaghu CkNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Benami Transactions Prohibition Amendment Act 2015Documento33 pagineBenami Transactions Prohibition Amendment Act 2015Latest Laws TeamNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- ACS 1803 Accounting General Ledger SystemDocumento5 pagineACS 1803 Accounting General Ledger SystemRaghu Ck100% (1)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Business EthicsDocumento9 pagineBusiness Ethicskartikeya1067% (3)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- International Financial FlowsDocumento12 pagineInternational Financial FlowsAkhil James XaiozNessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

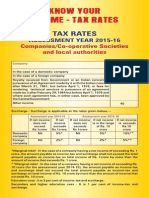

- Companies Tax RatesDocumento2 pagineCompanies Tax RatesRaghu CkNessuna valutazione finora

- Important Acts Related To BankingDocumento1 paginaImportant Acts Related To BankingRaghu CkNessuna valutazione finora

- Competency Mapping TelcoDocumento64 pagineCompetency Mapping TelcoRaghu CkNessuna valutazione finora

- Basic Concept of AccountingDocumento24 pagineBasic Concept of AccountingRaghu CkNessuna valutazione finora

- VAT, Luxury Tax, Entry Tax and Excise Duty Changes in Karnataka Budget 2014-15Documento4 pagineVAT, Luxury Tax, Entry Tax and Excise Duty Changes in Karnataka Budget 2014-15Raghu CkNessuna valutazione finora

- International Harmonization of Financial ReportingDocumento8 pagineInternational Harmonization of Financial ReportingRaghu Ck100% (1)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- SBI Computer QuizDocumento2 pagineSBI Computer QuizRaghu CkNessuna valutazione finora

- Corporate GovernanceDocumento8 pagineCorporate GovernanceRaghu CkNessuna valutazione finora

- Business EthicsDocumento9 pagineBusiness Ethicskartikeya1067% (3)

- A Study On Training & DevelopmentDocumento76 pagineA Study On Training & DevelopmentPradeepnspNessuna valutazione finora

- Categories of E-CommerceDocumento5 pagineCategories of E-CommerceRaghu CkNessuna valutazione finora

- Online Shopping ProjectDocumento11 pagineOnline Shopping ProjectRaghu CkNessuna valutazione finora

- Supply Chain Re-Engineering Saves Elizabeth Arden $180MDocumento6 pagineSupply Chain Re-Engineering Saves Elizabeth Arden $180MjaveriaNessuna valutazione finora

- 1 IB Nature & ScopeDocumento19 pagine1 IB Nature & ScopePanav MohindraNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Shipping Bill of LadingDocumento1 paginaShipping Bill of LadingdonsterthemonsterNessuna valutazione finora

- Spreadsheet Concepts Using Microsoft Excel: ObjectivesDocumento26 pagineSpreadsheet Concepts Using Microsoft Excel: ObjectivesYunita Yozpin AyanknyaRizalNessuna valutazione finora

- Redox, Group 2 and Group 7 ExtraDocumento8 pagineRedox, Group 2 and Group 7 ExtraShabnam ShahNessuna valutazione finora

- Suggested Readings:: Fragasso, P. M., & Israelsen, C. L. (2010) - Your Nest Egg Game Plan: How To Get YourDocumento3 pagineSuggested Readings:: Fragasso, P. M., & Israelsen, C. L. (2010) - Your Nest Egg Game Plan: How To Get YourLisa BlairNessuna valutazione finora

- MC ElroyDocumento2 pagineMC ElroyTanmay DastidarNessuna valutazione finora

- Bayfield Mud CompanyDocumento3 pagineBayfield Mud CompanyMica VillaNessuna valutazione finora

- Tanker CharteringDocumento78 pagineTanker CharteringVinod Dsouza100% (4)

- Expansion StrategyDocumento14 pagineExpansion StrategyAttin TalwarNessuna valutazione finora

- IntegralBusi Kingsford MarketingPlanDocumento29 pagineIntegralBusi Kingsford MarketingPlanTaimoor Ul HassanNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Real Estate Mortgage-JebulanDocumento2 pagineReal Estate Mortgage-JebulanLee-ai CarilloNessuna valutazione finora

- Cost Behavior: Analysis and UseDocumento36 pagineCost Behavior: Analysis and Userachim04100% (1)

- PerfumeDocumento21 paginePerfumedeoremeghanNessuna valutazione finora

- Intermediate Accounting Exam 2 SolutionsDocumento5 pagineIntermediate Accounting Exam 2 SolutionsAlex SchuldinerNessuna valutazione finora

- Lion Air ETicket (IIZKUK) - NataliaDocumento2 pagineLion Air ETicket (IIZKUK) - NataliaNatalia LeeNessuna valutazione finora

- Grade 11 Economics Unit #3: Government Intervention Practice Test and Answer KeyDocumento8 pagineGrade 11 Economics Unit #3: Government Intervention Practice Test and Answer KeyWayne TeoNessuna valutazione finora

- China Soap Synthetic Detergent Market ReportDocumento10 pagineChina Soap Synthetic Detergent Market ReportAllChinaReports.comNessuna valutazione finora

- HR Audit CaseDocumento9 pagineHR Audit CaseAnkit JainNessuna valutazione finora

- Swanand Co-Op. Housing Society LTDDocumento2 pagineSwanand Co-Op. Housing Society LTDskumarsrNessuna valutazione finora

- Bicol Region As One of The Hot Spot For Cacao IndustryDocumento10 pagineBicol Region As One of The Hot Spot For Cacao IndustryPlantacion de Sikwate0% (1)

- Keep Your Liquids On The Proper Flight Path: The New Security RegulationsDocumento2 pagineKeep Your Liquids On The Proper Flight Path: The New Security RegulationsChai YawatNessuna valutazione finora

- Analytical Chemistry Hand-Out 1Documento11 pagineAnalytical Chemistry Hand-Out 1Mark Jesson Datario100% (1)

- Product Portfolio AnalysisDocumento30 pagineProduct Portfolio AnalysisShakti Dash25% (4)

- Macro CH 11Documento48 pagineMacro CH 11maria37066100% (3)

- Indian News Agencies at A GlanceDocumento3 pagineIndian News Agencies at A GlanceNetijyata MahendruNessuna valutazione finora

- Caribou Stew RecipeDocumento4 pagineCaribou Stew RecipeNunatsiaqNewsNessuna valutazione finora

- Burger and Fries Ingredients Burgers: Fries: KetchupDocumento5 pagineBurger and Fries Ingredients Burgers: Fries: KetchupNobody2222Nessuna valutazione finora

- Ms Anuradha Bhatia Dit TP 1 MumbaiDocumento28 pagineMs Anuradha Bhatia Dit TP 1 MumbaiamolkhareNessuna valutazione finora

- IncotermsDocumento1 paginaIncotermssrinivas0% (1)