Potrebbero piacerti anche

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Reviewer in Income Taxation Old TaxationDocumento1 paginaReviewer in Income Taxation Old TaxationJanRalphBulanonNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Influential Business Leaders in The PhilippinesDocumento5 pagineInfluential Business Leaders in The PhilippinesJanRalphBulanonNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- HumanitiesDocumento3 pagineHumanitiesJanRalphBulanonNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Human Behavior in OrganizationDocumento8 pagineHuman Behavior in OrganizationJanRalphBulanonNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Preliminary InvestigationDocumento17 paginePreliminary InvestigationJanRalphBulanonNessuna valutazione finora

- Jan RalphPresentationDocumento9 pagineJan RalphPresentationJanRalphBulanonNessuna valutazione finora

- Jan Ralph P. BulanonDocumento1 paginaJan Ralph P. BulanonJanRalphBulanonNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- M.I. - Based Activities: Criteria 4 3 2 1Documento1 paginaM.I. - Based Activities: Criteria 4 3 2 1JanRalphBulanonNessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Demo (Grapes of Wrath)Documento7 pagineDemo (Grapes of Wrath)JanRalphBulanonNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Perception: Your Truth and The TruthDocumento23 paginePerception: Your Truth and The TruthJanRalphBulanonNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Epitome of Good LifeDocumento2 pagineEpitome of Good LifeJanRalphBulanonNessuna valutazione finora

- Periodic and PerpetualDocumento2 paginePeriodic and PerpetualLayNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Problem SetDocumento61 pagineProblem SetEmily FungNessuna valutazione finora

- Solutions Solution Manual09Documento109 pagineSolutions Solution Manual09RiaNessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Sip Dissertation - Final - Final For CollegeDocumento17 pagineSip Dissertation - Final - Final For Collegevikashirulkar922Nessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

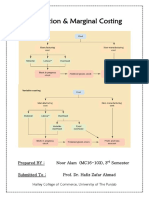

- Absorption & Marginal Costing - Noor Alam (MC16-103)Documento24 pagineAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- Brand Growth:: The Rules For SuccessDocumento4 pagineBrand Growth:: The Rules For SuccessRashmi Gopalakrishnan100% (1)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Customer Perception of Curry Powder Brands With Special Reference To Mohanlal's Taste Buds BrandDocumento7 pagineCustomer Perception of Curry Powder Brands With Special Reference To Mohanlal's Taste Buds BrandNimisha vkNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- MID TERM Internet - Marketing CHAPTER 6Documento185 pagineMID TERM Internet - Marketing CHAPTER 6BHAGYASHREE SHELARNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- BCG InsideSherpa Task HandsetLeasing - Email - AbinashAgrawalDocumento2 pagineBCG InsideSherpa Task HandsetLeasing - Email - AbinashAgrawalAbinash AgrawalNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Adolph Coors in The Brewing Industry: Take-AwaysDocumento9 pagineAdolph Coors in The Brewing Industry: Take-AwaysZANessuna valutazione finora

- EOQDocumento4 pagineEOQRavi SinghNessuna valutazione finora

- Value Under The Central Excise ActDocumento6 pagineValue Under The Central Excise ActChandu Aradhya S RNessuna valutazione finora

- Supply and Demand TogetherDocumento6 pagineSupply and Demand TogetherQuang ĐạiNessuna valutazione finora

- Uniqlo: SWOT AnalysisDocumento3 pagineUniqlo: SWOT AnalysisOpa Evilsiam0% (1)

- Forecasting Revenues and Cost To Be IncurredDocumento7 pagineForecasting Revenues and Cost To Be IncurredCharley Vill Credo100% (1)

- 1g Bingham CH 7 Prof Chauvins Instructions Student VersionDocumento13 pagine1g Bingham CH 7 Prof Chauvins Instructions Student VersionSalman KhalidNessuna valutazione finora

- Pom Unit 2Documento68 paginePom Unit 2sasikanthNessuna valutazione finora

- 3rd Sem Tourism MarketingDocumento2 pagine3rd Sem Tourism MarketingakashbpradeepcorpusNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- ENT PS Unit3 Lesson3 FinalDocumento28 pagineENT PS Unit3 Lesson3 FinalVince Romyson VenturaNessuna valutazione finora

- 2020 Inspection Grant Thornton LLP: (Headquartered in Chicago, Illinois)Documento24 pagine2020 Inspection Grant Thornton LLP: (Headquartered in Chicago, Illinois)Jason BramwellNessuna valutazione finora

- Investment Analysis and Stock Market OperationsDocumento45 pagineInvestment Analysis and Stock Market Operationssurabhi24jain4439100% (1)

- Buenafe, Melanie Joy P. Sbac-3D: Journal EntryDocumento7 pagineBuenafe, Melanie Joy P. Sbac-3D: Journal EntryMelanie BuenafeNessuna valutazione finora

- Strategic Social Media MarketingDocumento21 pagineStrategic Social Media MarketingTahir SaeedNessuna valutazione finora

- Marketing Plan PresentationDocumento20 pagineMarketing Plan Presentationakshaysingh211100% (1)

- Product Strategies: Branding & Packaging DecisionsDocumento17 pagineProduct Strategies: Branding & Packaging Decisionsyeschowdhary6722Nessuna valutazione finora

- HANA Presented SlidesDocumento102 pagineHANA Presented SlidesRao VedulaNessuna valutazione finora

- SSM Tvs Selling ProcessDocumento4 pagineSSM Tvs Selling ProcessAntara MukherjeeNessuna valutazione finora

- Financial Management - Assignment 2Documento7 pagineFinancial Management - Assignment 2Ngeno KipkiruiNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The PA I-78I-81 Logistics CorridorDocumento20 pagineThe PA I-78I-81 Logistics CorridorAnonymous Feglbx5Nessuna valutazione finora

- Brand AuditDocumento29 pagineBrand AuditRaman KulkarniNessuna valutazione finora