Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Commercial Real Estate International Business TrendsDocumento21 pagineCommercial Real Estate International Business TrendsNational Association of REALTORS®100% (2)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Why Baptists Are Not ProtestantsDocumento4 pagineWhy Baptists Are Not ProtestantsRyan Bladimer Africa RubioNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- How Can Cost Segregation Help Minimize Your Tax BurdenDocumento6 pagineHow Can Cost Segregation Help Minimize Your Tax BurdenO'Connor AssociateNessuna valutazione finora

- Scheulin Email Thread BRENT ROSEDocumento3 pagineScheulin Email Thread BRENT ROSEtpepperman100% (1)

- Giannasca FAR As Filed 10-10-2019 AcceptedDocumento39 pagineGiannasca FAR As Filed 10-10-2019 AcceptedRussinatorNessuna valutazione finora

- Healing Verses in QuranDocumento2 pagineHealing Verses in QuranBadrul Ahsan100% (1)

- IPRA Case DigestDocumento14 pagineIPRA Case DigestElden ClaireNessuna valutazione finora

- Jaka Investment Vs CIR - CDDocumento2 pagineJaka Investment Vs CIR - CDNolas Jay100% (1)

- Salonga Vs Cruz PanoDocumento1 paginaSalonga Vs Cruz PanoGeorge Demegillo Rocero100% (3)

- Durkheim's Division of Labor in SocietyDocumento22 pagineDurkheim's Division of Labor in SocietyJeorge M. Dela CruzNessuna valutazione finora

- Bids MinutesDocumento2 pagineBids MinutesJeanette Canales RapadaNessuna valutazione finora

- Why O'Connor For Property Tax Reduction?Documento7 pagineWhy O'Connor For Property Tax Reduction?O'Connor AssociateNessuna valutazione finora

- House Flipping - A New Way of IncomeDocumento6 pagineHouse Flipping - A New Way of IncomeO'Connor AssociateNessuna valutazione finora

- Steps To Protest in Harris CountyDocumento7 pagineSteps To Protest in Harris CountyO'Connor AssociateNessuna valutazione finora

- PRESENTATION - ERE - Tactics For Investors To Drive ROIDocumento7 paginePRESENTATION - ERE - Tactics For Investors To Drive ROIO'Connor AssociateNessuna valutazione finora

- How To Apply For A Homestead ExemptionDocumento6 pagineHow To Apply For A Homestead ExemptionO'Connor AssociateNessuna valutazione finora

- The IRS Guidelines For Non-Load Bearing WallsDocumento5 pagineThe IRS Guidelines For Non-Load Bearing WallsO'Connor AssociateNessuna valutazione finora

- Top 3 Methods of Valuing Personal PropertyDocumento7 pagineTop 3 Methods of Valuing Personal PropertyO'Connor AssociateNessuna valutazione finora

- Tax Benefits For Home OwnersDocumento7 pagineTax Benefits For Home OwnersO'Connor AssociateNessuna valutazione finora

- Wisconsin Municipal AssessorsDocumento48 pagineWisconsin Municipal AssessorsO'Connor AssociateNessuna valutazione finora

- PRESENTATION - OCA - The Thinning Line of Rental Collection in April - 2020Documento6 paginePRESENTATION - OCA - The Thinning Line of Rental Collection in April - 2020O'Connor AssociateNessuna valutazione finora

- 25+ Reasons You SHOULD Protest Your HIGH PROPERTY TAXESDocumento8 pagine25+ Reasons You SHOULD Protest Your HIGH PROPERTY TAXESO'Connor AssociateNessuna valutazione finora

- 3 Ways To Reduce Your Commercial Property Taxes With Cost SegregationDocumento7 pagine3 Ways To Reduce Your Commercial Property Taxes With Cost SegregationO'Connor AssociateNessuna valutazione finora

- Hcad Business Personal Property FaqDocumento2 pagineHcad Business Personal Property FaqO'Connor AssociateNessuna valutazione finora

- GeorgiaCertificationProgram2017 2018Documento2 pagineGeorgiaCertificationProgram2017 2018O'Connor AssociateNessuna valutazione finora

- Hcad Business Personal Property FaqDocumento2 pagineHcad Business Personal Property FaqO'Connor AssociateNessuna valutazione finora

- Property Assessment Appeal To The County Board of EqualizationDocumento4 pagineProperty Assessment Appeal To The County Board of EqualizationO'Connor AssociateNessuna valutazione finora

- Tax DeferralDocumento1 paginaTax DeferralO'Connor AssociateNessuna valutazione finora

- Dallascad - Propertytaxoverview2017Documento30 pagineDallascad - Propertytaxoverview2017O'Connor AssociateNessuna valutazione finora

- Cap Rate Rate ReportDocumento207 pagineCap Rate Rate ReportO'Connor Associate0% (1)

- Texas Real Estate InspectorDocumento25 pagineTexas Real Estate InspectorO'Connor AssociateNessuna valutazione finora

- Lincoln Institute of Land Policy's Comparison of 2016 Property TaxesDocumento108 pagineLincoln Institute of Land Policy's Comparison of 2016 Property TaxescrainsnewyorkNessuna valutazione finora

- Austin Property Taxpayer Remedies 2017Documento1 paginaAustin Property Taxpayer Remedies 2017O'Connor AssociateNessuna valutazione finora

- Dallas Central Appraisal District 2017 2018Documento30 pagineDallas Central Appraisal District 2017 2018O'Connor AssociateNessuna valutazione finora

- W C A D: Ise Ounty Ppraisal IstrictDocumento43 pagineW C A D: Ise Ounty Ppraisal IstrictO'Connor AssociateNessuna valutazione finora

- Williamson Cad 2017 Rendition General InformationDocumento2 pagineWilliamson Cad 2017 Rendition General InformationO'Connor AssociateNessuna valutazione finora

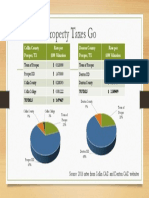

- Where The Property Taxes GoDocumento1 paginaWhere The Property Taxes GoO'Connor AssociateNessuna valutazione finora

- Montgomery County Exemption AnalysisDocumento19 pagineMontgomery County Exemption AnalysisO'Connor AssociateNessuna valutazione finora

- 101domain API Reseller Agreement - EncryptedDocumento19 pagine101domain API Reseller Agreement - EncryptedBenNessuna valutazione finora

- Crisis After Suffering One of Its Sharpest RecessionsDocumento5 pagineCrisis After Suffering One of Its Sharpest RecessionsПавло Коханський0% (2)

- London International Model United Nations: A Guide To MUN ResearchDocumento6 pagineLondon International Model United Nations: A Guide To MUN ResearchAldhani PutryNessuna valutazione finora

- Vector Potential For A Particle On The Ring and Unitary Transform of The HamiltonianDocumento8 pagineVector Potential For A Particle On The Ring and Unitary Transform of The HamiltonianShaharica BaluNessuna valutazione finora

- 48 2 PDFDocumento353 pagine48 2 PDFGrowlerJoeNessuna valutazione finora

- Case Study On Tata NanoDocumento12 pagineCase Study On Tata NanoChandel Manuj100% (1)

- RAILROAD Joint Petition For Rulemaking To Modernize Annual Revenue Adequacy DeterminationsDocumento182 pagineRAILROAD Joint Petition For Rulemaking To Modernize Annual Revenue Adequacy DeterminationsStar News Digital MediaNessuna valutazione finora

- Review - Phippine Arch Post WarDocumento34 pagineReview - Phippine Arch Post WariloilocityNessuna valutazione finora

- The Transfer of Property Act 1882Documento7 pagineThe Transfer of Property Act 1882harshad nickNessuna valutazione finora

- Presenters GuidelinesDocumento9 paginePresenters GuidelinesAl Dustur JurnalNessuna valutazione finora

- Appointments and ResignationsDocumento8 pagineAppointments and ResignationsKarthikNessuna valutazione finora

- Trip ID: 230329124846: New Delhi To Gorakhpur 11:15 GOPDocumento2 pagineTrip ID: 230329124846: New Delhi To Gorakhpur 11:15 GOPRishu KumarNessuna valutazione finora

- A. Abstract: "Same-Sex Adoption Rights"Documento12 pagineA. Abstract: "Same-Sex Adoption Rights"api-310703244Nessuna valutazione finora

- The First World WarDocumento3 pagineThe First World Warabhishek biswasNessuna valutazione finora

- Memo Re Intensification of Anti-Kidnapping Stratergy and Effort Against Motorcycle Riding Suspects (MRS)Documento2 pagineMemo Re Intensification of Anti-Kidnapping Stratergy and Effort Against Motorcycle Riding Suspects (MRS)Wilben DanezNessuna valutazione finora

- Hydrolics-Ch 4Documento21 pagineHydrolics-Ch 4solxNessuna valutazione finora

- 09 10 CalendarDocumento1 pagina09 10 CalendardhdyerNessuna valutazione finora

- Hugo Grotius and England - Hugh Trevor-RoperDocumento43 pagineHugo Grotius and England - Hugh Trevor-RopermoltenpaperNessuna valutazione finora

- Fam Law II - CompleteDocumento103 pagineFam Law II - CompletesoumyaNessuna valutazione finora

- My Quiz For Negotiable InstrumentsDocumento2 pagineMy Quiz For Negotiable InstrumentsJamie DiazNessuna valutazione finora

- Psalm 51 (Part 1)Documento5 paginePsalm 51 (Part 1)Virgil GillNessuna valutazione finora