Potrebbero piacerti anche

- Sun Pharma Report.Documento26 pagineSun Pharma Report.knowledge_power67% (15)

- SWOT Analysis of Allied Bank Limited, PakistanDocumento2 pagineSWOT Analysis of Allied Bank Limited, PakistanValeed Ak82% (11)

- Affidavit of Lara Ann Lavi - Dec 10 2009 - USA and Oppression - 2Documento32 pagineAffidavit of Lara Ann Lavi - Dec 10 2009 - USA and Oppression - 2asghar_786Nessuna valutazione finora

- Carwash Proposal: Introducing Broker: Contact Name: Email Address: Phone Number: Mobile Number: Fax NumberDocumento4 pagineCarwash Proposal: Introducing Broker: Contact Name: Email Address: Phone Number: Mobile Number: Fax Numbermuhammad waseemNessuna valutazione finora

- Carwash Proposal: Introducing Broker: Contact Name: Email Address: Phone Number: Mobile Number: Fax NumberDocumento4 pagineCarwash Proposal: Introducing Broker: Contact Name: Email Address: Phone Number: Mobile Number: Fax Numbermuhammad waseemNessuna valutazione finora

- Capital Budgeting Techniques: Multiple Choice QuestionsDocumento10 pagineCapital Budgeting Techniques: Multiple Choice QuestionsRod100% (1)

- Internship Report On Deposit and Investment Management of Al-Arafah Islami Bank LimitedDocumento92 pagineInternship Report On Deposit and Investment Management of Al-Arafah Islami Bank LimitedSiyamHossain80% (5)

- Personal Trading BehaviourDocumento5 paginePersonal Trading Behaviourapi-3739065Nessuna valutazione finora

- PDD Accounting For Bad Debts and Writeoffs (BDAR2160)Documento37 paginePDD Accounting For Bad Debts and Writeoffs (BDAR2160)SRDNessuna valutazione finora

- Internship Report On Meezan Bank LimitedDocumento24 pagineInternship Report On Meezan Bank LimitedZIA UL REHMANNessuna valutazione finora

- Mudasir Intership Report 27-10-2019Documento33 pagineMudasir Intership Report 27-10-2019Masroor Ali LarikNessuna valutazione finora

- Internship Report On The Bank of Punjab With Complete Analysis 2009Documento66 pagineInternship Report On The Bank of Punjab With Complete Analysis 2009Mohsin Saeed Bukhari77% (22)

- Sample IB Economics Internal Assessment Commentary - MacroDocumento3 pagineSample IB Economics Internal Assessment Commentary - MacroUday SethiNessuna valutazione finora

- Askari Bank LTDDocumento12 pagineAskari Bank LTDMuhammadAmmarKhalidNessuna valutazione finora

- ZTBLDocumento52 pagineZTBLSheikh Aqeel50% (2)

- Marvin Manufacturing Company: Cost of Goods Sold P 884,000Documento8 pagineMarvin Manufacturing Company: Cost of Goods Sold P 884,000Ryze100% (1)

- IKEADocumento22 pagineIKEAKurt MarshallNessuna valutazione finora

- Salas Vs CADocumento4 pagineSalas Vs CAHiroshi Carlos100% (1)

- Internship Report On Bank AlfalahDocumento81 pagineInternship Report On Bank AlfalahKomal ShujaatNessuna valutazione finora

- ZTBL Internship Report PDFDocumento71 pagineZTBL Internship Report PDFmuhammad waseem100% (8)

- Internship Report ZTBLDocumento106 pagineInternship Report ZTBLkamilbismaNessuna valutazione finora

- Internship Report National Bank of Pakistan and Its Nearest GuidelinesDocumento67 pagineInternship Report National Bank of Pakistan and Its Nearest GuidelinesAbaid SandhuNessuna valutazione finora

- Strategic Management Report On Bank of Punjab LTDDocumento17 pagineStrategic Management Report On Bank of Punjab LTDimranrajput100% (2)

- Internship Report On ZTBL by Mumtaz Ali HulioDocumento48 pagineInternship Report On ZTBL by Mumtaz Ali Hulioasif_iqbal84Nessuna valutazione finora

- Internship Report On Zarai Taraqiati Bank LTD (ZTBL)Documento48 pagineInternship Report On Zarai Taraqiati Bank LTD (ZTBL)bbaahmad8986% (7)

- ZTBL Research ReportDocumento66 pagineZTBL Research Reportsarfrazhunzai12383% (6)

- Internship Report On ZTBL by Aneeka NiazDocumento54 pagineInternship Report On ZTBL by Aneeka NiazAneeka Niaz33% (3)

- HRM Project On ZTBLDocumento42 pagineHRM Project On ZTBLAgha Ehtisham0% (1)

- Mba 5th ZTBL Internship ReportDocumento24 pagineMba 5th ZTBL Internship ReportZIA UL REHMANNessuna valutazione finora

- ZTBL ReportDocumento30 pagineZTBL ReportAbid Bilal100% (1)

- Internship Report On ZTBL by Mumtaz Ali HulioDocumento48 pagineInternship Report On ZTBL by Mumtaz Ali Huliohulimumtaz93% (14)

- Internship Report On ZTBL, Prepared by Wasim Uddin Orakzai Student of Finance 2010, KUSTDocumento95 pagineInternship Report On ZTBL, Prepared by Wasim Uddin Orakzai Student of Finance 2010, KUSTWasimOrakzai100% (4)

- Report On ZTBLDocumento23 pagineReport On ZTBLFarrukh Gurmani100% (1)

- Internship Report ZTBL, Hailey CollegeDocumento109 pagineInternship Report ZTBL, Hailey CollegeAdnan80% (10)

- ZTBL 14.8.16Documento68 pagineZTBL 14.8.16MansoorBalochNessuna valutazione finora

- Internship Report On ZTBLDocumento87 pagineInternship Report On ZTBLShabnam Naz100% (3)

- Soneri Bank Internship ReportDocumento71 pagineSoneri Bank Internship Reportrumzu100% (1)

- The Crescent Standard Investment Bank LimitedDocumento4 pagineThe Crescent Standard Investment Bank Limited11108218100% (1)

- Bank Alfalah Internship Report 2018Documento28 pagineBank Alfalah Internship Report 2018Hamza Butt100% (3)

- Soneri Bank Internship ReportDocumento37 pagineSoneri Bank Internship Reportbbaahmad89100% (1)

- Internship Report Askari Bank Ltd. 2009Documento59 pagineInternship Report Askari Bank Ltd. 2009Imran Mehmood100% (1)

- Sehrish Khan UBL ProjectDocumento62 pagineSehrish Khan UBL Projectsherybalouch100% (1)

- A Complete Report On HBL ManagementDocumento21 pagineA Complete Report On HBL ManagementSidra IdreesNessuna valutazione finora

- M2 .... Revised ZTBL ReportDocumento46 pagineM2 .... Revised ZTBL ReportqweNessuna valutazione finora

- Askari Bank Internship ReportDocumento101 pagineAskari Bank Internship ReportsolacuanNessuna valutazione finora

- Horizontal/Vertical Analysis 2013 Askari BankDocumento8 pagineHorizontal/Vertical Analysis 2013 Askari BankVania Malik100% (1)

- Ratio Analysis Bank AL Habib Ltd.Documento23 pagineRatio Analysis Bank AL Habib Ltd.Hussain M Raza33% (3)

- Allied Bank LimitedDocumento6 pagineAllied Bank LimitedWafa AliNessuna valutazione finora

- National Bank of Pakistan Internship ReportDocumento68 pagineNational Bank of Pakistan Internship Reportbbaahmad89100% (2)

- Intern Ship Report of Bank Alfalah Pakistan On Marketing (MBA)Documento39 pagineIntern Ship Report of Bank Alfalah Pakistan On Marketing (MBA)Yasir Khan50% (4)

- Internship Report On Foreign Exchange Activities of Jamuna Bank Mohakhali BranchDocumento29 pagineInternship Report On Foreign Exchange Activities of Jamuna Bank Mohakhali Branchকে.এস.এম. ইকরাম উল্যাহ71% (7)

- Internship Report On Habib Bank LimitedDocumento75 pagineInternship Report On Habib Bank LimitedMariyam Khan87% (15)

- Internship Sindh BankDocumento34 pagineInternship Sindh BankKR Burki100% (1)

- Bank of Punjab Internship UOGDocumento38 pagineBank of Punjab Internship UOGAhsanNessuna valutazione finora

- Internship Report On: "General Banking Activities of JANATA Bank LTD."Documento50 pagineInternship Report On: "General Banking Activities of JANATA Bank LTD."Tareq AlamNessuna valutazione finora

- Internship Report AB BankDocumento95 pagineInternship Report AB Bankshamimahmed313100% (2)

- Fraz Internship Report On BopDocumento37 pagineFraz Internship Report On BopRashid UosNessuna valutazione finora

- FFCDocumento17 pagineFFCAmna KhanNessuna valutazione finora

- Internship Report On BRAC Bank Ltd.Documento93 pagineInternship Report On BRAC Bank Ltd.Md. Likhon82% (17)

- Bank of KhyberDocumento48 pagineBank of KhyberSameer KhanNessuna valutazione finora

- Bop Internship ReportDocumento57 pagineBop Internship Reportahsan nadeem qadriNessuna valutazione finora

- Zahid JS Bank ReportDocumento114 pagineZahid JS Bank ReportSyed Zulqarnain HaiderNessuna valutazione finora

- UBL ReportDocumento48 pagineUBL ReportShabnam NazNessuna valutazione finora

- Allied Bank ProjectDocumento47 pagineAllied Bank ProjectChaudry RazaNessuna valutazione finora

- Habib Bank LimitedDocumento61 pagineHabib Bank Limitedmuhammadtaimoorkhan91% (11)

- HRM Project On ZTBLDocumento40 pagineHRM Project On ZTBLzohaibssNessuna valutazione finora

- ZTBL Internship Report PDFDocumento71 pagineZTBL Internship Report PDFibrahimNessuna valutazione finora

- ZTBL (New) Internship Report - SalmanDocumento44 pagineZTBL (New) Internship Report - SalmanUltimate MemerNessuna valutazione finora

- HB ProjectDocumento6 pagineHB ProjectSaad SulehriNessuna valutazione finora

- 160831051407Documento57 pagine160831051407Shahrukh MunirNessuna valutazione finora

- Muhammad RabnawazDocumento33 pagineMuhammad Rabnawazaqsamumtaz812Nessuna valutazione finora

- Waseem CV 2Documento1 paginaWaseem CV 2muhammad waseemNessuna valutazione finora

- It Is Important That You Fill Out This Application Completely. Please Type or PrintDocumento7 pagineIt Is Important That You Fill Out This Application Completely. Please Type or PrintNicky HouseNessuna valutazione finora

- Muhammad's ResumeDocumento1 paginaMuhammad's Resumemuhammad waseemNessuna valutazione finora

- Fme Understanding Emotional Intelligence PDFDocumento50 pagineFme Understanding Emotional Intelligence PDFrgscribd61Nessuna valutazione finora

- Money PDFDocumento22 pagineMoney PDFmuhammad waseemNessuna valutazione finora

- RM FinalDocumento32 pagineRM Finalmuhammad waseemNessuna valutazione finora

- Emotional Intelligence HandoutDocumento21 pagineEmotional Intelligence HandoutandresrangNessuna valutazione finora

- 43Documento12 pagine43muhammad waseem0% (1)

- Bank AlfalahDocumento62 pagineBank AlfalahMuhammed Siddiq KhanNessuna valutazione finora

- Internship Report InstructionsDocumento3 pagineInternship Report Instructionsmuhammad waseemNessuna valutazione finora

- Assignment Tital PageDocumento1 paginaAssignment Tital Pagemuhammad waseemNessuna valutazione finora

- Objective: Degree Year Marks Board/Universit yDocumento1 paginaObjective: Degree Year Marks Board/Universit ymuhammad waseemNessuna valutazione finora

- 14 - Business Plan TemplateDocumento13 pagine14 - Business Plan Templatebiglw05Nessuna valutazione finora

- ZTBLDocumento143 pagineZTBLmuhammad waseemNessuna valutazione finora

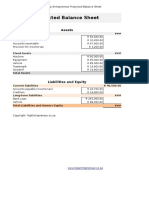

- Pro Forma Balance SheetDocumento1 paginaPro Forma Balance SheetChibuzo Turi OgbonnaNessuna valutazione finora

- Green, K., López, M., Wysocki, A., Kepner, K., Farnsworth, D. & and Clark, J. L.Documento3 pagineGreen, K., López, M., Wysocki, A., Kepner, K., Farnsworth, D. & and Clark, J. L.sharrelclNessuna valutazione finora

- Lecture 15 16 17Documento28 pagineLecture 15 16 17muhammad waseemNessuna valutazione finora

- IMC-Lecture 2Documento30 pagineIMC-Lecture 2muhammad waseemNessuna valutazione finora

- IMC-Lecture 2Documento30 pagineIMC-Lecture 2muhammad waseemNessuna valutazione finora

- IMC-Lecture 2Documento30 pagineIMC-Lecture 2muhammad waseemNessuna valutazione finora

- Budgetcircular2010 11Documento109 pagineBudgetcircular2010 11Vikas AnandNessuna valutazione finora

- My Affidavit For LawyerDocumento4 pagineMy Affidavit For LawyerJohn GuillermoNessuna valutazione finora

- Principles of Management Topic 7Documento26 paginePrinciples of Management Topic 7joebloggs1888Nessuna valutazione finora

- Housing Finance and NHBDocumento19 pagineHousing Finance and NHBiqbal_puneetNessuna valutazione finora

- Lembar - JWB - Soal - B - Sesi 2Documento11 pagineLembar - JWB - Soal - B - Sesi 2Sandi RiswandiNessuna valutazione finora

- Jms School Fee 2022-2023Documento1 paginaJms School Fee 2022-2023Dhiya UlhaqNessuna valutazione finora

- IB ChallanDocumento1 paginaIB ChallanPrasad HiremathNessuna valutazione finora

- APC 2017 English Information On The DayDocumento17 pagineAPC 2017 English Information On The DaySafwaan DanielsNessuna valutazione finora

- Regd Office: Unit No. 2, First Floor, 3A Pollock Street, Kolkata: 700 001, West BengalDocumento6 pagineRegd Office: Unit No. 2, First Floor, 3A Pollock Street, Kolkata: 700 001, West BengalCA Pallavi KNessuna valutazione finora

- Article 1207 Joint and SolidDocumento4 pagineArticle 1207 Joint and SolidRio PortoNessuna valutazione finora

- #5 PFRS 5Documento3 pagine#5 PFRS 5jaysonNessuna valutazione finora

- The Beginnings of FDI in E-CommerceDocumento16 pagineThe Beginnings of FDI in E-CommerceAbhinavNessuna valutazione finora

- Job Sheet Od Buku BesarDocumento13 pagineJob Sheet Od Buku Besarjuandry andryNessuna valutazione finora

- Washington Consensus ChapterDocumento12 pagineWashington Consensus ChapterBropa-sond Enoch KategayaNessuna valutazione finora

- Corporate Income Tax ActDocumento59 pagineCorporate Income Tax ActMateusz DłużniewskiNessuna valutazione finora

- Partnership Agreement - Sample - Taxguru - inDocumento7 paginePartnership Agreement - Sample - Taxguru - inAbhinav BharadwajNessuna valutazione finora

- Intacc Midterm Sw&QuizzesDocumento68 pagineIntacc Midterm Sw&QuizzesIris FenelleNessuna valutazione finora

- Tqs Finals Operations-AuditDocumento46 pagineTqs Finals Operations-AuditCristel TannaganNessuna valutazione finora

- YTL Buys Rival Lafarge Malaysia: Corporate NewsDocumento3 pagineYTL Buys Rival Lafarge Malaysia: Corporate NewsSatesh KalimuthuNessuna valutazione finora

- Investment Project (Mock Trading)Documento9 pagineInvestment Project (Mock Trading)sanaNessuna valutazione finora

- General Exception. A Bond That Otherwise Satisfies The Hedge Fund Bond TestDocumento1 paginaGeneral Exception. A Bond That Otherwise Satisfies The Hedge Fund Bond TestVIVEK SHARMANessuna valutazione finora