Potrebbero piacerti anche

- Budget Analysis: 2009-2010Documento11 pagineBudget Analysis: 2009-2010Waseem IshfaqNessuna valutazione finora

- Management Discussion and Analysis For The Financial YearDocumento6 pagineManagement Discussion and Analysis For The Financial Yearziaa senNessuna valutazione finora

- Air Freight in India - Macroeconomic IndicatorsDocumento5 pagineAir Freight in India - Macroeconomic IndicatorsnitinNessuna valutazione finora

- India: Steady Private and Public Consumption GrowthDocumento4 pagineIndia: Steady Private and Public Consumption GrowthRohan AtrawalkarNessuna valutazione finora

- Research Pulse: February 2020Documento14 pagineResearch Pulse: February 2020JeetuNessuna valutazione finora

- Economic Forecast Summary Argentina Oecd Economic Outlook November 2016Documento3 pagineEconomic Forecast Summary Argentina Oecd Economic Outlook November 2016Ciurlic MariaNessuna valutazione finora

- Industry and InfrastructureDocumento48 pagineIndustry and Infrastructuresudip dhuriNessuna valutazione finora

- Prezentare 1Documento16 paginePrezentare 1flaviusNessuna valutazione finora

- Indian Capital Goods IndustryDocumento19 pagineIndian Capital Goods IndustryanilkunjuNessuna valutazione finora

- State of Pakistan EconomyDocumento8 pagineState of Pakistan EconomyMuhammad KashifNessuna valutazione finora

- Alas John Paul Facon Raul Augustus Macrobite1Documento3 pagineAlas John Paul Facon Raul Augustus Macrobite1Raul Augustus D. FACONNessuna valutazione finora

- Bangladesh gw2011 Allpresentations 1 PDFDocumento83 pagineBangladesh gw2011 Allpresentations 1 PDFMostaque Ahmed AnntoNessuna valutazione finora

- Monthly Economic Bulletin: January 2011Documento15 pagineMonthly Economic Bulletin: January 2011lrochekellyNessuna valutazione finora

- Ekonomski Pregled OECD-aDocumento26 pagineEkonomski Pregled OECD-aTportal.hrNessuna valutazione finora

- Construction Industry Statistic, Jun 2017Documento26 pagineConstruction Industry Statistic, Jun 2017Jahid HasanNessuna valutazione finora

- Amey Patale 17-19 PGFinanceDocumento9 pagineAmey Patale 17-19 PGFinanceAMEY PATALENessuna valutazione finora

- 18-Article Text-94-1-10-20200929Documento14 pagine18-Article Text-94-1-10-20200929Angela SolanaNessuna valutazione finora

- Construction Industry ReportDocumento12 pagineConstruction Industry Reportyahoooo1234Nessuna valutazione finora

- Prezentare Ionut DumitruDocumento28 paginePrezentare Ionut DumitruAnonymous c3IPK8Nessuna valutazione finora

- Sinking Deeper: Lockdowns and Restrictions Have Hit Harder Than ExpectedDocumento6 pagineSinking Deeper: Lockdowns and Restrictions Have Hit Harder Than Expectedabhinavsingh4uNessuna valutazione finora

- Confronting Economic SlowdownDocumento26 pagineConfronting Economic Slowdownepra100% (1)

- Assignment Sample 1Documento22 pagineAssignment Sample 1Nguyen GingNessuna valutazione finora

- Should I Invest in Municipal Bonds RevisedDocumento7 pagineShould I Invest in Municipal Bonds RevisedKevin MeansNessuna valutazione finora

- India Economic Update June 23 2010Documento25 pagineIndia Economic Update June 23 2010Ning Ning Intan PermataNessuna valutazione finora

- Residential Market Update:: ResearchDocumento22 pagineResidential Market Update:: Researchjatin girotraNessuna valutazione finora

- 3Q17 Net Income Down 39.2% Y/y, Outlook Remains Poor: Universal Robina CorporationDocumento8 pagine3Q17 Net Income Down 39.2% Y/y, Outlook Remains Poor: Universal Robina Corporationherrewt rewterwNessuna valutazione finora

- Analisis Uang Beredar April 2019Documento10 pagineAnalisis Uang Beredar April 2019Deya Nadya KemalasariNessuna valutazione finora

- YG Country Fiche HU 2020 OCTOBERDocumento9 pagineYG Country Fiche HU 2020 OCTOBERAxel UhaldeNessuna valutazione finora

- Accounting Solution FinanceDocumento23 pagineAccounting Solution FinancePayal PatelNessuna valutazione finora

- Dabur Q3FY11 ResultDocumento17 pagineDabur Q3FY11 ResultjackjariNessuna valutazione finora

- FICCI Eco Survey 2011 12Documento9 pagineFICCI Eco Survey 2011 12Anirudh BhatjiwaleNessuna valutazione finora

- China+Property+Market+Overview Q4+2020 Logistics enDocumento14 pagineChina+Property+Market+Overview Q4+2020 Logistics enKhriztopher PhayNessuna valutazione finora

- NT Daily CommentaryDocumento8 pagineNT Daily Commentaryonmargin100% (2)

- Splicing of Time Series - GDP of IndiaDocumento7 pagineSplicing of Time Series - GDP of Indiaharshalshah3110Nessuna valutazione finora

- Splicing of Time Series - GDP of IndiaDocumento7 pagineSplicing of Time Series - GDP of Indiaharshalshah3110Nessuna valutazione finora

- 2021 - YOUniversity Deal Challenge - SaurabhDocumento22 pagine2021 - YOUniversity Deal Challenge - SaurabhRadhika AgrawalNessuna valutazione finora

- A Brief On Rangrajan Committee Report 2011-12: Presented by Nithin.K S4 Mba JBSDocumento7 pagineA Brief On Rangrajan Committee Report 2011-12: Presented by Nithin.K S4 Mba JBSNithin KuniyilNessuna valutazione finora

- Inflation: Table 7.1: Historical Trend in Headline InflationDocumento27 pagineInflation: Table 7.1: Historical Trend in Headline InflationBilal AhmedNessuna valutazione finora

- WING Wingstop Investor Presentation June 2018Documento37 pagineWING Wingstop Investor Presentation June 2018Ala BasterNessuna valutazione finora

- Atanu, Neena, Priyabadan G5Documento36 pagineAtanu, Neena, Priyabadan G5access_swatiNessuna valutazione finora

- Paul Kasriel: Great Depression, Just The FactsDocumento7 paginePaul Kasriel: Great Depression, Just The Factshblodget100% (3)

- 2014 02 06 PH S Mpi PDFDocumento4 pagine2014 02 06 PH S Mpi PDFJNessuna valutazione finora

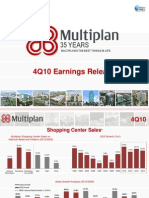

- Apresentao 4 QENGDocumento17 pagineApresentao 4 QENGMultiplan RINessuna valutazione finora

- Credit Analysis of Premier Foods PLC - Sample 1Documento14 pagineCredit Analysis of Premier Foods PLC - Sample 1BethelNessuna valutazione finora

- IndiaEconomicsOverheating090207 MF PDFDocumento4 pagineIndiaEconomicsOverheating090207 MF PDFdidwaniasNessuna valutazione finora

- Revenue Statistics in Africa 2020 Democratic Republic of The CongoDocumento2 pagineRevenue Statistics in Africa 2020 Democratic Republic of The CongoDawitNessuna valutazione finora

- SER 2021 Chapter 04Documento4 pagineSER 2021 Chapter 04IPNessuna valutazione finora

- Bangladesh Seventh Five Year Plan - FinalDocumento50 pagineBangladesh Seventh Five Year Plan - FinalsumondccNessuna valutazione finora

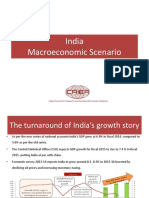

- Ok Macro IndiaDocumento22 pagineOk Macro IndiaSaurabh JadhavNessuna valutazione finora

- Jefferis Et Al 2020 Final PaperDocumento40 pagineJefferis Et Al 2020 Final PaperJose Antonio ChicurraneNessuna valutazione finora

- Arthur Kachemba-ST4S38-V1 - Assignment 2Documento12 pagineArthur Kachemba-ST4S38-V1 - Assignment 2Arthur Kachemba50% (2)

- ICCT Comments Renewable Fuel Standard Program Rvo Noda 20171019Documento5 pagineICCT Comments Renewable Fuel Standard Program Rvo Noda 20171019The International Council on Clean TransportationNessuna valutazione finora

- Key Economic Indicators IndiaDocumento49 pagineKey Economic Indicators IndiavivekNessuna valutazione finora

- WARC Global Ad Trends State of The Industry 2020 21 SAMPLEDocumento31 pagineWARC Global Ad Trends State of The Industry 2020 21 SAMPLEVanessa FonsecaNessuna valutazione finora

- Ghana Real Economic Sectors Performances.Documento29 pagineGhana Real Economic Sectors Performances.Opoku Afram PaulNessuna valutazione finora

- FY2009 Financial ResultsDocumento17 pagineFY2009 Financial ResultstinkrboxNessuna valutazione finora

- MER - Jan - 2022 - 15 Feb - FinalDocumento30 pagineMER - Jan - 2022 - 15 Feb - FinalShemeem SNessuna valutazione finora

- WING Investor Presentation IR Website 2018 WingstopDocumento37 pagineWING Investor Presentation IR Website 2018 WingstopAla BasterNessuna valutazione finora

- Creating Strategic Value through Financial TechnologyDa EverandCreating Strategic Value through Financial TechnologyNessuna valutazione finora

- Digital Transformation Payday: Navigate the Hype, Lower the Risks, Increase Return on InvestmentsDa EverandDigital Transformation Payday: Navigate the Hype, Lower the Risks, Increase Return on InvestmentsNessuna valutazione finora

- Grsitl: Package Section LineDocumento6 pagineGrsitl: Package Section LineAmit GuptaNessuna valutazione finora

- Study On Analysis of Tariff Orders&other Orders of State Electricity Regulatory Commissions PDFDocumento854 pagineStudy On Analysis of Tariff Orders&other Orders of State Electricity Regulatory Commissions PDFAmit GuptaNessuna valutazione finora

- Report On The Performance of State Power Utilites For The Years 2009-10 To 2011-12Documento236 pagineReport On The Performance of State Power Utilites For The Years 2009-10 To 2011-12Amit GuptaNessuna valutazione finora

- Basic Statistics On Indian Petroleum & Natural GasDocumento53 pagineBasic Statistics On Indian Petroleum & Natural GasAmit GuptaNessuna valutazione finora

- Nit 1Documento2 pagineNit 1Amit GuptaNessuna valutazione finora

- LNG TerminalDocumento17 pagineLNG TerminalAmit GuptaNessuna valutazione finora

- Stu Notes Sess 1 FoundationDocumento25 pagineStu Notes Sess 1 FoundationAmit GuptaNessuna valutazione finora

- SIP - Joining Report Form.Documento1 paginaSIP - Joining Report Form.Amit GuptaNessuna valutazione finora

- Student Int. AssignmentDocumento2 pagineStudent Int. AssignmentAmit GuptaNessuna valutazione finora

- A Project Study Report On: Training Undertaken atDocumento59 pagineA Project Study Report On: Training Undertaken atAmit GuptaNessuna valutazione finora

- Term III Schedule Week-1 (Student Version)Documento2 pagineTerm III Schedule Week-1 (Student Version)Amit GuptaNessuna valutazione finora

- Financial Market and Institutions Ch16Documento8 pagineFinancial Market and Institutions Ch16kellyNessuna valutazione finora

- FMR MCBDocumento12 pagineFMR MCBSaad TanvirNessuna valutazione finora

- Mindset Development Organisation Annual Report 2012Documento29 pagineMindset Development Organisation Annual Report 2012chenyi55253779Nessuna valutazione finora

- 05Documento19 pagine05Emre TürkmenNessuna valutazione finora

- The Natural Rate of Interest: Drivers and Implications For PolicyDocumento24 pagineThe Natural Rate of Interest: Drivers and Implications For PolicyClasicos DominicanosNessuna valutazione finora

- PT 365 EconomyDocumento85 paginePT 365 EconomySakshi KatyalNessuna valutazione finora

- Goal Based Investing Calculator Mar 2016 2Documento6 pagineGoal Based Investing Calculator Mar 2016 2seemarani12713Nessuna valutazione finora

- Unit Test 11: Answer All Thirty Questions. There Is One Mark Per QuestionDocumento6 pagineUnit Test 11: Answer All Thirty Questions. There Is One Mark Per QuestionQuảng KimNessuna valutazione finora

- Gold Standard PDFDocumento23 pagineGold Standard PDFfarukeeeeeNessuna valutazione finora

- Basics of Aircraft Market Analysis v1Documento30 pagineBasics of Aircraft Market Analysis v1avianovaNessuna valutazione finora

- Assignment No-2: B. Assignment Submission InstructionsDocumento14 pagineAssignment No-2: B. Assignment Submission InstructionsshuchimNessuna valutazione finora

- 13 - 34 The Influence of Monetary and Fiscal Policy On Aggregate DemandDocumento36 pagine13 - 34 The Influence of Monetary and Fiscal Policy On Aggregate DemandDy ANessuna valutazione finora

- Pakistan Strategy (The Cyclical Upturn - Receding Headwinds Offer Scope For Further Re-Rating)Documento35 paginePakistan Strategy (The Cyclical Upturn - Receding Headwinds Offer Scope For Further Re-Rating)muddasir1980Nessuna valutazione finora

- Macroeconomics Question Bank - MRU (Without Answers)Documento97 pagineMacroeconomics Question Bank - MRU (Without Answers)saif ur rehmanNessuna valutazione finora

- EconomicsDocumento12 pagineEconomicsDeeksha PakhariyaNessuna valutazione finora

- 9708 Economics Example Candidate Responses 2012 InddDocumento158 pagine9708 Economics Example Candidate Responses 2012 InddHareemFatima0% (1)

- Sample Test - No KeysDocumento4 pagineSample Test - No KeysQUỲNH BÙI NGỌC KHÁNHNessuna valutazione finora

- 9 - ch27 Money, Interest, Real GDP, and The Price LevelDocumento48 pagine9 - ch27 Money, Interest, Real GDP, and The Price Levelcool_mechNessuna valutazione finora

- Harris Construction Cost BulletinDocumento2 pagineHarris Construction Cost BulletinAaron SteeleNessuna valutazione finora

- Neetha John Cia - 1 GM (20mbar0328)Documento4 pagineNeetha John Cia - 1 GM (20mbar0328)neetha johnNessuna valutazione finora

- Global Economic Crisis: Causes, Impact On Indian Economy, Agriculture and FisheriesDocumento7 pagineGlobal Economic Crisis: Causes, Impact On Indian Economy, Agriculture and FisheriesMadhuri JhaveriNessuna valutazione finora

- Bill Marsha WhiteDocumento14 pagineBill Marsha WhiteFinancial SenseNessuna valutazione finora

- What Is MoneyDocumento9 pagineWhat Is Moneymariya0% (1)

- Chapter #5Documento11 pagineChapter #5Aisha rashidNessuna valutazione finora

- Steve Keen Final OutlookDocumento20 pagineSteve Keen Final Outlookaao5269Nessuna valutazione finora

- Inflation and The Quantity Theory of MoneyDocumento22 pagineInflation and The Quantity Theory of MoneyBình Nguyễn ĐăngNessuna valutazione finora

- Collabetition: 3 Principles For The Creative Person in All of UsDocumento146 pagineCollabetition: 3 Principles For The Creative Person in All of UsTaiNessuna valutazione finora

- TEGI0600Documento54 pagineTEGI0600Ely TharNessuna valutazione finora

- Economic and Legal Analysis of Inflation and DeflationDocumento23 pagineEconomic and Legal Analysis of Inflation and Deflationbindu priyaNessuna valutazione finora

- EC1009 May ExamDocumento10 pagineEC1009 May ExamFabioNessuna valutazione finora