Potrebbero piacerti anche

- Order To Cash BPO A Complete Guide - 2020 EditionDa EverandOrder To Cash BPO A Complete Guide - 2020 EditionNessuna valutazione finora

- SEPADirectDebit AX2009SP1 AX2012 PDFDocumento31 pagineSEPADirectDebit AX2009SP1 AX2012 PDFJessica MengNessuna valutazione finora

- Public Cloud ERP for Small or Midsize Businesses A Complete Guide - 2019 EditionDa EverandPublic Cloud ERP for Small or Midsize Businesses A Complete Guide - 2019 EditionNessuna valutazione finora

- SEPA Direct Debit RulesDocumento8 pagineSEPA Direct Debit Rulesh1760472Nessuna valutazione finora

- ING Payments MT940 Format DescriptionDocumento26 pagineING Payments MT940 Format Descriptionanandbajaj0Nessuna valutazione finora

- BNY MellonDocumento3 pagineBNY MellonRajat SharmaNessuna valutazione finora

- SAP Transactional Banking A Clear and Concise ReferenceDa EverandSAP Transactional Banking A Clear and Concise ReferenceNessuna valutazione finora

- Proposal BIDocumento7 pagineProposal BINik Syukriah Amin100% (1)

- Swift Payment SAPDocumento3 pagineSwift Payment SAPsuva61750% (2)

- PV PPT DIGITAL WALLET LatestDocumento56 paginePV PPT DIGITAL WALLET Latestravi dasariNessuna valutazione finora

- Composable Infrastructure: APJ Data Center SEVTDocumento10 pagineComposable Infrastructure: APJ Data Center SEVTAnonymous SR0AF3Nessuna valutazione finora

- FICO Interview QuestionsDocumento177 pagineFICO Interview QuestionsNagaratna ReddyNessuna valutazione finora

- Vtiger CRM Integration Guide Open SourceDocumento12 pagineVtiger CRM Integration Guide Open SourceomariduranNessuna valutazione finora

- 24-Hour UBL Phone Banking UAN 111 - 825 - 888: Greeting For EnglishDocumento1 pagina24-Hour UBL Phone Banking UAN 111 - 825 - 888: Greeting For Englishsweet sharyNessuna valutazione finora

- Net Banking Mini ProjectDocumento65 pagineNet Banking Mini ProjectTrupti SuryawanshiNessuna valutazione finora

- Sap in PakistanDocumento16 pagineSap in PakistanArslan Ali100% (3)

- Netsuite Electronic Payments: Securely Automate EFT Payments and Collections With A Single Global SolutionDocumento5 pagineNetsuite Electronic Payments: Securely Automate EFT Payments and Collections With A Single Global SolutionJawad HaiderNessuna valutazione finora

- Swift For Corporates OverviewDocumento61 pagineSwift For Corporates Overviewkris_acc85100% (1)

- Renjith R Pillai - CV MARCH 2018Documento3 pagineRenjith R Pillai - CV MARCH 2018Renjith R PillaiNessuna valutazione finora

- HSBCnet - MY MT940 File SpecificationDocumento8 pagineHSBCnet - MY MT940 File SpecificationGhosh2Nessuna valutazione finora

- Bank ReconciliationDocumento19 pagineBank ReconciliationKalyan KakustamNessuna valutazione finora

- Accenture ISO 20022 Opportunities APACDocumento12 pagineAccenture ISO 20022 Opportunities APACtbt32Nessuna valutazione finora

- Oracle Finance Trial Balance and Ledger DetailsDocumento59 pagineOracle Finance Trial Balance and Ledger DetailsKatie RuizNessuna valutazione finora

- ClarificationsDocumento15 pagineClarificationsArun KumarNessuna valutazione finora

- Oracle - 1Z0-518 Oracle EBS R12.1 Receivables EssentialsDocumento5 pagineOracle - 1Z0-518 Oracle EBS R12.1 Receivables EssentialsAnurag SinghNessuna valutazione finora

- Bank Portfolio ManagementDocumento6 pagineBank Portfolio ManagementAbhay VelayudhanNessuna valutazione finora

- Idoc Basic Document GokulDocumento29 pagineIdoc Basic Document GokulK.r. KrrishNessuna valutazione finora

- F-13 Vendor Automatic Account ClearingDocumento6 pagineF-13 Vendor Automatic Account ClearingDipak kumar PradhanNessuna valutazione finora

- Finacle OriginationDocumento6 pagineFinacle OriginationAnand KumarNessuna valutazione finora

- Sap Fico: About The TrainerDocumento5 pagineSap Fico: About The TrainerkhushbooNessuna valutazione finora

- Travel Bill Tracking SystemDocumento10 pagineTravel Bill Tracking SystemVKM20130% (1)

- Sap Financials - ENTERPRISE STRUCTURE - Interview Q's With A'sDocumento15 pagineSap Financials - ENTERPRISE STRUCTURE - Interview Q's With A'sKarthik SelvarajNessuna valutazione finora

- Real Time Treasury Episode2Documento21 pagineReal Time Treasury Episode2HACNessuna valutazione finora

- Unit - 1: Automatic Payments Lesson: Explaining The Automatic Payment RunDocumento3 pagineUnit - 1: Automatic Payments Lesson: Explaining The Automatic Payment RunHaneesh DevarasettyNessuna valutazione finora

- Better Bank Monitor PDFDocumento33 pagineBetter Bank Monitor PDFdavid cooperfeldNessuna valutazione finora

- Cash Manaagement ConceptDocumento4 pagineCash Manaagement ConceptRoberto De FlumeriNessuna valutazione finora

- Flowserve SAP S4 HANA - Basic Fiori Navigation - OldDocumento32 pagineFlowserve SAP S4 HANA - Basic Fiori Navigation - OldraghuNessuna valutazione finora

- Integration Framework For SAP Business One - Overview - HelpPortalDocumento29 pagineIntegration Framework For SAP Business One - Overview - HelpPortalWilson Chalar VargasNessuna valutazione finora

- Codification Annex ING Format Descriptions Strategic v1.0 - tcm162-110480Documento24 pagineCodification Annex ING Format Descriptions Strategic v1.0 - tcm162-110480rahul_agrawal165Nessuna valutazione finora

- Blackline For Oracle: Transform Your Financial CloseDocumento24 pagineBlackline For Oracle: Transform Your Financial ClosesriramNessuna valutazione finora

- EU SEPA Credit Transfer Rulebook v8.1 ApprovedDocumento115 pagineEU SEPA Credit Transfer Rulebook v8.1 ApprovedMonica PopoviciNessuna valutazione finora

- Curriculum Vitae: Career ObjectiveDocumento2 pagineCurriculum Vitae: Career ObjectiveJobs JobbsNessuna valutazione finora

- Implementation of Ghana Retail Payment Systems InfrastructureDocumento14 pagineImplementation of Ghana Retail Payment Systems InfrastructureGhanaWeb Editorial100% (1)

- CIPSP Jan2018RDocumento7 pagineCIPSP Jan2018RaNessuna valutazione finora

- Collections 12 0Documento76 pagineCollections 12 0Pearl AsiamahNessuna valutazione finora

- Swift mt940 942Documento13 pagineSwift mt940 942Sulaiman YusufNessuna valutazione finora

- Qatar Vat Implementation RoadmapDocumento8 pagineQatar Vat Implementation RoadmapKhurram HussainNessuna valutazione finora

- Deepa Karuppiah SAP FICODocumento4 pagineDeepa Karuppiah SAP FICO437ko7Nessuna valutazione finora

- General Ledger ReportsDocumento106 pagineGeneral Ledger ReportsVamsiNessuna valutazione finora

- DBS IDEAL CURATED - Case Study - Screening Solution V1Documento6 pagineDBS IDEAL CURATED - Case Study - Screening Solution V1Himanshu GhadigaonkarNessuna valutazione finora

- Company's Name: Software's Name: Octopus Microfinance Octopus Microfinance SuiteDocumento12 pagineCompany's Name: Software's Name: Octopus Microfinance Octopus Microfinance Suitejbc3691Nessuna valutazione finora

- Mpbim Project Report SapDocumento29 pagineMpbim Project Report SapShashidhar HanjiNessuna valutazione finora

- 16 Unifying Econometrics TsendsurenDocumento18 pagine16 Unifying Econometrics TsendsurenBaatar SukhbaatarNessuna valutazione finora

- India Merchant Agreement Terms - ConditionsDocumento16 pagineIndia Merchant Agreement Terms - ConditionsBaatar SukhbaatarNessuna valutazione finora

- State of CX Financial - v01Documento14 pagineState of CX Financial - v01Baatar SukhbaatarNessuna valutazione finora

- Security Orchestration, Automation and Response (SOAR) CapabilitiesDocumento17 pagineSecurity Orchestration, Automation and Response (SOAR) CapabilitiesBaatar SukhbaatarNessuna valutazione finora

- Optimizing Siem With Log ManagementDocumento13 pagineOptimizing Siem With Log ManagementBaatar SukhbaatarNessuna valutazione finora

- Red Hat Process Automation Manager: Automate Business DecisionsDocumento3 pagineRed Hat Process Automation Manager: Automate Business DecisionsBaatar SukhbaatarNessuna valutazione finora

- Unveiling The Myth of Windows 10 MVP White PaperDocumento5 pagineUnveiling The Myth of Windows 10 MVP White PaperBaatar SukhbaatarNessuna valutazione finora

- Nuodb Neobank WP PDFDocumento6 pagineNuodb Neobank WP PDFBaatar SukhbaatarNessuna valutazione finora

- Services Cisco Smartnet Tei StudyDocumento19 pagineServices Cisco Smartnet Tei StudyBaatar SukhbaatarNessuna valutazione finora

- Watchguard Dimension: Oceans of Data Instantly Become Security IntelligenceDocumento1 paginaWatchguard Dimension: Oceans of Data Instantly Become Security IntelligenceBaatar SukhbaatarNessuna valutazione finora

- COBIT 2019 vs. COBIT 5Documento6 pagineCOBIT 2019 vs. COBIT 5Baatar SukhbaatarNessuna valutazione finora

- Watchguard Firebox T15: HardwareDocumento16 pagineWatchguard Firebox T15: HardwareBaatar SukhbaatarNessuna valutazione finora

- FPS Rules - v13.2 - (Effective 1st March 2019)Documento109 pagineFPS Rules - v13.2 - (Effective 1st March 2019)Baatar SukhbaatarNessuna valutazione finora

- Identity20gov20 20the 10 Universal Truths of Identity and Access Management Ebook 25057Documento14 pagineIdentity20gov20 20the 10 Universal Truths of Identity and Access Management Ebook 25057Baatar SukhbaatarNessuna valutazione finora

- PowerShell CMD Line Conversion Guide ADDocumento4 paginePowerShell CMD Line Conversion Guide ADManuel Pirez NunezNessuna valutazione finora

- Common Loan Origination (InfoSys)Documento2 pagineCommon Loan Origination (InfoSys)Baatar SukhbaatarNessuna valutazione finora

- Introduction To AccountingDocumento57 pagineIntroduction To AccountingJustine MaravillaNessuna valutazione finora

- Perpetual - Financial StatementsDocumento4 paginePerpetual - Financial StatementsJeon Cyrone CuachonNessuna valutazione finora

- Finex ServicesDocumento3 pagineFinex Servicesggn08Nessuna valutazione finora

- Cityam 2010-10-29Documento52 pagineCityam 2010-10-29City A.M.Nessuna valutazione finora

- Assignment On NCC BankDocumento44 pagineAssignment On NCC Bankhasan633100% (1)

- CISI Exam Booking Instructions-1Documento4 pagineCISI Exam Booking Instructions-1simon.dk.designerNessuna valutazione finora

- Delhi To Rudrapur: Abhibus TicketDocumento2 pagineDelhi To Rudrapur: Abhibus TicketKrishan SharmaNessuna valutazione finora

- Two MillionDocumento19 pagineTwo MillionFazal Ahmed100% (1)

- Certificate in Bookkeeping and Accounting Level 2Documento38 pagineCertificate in Bookkeeping and Accounting Level 2McKay TheinNessuna valutazione finora

- Mirae Factsheet April2017Documento16 pagineMirae Factsheet April2017Dashang G. MakwanaNessuna valutazione finora

- PRED 3210 Chapter 4Documento8 paginePRED 3210 Chapter 4Jheny PalamaraNessuna valutazione finora

- Money in The Nation's EconomyDocumento18 pagineMoney in The Nation's EconomyAnne Gatchalian67% (3)

- Problem 1-1 To 1-3 Intermediate Accounting (Vol 1)Documento8 pagineProblem 1-1 To 1-3 Intermediate Accounting (Vol 1)Margarette TumbadoNessuna valutazione finora

- CF Bake House: Project ReportDocumento21 pagineCF Bake House: Project ReportRajinikkanthNessuna valutazione finora

- Bajaj Allianz InsuranceDocumento93 pagineBajaj Allianz InsuranceswatiNessuna valutazione finora

- SOE11144 Global Business Economics and FinanceDocumento12 pagineSOE11144 Global Business Economics and FinanceNadia RiazNessuna valutazione finora

- Fabm ExamDocumento3 pagineFabm ExamRonald AlmagroNessuna valutazione finora

- Request For Strategic Advice On Business Schools in Scottish UniversitiesDocumento22 pagineRequest For Strategic Advice On Business Schools in Scottish UniversitiesThe Royal Society of EdinburghNessuna valutazione finora

- Valuation of Bonds and SharesDocumento39 pagineValuation of Bonds and Shareskunalacharya5Nessuna valutazione finora

- Key Facts Missold IVA Legal PartnerDocumento1 paginaKey Facts Missold IVA Legal PartnerAnthony RobertsNessuna valutazione finora

- A Study On Claims ManagementDocumento77 pagineA Study On Claims Managementarjunmba119624100% (2)

- Assignment - 2: Semester Spring 2021Documento3 pagineAssignment - 2: Semester Spring 2021Amina HamidNessuna valutazione finora

- Welcome To Presentation On Discharge of SuretyDocumento18 pagineWelcome To Presentation On Discharge of SuretyAmit Gurav94% (16)

- Louw 3Documento27 pagineLouw 3ZeabMariaNessuna valutazione finora

- Monetary Policy and Central Banking PDFDocumento2 pagineMonetary Policy and Central Banking PDFTrisia Corinne JaringNessuna valutazione finora

- Accounting NotesDocumento6 pagineAccounting NotesHimanshu SinghNessuna valutazione finora

- AccountingDocumento8 pagineAccountingfransiscaNessuna valutazione finora

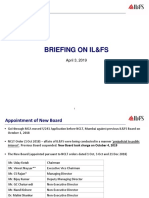

- ILFS Briefing (April 2019)Documento15 pagineILFS Briefing (April 2019)Richard DierdreNessuna valutazione finora

- Exhaustive List of Analytics Companies in IndiaDocumento4 pagineExhaustive List of Analytics Companies in IndiagoodthoughtsNessuna valutazione finora

- iPAY International S.A. 2014Documento20 pagineiPAY International S.A. 2014LuxembourgAtaGlanceNessuna valutazione finora