Potrebbero piacerti anche

- Corporate Finance Formulas: A Simple IntroductionDa EverandCorporate Finance Formulas: A Simple IntroductionValutazione: 4 su 5 stelle4/5 (8)

- Option Valuation: Numerical ExampleDocumento15 pagineOption Valuation: Numerical ExampleMarwa HassanNessuna valutazione finora

- BKM, Chap 16Documento16 pagineBKM, Chap 16rob_jiangNessuna valutazione finora

- Risk Management Solution To Chapter 15Documento3 pagineRisk Management Solution To Chapter 15BombitaNessuna valutazione finora

- Workshop 9Documento8 pagineWorkshop 9Hakim AzmiNessuna valutazione finora

- Financial DerivativesDocumento30 pagineFinancial DerivativesBevNessuna valutazione finora

- Derivative Markets Solutions'Documento30 pagineDerivative Markets Solutions'Kamy ZhuNessuna valutazione finora

- Chapter 24: Options and Corporate Finance: Extensions and ApplicationsDocumento15 pagineChapter 24: Options and Corporate Finance: Extensions and ApplicationsDigital Marketing AryoNessuna valutazione finora

- Options PricingDocumento17 pagineOptions Pricingvodakaa100% (1)

- Chap 4: Comparing Net Present Value, Decision Trees, and Real OptionsDocumento51 pagineChap 4: Comparing Net Present Value, Decision Trees, and Real OptionsPrabhpuneet PandherNessuna valutazione finora

- Brealey. Myers. Allen Chapter 22 SolutionDocumento8 pagineBrealey. Myers. Allen Chapter 22 SolutionPulkit Aggarwal100% (1)

- Problem Set 5 Solution-2 CopieDocumento5 pagineProblem Set 5 Solution-2 CopieCarol VarelaNessuna valutazione finora

- 6 - Tutorial FINS3625S2Yr2018Week 6 Tutorial SolutionsDocumento9 pagine6 - Tutorial FINS3625S2Yr2018Week 6 Tutorial SolutionsChrisNessuna valutazione finora

- Tutorial - Investment and Financial AnalysisDocumento40 pagineTutorial - Investment and Financial AnalysiskelvinplayzgamesNessuna valutazione finora

- 35757845Documento28 pagine35757845omprakashNessuna valutazione finora

- Investment Rev23Documento7 pagineInvestment Rev23tapiwanashejakaNessuna valutazione finora

- HW 2Documento4 pagineHW 2TaySyYinNessuna valutazione finora

- Solution To Derivatives Markets: SOA Exam MFE and CAS Exam 3 FEDocumento25 pagineSolution To Derivatives Markets: SOA Exam MFE and CAS Exam 3 FENga BuiNessuna valutazione finora

- Essentials of Investments (BKM 7 Ed.) Answers To Suggested Problems - Lecture 1Documento4 pagineEssentials of Investments (BKM 7 Ed.) Answers To Suggested Problems - Lecture 1masterchocoNessuna valutazione finora

- How Traders Manage Their RisksDocumento23 pagineHow Traders Manage Their RisksWania JksNessuna valutazione finora

- Options and Their ValuationDocumento20 pagineOptions and Their ValuationappiippaNessuna valutazione finora

- BRIGHAM CH 19 SM 3ce - REVISEDDocumento11 pagineBRIGHAM CH 19 SM 3ce - REVISEDVu Khanh LeNessuna valutazione finora

- Derivative Markets Solutions PDFDocumento30 pagineDerivative Markets Solutions PDFPeter HuaNessuna valutazione finora

- Midsem SolutionDocumento4 pagineMidsem SolutionEklavyaNessuna valutazione finora

- 7 Introduction To Binomial TreesDocumento25 pagine7 Introduction To Binomial TreesDragosCavescuNessuna valutazione finora

- Microeconomics Assignment 1: I 2i 3i 4iDocumento5 pagineMicroeconomics Assignment 1: I 2i 3i 4iYash AgarwalNessuna valutazione finora

- 3.3.2.2 Explain Stock Valuation Alolod DelicanoDocumento11 pagine3.3.2.2 Explain Stock Valuation Alolod DelicanoaiahNessuna valutazione finora

- Ex3 Put OptionDocumento5 pagineEx3 Put OptionP MarpaungNessuna valutazione finora

- Introductory DerivativesDocumento2 pagineIntroductory DerivativesnickbuchNessuna valutazione finora

- Answers To Problem Sets: Introduction To Risk and ReturnDocumento11 pagineAnswers To Problem Sets: Introduction To Risk and ReturnKksksk IsjsjNessuna valutazione finora

- SOA MFE 76 Practice Ques SolsDocumento70 pagineSOA MFE 76 Practice Ques SolsGracia DongNessuna valutazione finora

- Solutions To Chapter 7Documento12 pagineSolutions To Chapter 7Naa'irah RehmanNessuna valutazione finora

- Derivatives Test 3 SolnDocumento12 pagineDerivatives Test 3 SolnHetviNessuna valutazione finora

- Chapter 6 Example Trips LogisticsDocumento10 pagineChapter 6 Example Trips LogisticsYUSHIHUINessuna valutazione finora

- Solution Manual For Operations and Supply Chain Management Russell Taylor 8th EditionDocumento20 pagineSolution Manual For Operations and Supply Chain Management Russell Taylor 8th Editionabettorcorpsew52rrcNessuna valutazione finora

- HW For M8 - Hedging With OptionsDocumento3 pagineHW For M8 - Hedging With OptionsNiyati ShahNessuna valutazione finora

- Binomial and Black Scholes - 111153Documento18 pagineBinomial and Black Scholes - 111153merijan31773Nessuna valutazione finora

- Problem Set 5Documento4 pagineProblem Set 5Carol VarelaNessuna valutazione finora

- Financial Derivative (90 M Session)Documento33 pagineFinancial Derivative (90 M Session)nicero555Nessuna valutazione finora

- Answers To Practice Questions: Introduction To Risk, Return, and The Opportunity Cost of CapitalDocumento9 pagineAnswers To Practice Questions: Introduction To Risk, Return, and The Opportunity Cost of CapitalShireen QaiserNessuna valutazione finora

- BKM 10e Chap013Documento18 pagineBKM 10e Chap013jl123123Nessuna valutazione finora

- Mini Case Chapter 8Documento8 pagineMini Case Chapter 8William Y. OspinaNessuna valutazione finora

- E51 Curswap Eur UsdDocumento2 pagineE51 Curswap Eur UsdkoushikNessuna valutazione finora

- Soln CH 21 Option ValDocumento10 pagineSoln CH 21 Option ValSilviu TrebuianNessuna valutazione finora

- 21FA ISOM2700 Practice Set7 SolDocumento5 pagine21FA ISOM2700 Practice Set7 Sol楊凱卉Nessuna valutazione finora

- Investment and Portfolio Management Session 3 SolutionsDocumento3 pagineInvestment and Portfolio Management Session 3 Solutions李佳南Nessuna valutazione finora

- Single Index ModelDocumento7 pagineSingle Index ModelNeelam MadarapuNessuna valutazione finora

- Derivative Markets SolutionsDocumento30 pagineDerivative Markets Solutionsnk7350100% (2)

- Shreve SolutionsDocumento60 pagineShreve SolutionsJason Huang100% (1)

- Exercises Chapter 12 1.: Income Beginning Price Ending Price Beginning Price Beginning PriceDocumento4 pagineExercises Chapter 12 1.: Income Beginning Price Ending Price Beginning Price Beginning PriceTrịnh Mỹ PhươngNessuna valutazione finora

- McDonald Chapter9Documento11 pagineMcDonald Chapter9Tu TruongNessuna valutazione finora

- M 7 Problem Set SolutionsDocumento9 pagineM 7 Problem Set SolutionsNiyati ShahNessuna valutazione finora

- Module 12 - Option Pricing - Binomial - Black Scholes - How To Do It - UPDATEDDocumento20 pagineModule 12 - Option Pricing - Binomial - Black Scholes - How To Do It - UPDATEDBaher WilliamNessuna valutazione finora

- Trip Logistics CaseDocumento20 pagineTrip Logistics CaseLingamurthy BNessuna valutazione finora

- Return, Risk and The Security Market LineDocumento25 pagineReturn, Risk and The Security Market Linewww_peru9788Nessuna valutazione finora

- Fin SolutionsDocumento9 pagineFin SolutionsTania Kalila HernandezNessuna valutazione finora

- Stochastic Calculus For Finance Shreve SolutionsDocumento60 pagineStochastic Calculus For Finance Shreve SolutionsJason Wu67% (3)

- FINC3014 Topic 8 SolutionsDocumento5 pagineFINC3014 Topic 8 Solutionssuitup100Nessuna valutazione finora

- 2018info MATH3974Documento2 pagine2018info MATH3974suitup100Nessuna valutazione finora

- FINC3014 Topic 11 SolutionsDocumento5 pagineFINC3014 Topic 11 Solutionssuitup100Nessuna valutazione finora

- FINC2011 Tutorial 5Documento10 pagineFINC2011 Tutorial 5suitup100100% (4)

- Option 02Documento62 pagineOption 02suitup100Nessuna valutazione finora

- FINC3012 MidSem NotesDocumento4 pagineFINC3012 MidSem Notessuitup100Nessuna valutazione finora

- FINC2011 Tutorial 4Documento7 pagineFINC2011 Tutorial 4suitup100100% (3)

- 21 Electric Charge & Electric FieldDocumento25 pagine21 Electric Charge & Electric Fieldsuitup100Nessuna valutazione finora

- Study Methods What To StudyDocumento3 pagineStudy Methods What To Studysuitup100Nessuna valutazione finora

- FINC2011 Tutorial 1 QuestionsDocumento4 pagineFINC2011 Tutorial 1 Questionssuitup100Nessuna valutazione finora

- Unit of Study Outline: Corporate Finance IIDocumento8 pagineUnit of Study Outline: Corporate Finance IIsuitup100Nessuna valutazione finora

- Lab 12Documento7 pagineLab 12suitup100Nessuna valutazione finora

- Why Beta Shifts As The Return Interval Changes: Munich Personal Repec ArchiveDocumento6 pagineWhy Beta Shifts As The Return Interval Changes: Munich Personal Repec Archivesuitup100Nessuna valutazione finora

- Chemistry Unspoken Rules: Scientific DiagramsDocumento2 pagineChemistry Unspoken Rules: Scientific Diagramssuitup100Nessuna valutazione finora

- 03 9708 22 MS Final Scoris 10032023Documento21 pagine03 9708 22 MS Final Scoris 10032023Kalsoom SoniNessuna valutazione finora

- FIDIC Blue - Green Book - Dredging & Reclamation Works - 2006Documento60 pagineFIDIC Blue - Green Book - Dredging & Reclamation Works - 2006Altug100% (6)

- RJR Nabisco ValuationDocumento33 pagineRJR Nabisco ValuationKrishna Chaitanya KothapalliNessuna valutazione finora

- Cyber Cafe and Back Office ServicesDocumento11 pagineCyber Cafe and Back Office Services124swadeshi0% (1)

- Nora JV Sakari AnalysisDocumento3 pagineNora JV Sakari AnalysisIrwan PriambodoNessuna valutazione finora

- KPTL Annual Report 2017 18Documento252 pagineKPTL Annual Report 2017 18Saurabh PatelNessuna valutazione finora

- 3Documento4 pagine3Rahmatullah Mardanvi100% (3)

- Heather EvansDocumento35 pagineHeather Evansmizhar7863173100% (1)

- Buyback: What Is A Buyback?Documento3 pagineBuyback: What Is A Buyback?Niño Rey LopezNessuna valutazione finora

- Public Finance-Harvey Rosen-Chapter 19Documento31 paginePublic Finance-Harvey Rosen-Chapter 19Mochammad Rizcky PramonandaNessuna valutazione finora

- Mock Exam Paper - 28 - April - 2022Documento3 pagineMock Exam Paper - 28 - April - 2022dilinhtinh04Nessuna valutazione finora

- Xylys PresentatiomDocumento10 pagineXylys PresentatiomMuhammad Ali SheikhNessuna valutazione finora

- Maintenance CapexDocumento2 pagineMaintenance CapexGaurav JainNessuna valutazione finora

- Research Report Bajaj Finance LTDDocumento8 pagineResearch Report Bajaj Finance LTDvivekNessuna valutazione finora

- Value Investors Club - WAYFAIR INC (W)Documento4 pagineValue Investors Club - WAYFAIR INC (W)Jorge VasconcelosNessuna valutazione finora

- Wa0025.Documento47 pagineWa0025.Mazen SalahNessuna valutazione finora

- Vivo ProjectDocumento53 pagineVivo ProjectAashish Goyal100% (4)

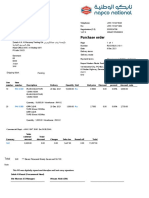

- Purchase Order: Napco Modern Plastic Products Co. - Sack DivisionDocumento1 paginaPurchase Order: Napco Modern Plastic Products Co. - Sack Divisionمحمد اصدNessuna valutazione finora

- Indian Weekender Vol 6 Issue 03Documento40 pagineIndian Weekender Vol 6 Issue 03Indian WeekenderNessuna valutazione finora

- Defaulting Rules in Purchase Orders and AgreementsDocumento27 pagineDefaulting Rules in Purchase Orders and AgreementsPavan GillellaNessuna valutazione finora

- The Proforma InvoiceDocumento8 pagineThe Proforma InvoiceAmit AgrawalNessuna valutazione finora

- Lesson PlansDocumento5 pagineLesson Plansapi-313507031Nessuna valutazione finora

- Problem Set CouponDocumento2 pagineProblem Set CouponClaudia ChoiNessuna valutazione finora

- Assignment On Ratio Analysis of Singer BangladeshDocumento17 pagineAssignment On Ratio Analysis of Singer BangladeshSISohelJnu100% (2)

- How To Do Laundry in HatyaiDocumento12 pagineHow To Do Laundry in HatyaiJoy InsaunNessuna valutazione finora

- Seminar-1 5Documento5 pagineSeminar-1 5Hoà NguyễnNessuna valutazione finora

- Incomplete SentencesDocumento103 pagineIncomplete Sentences0123405137067% (3)

- A Dictionary of Environmental EconomicsDocumento417 pagineA Dictionary of Environmental Economics279259100% (2)

- ADF Foods Limited - Report - 17th June 2008 - DhananjayanDocumento2 pagineADF Foods Limited - Report - 17th June 2008 - Dhananjayanapi-3702531Nessuna valutazione finora

- Title FormDocumento2 pagineTitle FormHamza MinhasNessuna valutazione finora