Potrebbero piacerti anche

- Bank Guarantees in International TradeDocumento4 pagineBank Guarantees in International TradeMohammad Shahjahan SiddiquiNessuna valutazione finora

- Bank Guarantee (Law Project)Documento4 pagineBank Guarantee (Law Project)starifNessuna valutazione finora

- CHAPTER VII - Bank GuaranteesDocumento12 pagineCHAPTER VII - Bank Guaranteespriya guptaNessuna valutazione finora

- SBLC & Advance Performance Guarantee (Apg)Documento11 pagineSBLC & Advance Performance Guarantee (Apg)Jasvinder Kaur100% (1)

- External Commercial BorrowingDocumento14 pagineExternal Commercial BorrowingKK SinghNessuna valutazione finora

- Compiled Digests Letters of CreditDocumento9 pagineCompiled Digests Letters of CreditAnonymous XvwKtnSrMRNessuna valutazione finora

- URDG 758 Force Majeure RuleDocumento4 pagineURDG 758 Force Majeure RulemamunabNessuna valutazione finora

- Letter of CreditDocumento6 pagineLetter of Creditpiya1234567Nessuna valutazione finora

- Bank GuaranteeDocumento1 paginaBank GuaranteeMuralikrishna SingamaneniNessuna valutazione finora

- Ucpdc 600 - Explanation On Various Articles - Part IDocumento9 pagineUcpdc 600 - Explanation On Various Articles - Part IChinnu AnchuriNessuna valutazione finora

- Trade Finance - Week 7-2Documento15 pagineTrade Finance - Week 7-2subash1111@gmail.comNessuna valutazione finora

- LC & Standby LCDocumento8 pagineLC & Standby LCmanith_kim13Nessuna valutazione finora

- Request Letter For Bank Guarantee-1st May 2018Documento1 paginaRequest Letter For Bank Guarantee-1st May 2018Karan AgrawalNessuna valutazione finora

- ICCDocumento4 pagineICCসুমন শাহরিয়ারNessuna valutazione finora

- Ucp600 English VersionDocumento23 pagineUcp600 English VersionDavid Hawkins0% (1)

- Shipping GuaranteesDocumento3 pagineShipping GuaranteesPadmanabhan RangarajanNessuna valutazione finora

- Model Bank Guarantee Format100 RsDocumento3 pagineModel Bank Guarantee Format100 RsDammudNessuna valutazione finora

- Commission On Banking Technique and PracticeDocumento37 pagineCommission On Banking Technique and Practicepiash246Nessuna valutazione finora

- Understanding The Ucp600Documento8 pagineUnderstanding The Ucp600mhussein2006100% (1)

- Standby Letter of CreditDocumento1 paginaStandby Letter of Creditheenasaluja89Nessuna valutazione finora

- Bank Guarantees and Trade FinanceDocumento14 pagineBank Guarantees and Trade Finance1221Nessuna valutazione finora

- World Bank General Conditions For LoansDocumento32 pagineWorld Bank General Conditions For LoansMax AzulNessuna valutazione finora

- Coral - Commitment LetterDocumento283 pagineCoral - Commitment LetterMarius AngaraNessuna valutazione finora

- Types of L/CDocumento127 pagineTypes of L/CSudershan ThaibaNessuna valutazione finora

- Form of Demand Guarantee Under URDG 758Documento3 pagineForm of Demand Guarantee Under URDG 758latifzahidNessuna valutazione finora

- ISP 98 Documentary and Standby Letters of CreditDocumento10 pagineISP 98 Documentary and Standby Letters of CreditengulfanddevourNessuna valutazione finora

- ArticleonLetterofCredit Part-IIDocumento3 pagineArticleonLetterofCredit Part-IIessakiNessuna valutazione finora

- 16-Contingent Liability - Schedule-12Documento62 pagine16-Contingent Liability - Schedule-12SudhansuSekharNessuna valutazione finora

- Bank of Uganda Releases Agent Banking RegulationsDocumento2 pagineBank of Uganda Releases Agent Banking RegulationspokechoNessuna valutazione finora

- Non Documentary ConditionsDocumento8 pagineNon Documentary ConditionsRami Al-SabriNessuna valutazione finora

- Isbp 745Documento57 pagineIsbp 745Nguyen Le Hong NhungNessuna valutazione finora

- Step by Step Process of Letter of CreditDocumento1 paginaStep by Step Process of Letter of CreditDhoni KhanNessuna valutazione finora

- Does UCP 600 Allow Discounting or Prepayment Under Deferred PaymentDocumento6 pagineDoes UCP 600 Allow Discounting or Prepayment Under Deferred PaymentchaudhrygiNessuna valutazione finora

- Urr 725Documento11 pagineUrr 725sayed126Nessuna valutazione finora

- Ias 37 PDFDocumento27 pagineIas 37 PDFmohedNessuna valutazione finora

- Bank Al Habib Car FinanceDocumento9 pagineBank Al Habib Car Financefatima rahimNessuna valutazione finora

- Documentary CreditDocumento15 pagineDocumentary CreditArmantoCepongNessuna valutazione finora

- Article 7 UCP 600Documento4 pagineArticle 7 UCP 600Jhoo AngelNessuna valutazione finora

- Bank GuaranteeDocumento7 pagineBank GuaranteeharshvarmaNessuna valutazione finora

- PPPs HYIP Explained.Documento18 paginePPPs HYIP Explained.FjbatisNessuna valutazione finora

- LC Docs ChecklistDocumento1 paginaLC Docs ChecklistkevindsizaNessuna valutazione finora

- Urdg 758 - WebnoteDocumento2 pagineUrdg 758 - Webnoteagung_wNessuna valutazione finora

- DAIBB MA Math Solutions 290315Documento11 pagineDAIBB MA Math Solutions 290315joyNessuna valutazione finora

- LC TerminologiesDocumento4 pagineLC Terminologiesapi-3802032100% (5)

- Icc Users Handbook For Documentary Credits Under Ucp 600Documento10 pagineIcc Users Handbook For Documentary Credits Under Ucp 600AARTICKNessuna valutazione finora

- Financial GuaranteeDocumento2 pagineFinancial Guaranteejeet_singh_deepNessuna valutazione finora

- Standby Letters of Credit: Trying To Make Your Life and Your (Documentary) Payments A Little EasierDocumento16 pagineStandby Letters of Credit: Trying To Make Your Life and Your (Documentary) Payments A Little Easiersomeonestupid1969Nessuna valutazione finora

- Guarantee ApplicationDocumento2 pagineGuarantee ApplicationAuila Rachim LubisNessuna valutazione finora

- LoansDocumento17 pagineLoansPia Samantha DasecoNessuna valutazione finora

- Bank GuaranteeDocumento3 pagineBank GuaranteeBidhan AcharyaNessuna valutazione finora

- Trade Faq Eng PDFDocumento38 pagineTrade Faq Eng PDFrubhakarNessuna valutazione finora

- European Union: What Is A 'Free Carrier - FCA'Documento11 pagineEuropean Union: What Is A 'Free Carrier - FCA'Aratrika ChoudhuriNessuna valutazione finora

- Bank Guarantee ProcedureDocumento1 paginaBank Guarantee ProcedureLatiff IbrahimNessuna valutazione finora

- Draft Version - Article On Cross Collateralization-C1Documento6 pagineDraft Version - Article On Cross Collateralization-C1Rohit Anand DasNessuna valutazione finora

- A - Bondholders Under IBC - Unravelling No Action Clauses - 01 PDFDocumento6 pagineA - Bondholders Under IBC - Unravelling No Action Clauses - 01 PDFmaulikNessuna valutazione finora

- Bank Guarantee (Defination)Documento15 pagineBank Guarantee (Defination)M Nagesh0% (1)

- Bank GuaranteesDocumento12 pagineBank Guaranteesmuhammadazmatullah100% (2)

- Law of Bank Guarantees ProjectDocumento8 pagineLaw of Bank Guarantees ProjectTushar PNessuna valutazione finora

- 14 - Adara Zalikha Setiawan - 1906423845 - Tugas Ke 7Documento5 pagine14 - Adara Zalikha Setiawan - 1906423845 - Tugas Ke 7Adara ZalikhaNessuna valutazione finora

- Company Travel Policy TemplateDocumento15 pagineCompany Travel Policy TemplateChaitanya SharmaNessuna valutazione finora

- Aptel NoteDocumento3 pagineAptel NoteChaitanya SharmaNessuna valutazione finora

- Judicial RulingDocumento12 pagineJudicial RulingChaitanya SharmaNessuna valutazione finora

- Morgan Stanley Mutual Fund Vs Kartrik DasDocumento15 pagineMorgan Stanley Mutual Fund Vs Kartrik DasChaitanya Sharma100% (1)

- Cyber Hacking in India Via Social Media: Submitted byDocumento23 pagineCyber Hacking in India Via Social Media: Submitted byChaitanya SharmaNessuna valutazione finora

- Ved KumariDocumento16 pagineVed KumariLathashree VenkatNessuna valutazione finora

- Morgan Stanley Mutual Fund V Kartick Das 1994 SCW 2801Documento12 pagineMorgan Stanley Mutual Fund V Kartick Das 1994 SCW 2801Chaitanya SharmaNessuna valutazione finora

- Criminal Conspiracy PDFDocumento10 pagineCriminal Conspiracy PDFChaitanya Sharma100% (1)

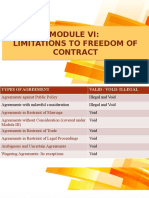

- Module VI - Limitations As To Freedom of ContractDocumento55 pagineModule VI - Limitations As To Freedom of ContractAadhitya NarayananNessuna valutazione finora

- Cases Under ContractsDocumento15 pagineCases Under ContractsPriyankaNessuna valutazione finora

- Rights and Obligation of The VendorDocumento4 pagineRights and Obligation of The VendorFaye Cience BoholNessuna valutazione finora

- Illegality: English Law: Holman V Johnson (1775) 1 Cowp 341Documento43 pagineIllegality: English Law: Holman V Johnson (1775) 1 Cowp 341承艳Nessuna valutazione finora

- Article 1196Documento17 pagineArticle 1196Christlyn Joy BaralNessuna valutazione finora

- Clarificatory Note No. 18-001 Subject: Consolidation of OwnershipDocumento6 pagineClarificatory Note No. 18-001 Subject: Consolidation of OwnershipReginald Matt Aquino SantiagoNessuna valutazione finora

- Binaya Kumar Parida EMBA-2020-21, 1 Semester Business and Corporate Laws Assignment Roll No-16Documento7 pagineBinaya Kumar Parida EMBA-2020-21, 1 Semester Business and Corporate Laws Assignment Roll No-16binay kumar ParidaNessuna valutazione finora

- Indian Contract Act 1872, With Sections & Illustrations: (Section 1) - Title, Commencement & ScopeDocumento32 pagineIndian Contract Act 1872, With Sections & Illustrations: (Section 1) - Title, Commencement & ScopeAshish KumarNessuna valutazione finora

- Insurance Commission Reviewer Set ADocumento9 pagineInsurance Commission Reviewer Set AMelissa CaagNessuna valutazione finora

- Memorandum of AgreementDocumento2 pagineMemorandum of AgreementMarcelino SanicoNessuna valutazione finora

- Area: Counting Unit Squares: Directions: Find The Area of The Shape by Counting The Square UnitsDocumento2 pagineArea: Counting Unit Squares: Directions: Find The Area of The Shape by Counting The Square UnitsAileen MimeryNessuna valutazione finora

- Solution Manual For Valuation 2nd Edition by TitmanDocumento24 pagineSolution Manual For Valuation 2nd Edition by TitmanDanaPalmerygfb100% (41)

- FC BG SBLC Loi 41+2%Documento28 pagineFC BG SBLC Loi 41+2%Lee Si HuiNessuna valutazione finora

- Problem SolutionsDocumento4 pagineProblem SolutionsParas JangirNessuna valutazione finora

- Partnership - Principles of AccountingDocumento9 paginePartnership - Principles of AccountingAbdulla MaseehNessuna valutazione finora

- Exercises in CM7 FinalsDocumento2 pagineExercises in CM7 FinalsCyril JeanneNessuna valutazione finora

- .LArrobis vs. Veterans BankDocumento5 pagine.LArrobis vs. Veterans BankAimie Razul-AparecioNessuna valutazione finora

- The Offer Must Be Capable of Creating Legal RelationshipDocumento6 pagineThe Offer Must Be Capable of Creating Legal RelationshipTrupti GowdaNessuna valutazione finora

- (Action Required) Google Assignment OnboardinDocumento4 pagine(Action Required) Google Assignment OnboardinFranco LeveraNessuna valutazione finora

- I'll Be There For YouDocumento8 pagineI'll Be There For YouPonto do Sabor Salgados e QuitandasNessuna valutazione finora

- Law of ContractDocumento3 pagineLaw of ContractSteve OutstandingNessuna valutazione finora

- Memorandum of Understanding - IPleadersDocumento36 pagineMemorandum of Understanding - IPleadersAbhik SahaNessuna valutazione finora

- Set-Off in International Economic Arbitration: by Klaus Peter BergerDocumento32 pagineSet-Off in International Economic Arbitration: by Klaus Peter BergerIkram Mahar100% (1)

- Accounting For Special TransactionsDocumento11 pagineAccounting For Special Transactionsjohn carloNessuna valutazione finora

- FANTASTIC5 - BA 1194 E - Assignment1Documento5 pagineFANTASTIC5 - BA 1194 E - Assignment1NURADILAH AHMAD SHAIFUDDINNessuna valutazione finora

- Three Payment Plan Plus-1Documento4 pagineThree Payment Plan Plus-1tapas1361Nessuna valutazione finora

- LicensesDocumento4 pagineLicensesFernando GarciaNessuna valutazione finora

- Explain The Nature of Fiduciary Duties Owned by A DirectorDocumento2 pagineExplain The Nature of Fiduciary Duties Owned by A DirectorJaydeep KushwahaNessuna valutazione finora

- Format of Pre Bid JV AgreementDocumento4 pagineFormat of Pre Bid JV Agreementsrasheed100% (1)

- Bona Fide Suspension of OperationsDocumento8 pagineBona Fide Suspension of OperationsGab NaparatoNessuna valutazione finora

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationDa EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationValutazione: 4 su 5 stelle4/5 (11)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassDa EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNessuna valutazione finora

- Narrative Economics: How Stories Go Viral and Drive Major Economic EventsDa EverandNarrative Economics: How Stories Go Viral and Drive Major Economic EventsValutazione: 4.5 su 5 stelle4.5/5 (94)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingDa EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingValutazione: 4.5 su 5 stelle4.5/5 (97)

- Principles for Dealing with the Changing World Order: Why Nations Succeed or FailDa EverandPrinciples for Dealing with the Changing World Order: Why Nations Succeed or FailValutazione: 4.5 su 5 stelle4.5/5 (237)

- The Meth Lunches: Food and Longing in an American CityDa EverandThe Meth Lunches: Food and Longing in an American CityValutazione: 5 su 5 stelle5/5 (5)

- Chip War: The Quest to Dominate the World's Most Critical TechnologyDa EverandChip War: The Quest to Dominate the World's Most Critical TechnologyValutazione: 4.5 su 5 stelle4.5/5 (228)

- Look Again: The Power of Noticing What Was Always ThereDa EverandLook Again: The Power of Noticing What Was Always ThereValutazione: 5 su 5 stelle5/5 (3)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesDa EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesValutazione: 4.5 su 5 stelle4.5/5 (8)

- The Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaDa EverandThe Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaNessuna valutazione finora

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumDa EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumValutazione: 3 su 5 stelle3/5 (12)

- This Changes Everything: Capitalism vs. The ClimateDa EverandThis Changes Everything: Capitalism vs. The ClimateValutazione: 4 su 5 stelle4/5 (349)

- Economics 101: How the World WorksDa EverandEconomics 101: How the World WorksValutazione: 4.5 su 5 stelle4.5/5 (34)

- Vienna: How the City of Ideas Created the Modern WorldDa EverandVienna: How the City of Ideas Created the Modern WorldNessuna valutazione finora

- How an Economy Grows and Why It Crashes: Collector's EditionDa EverandHow an Economy Grows and Why It Crashes: Collector's EditionValutazione: 4.5 su 5 stelle4.5/5 (102)

- Economics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsDa EverandEconomics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsValutazione: 5 su 5 stelle5/5 (3)

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetDa EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetNessuna valutazione finora

- Doughnut Economics: Seven Ways to Think Like a 21st-Century EconomistDa EverandDoughnut Economics: Seven Ways to Think Like a 21st-Century EconomistValutazione: 4.5 su 5 stelle4.5/5 (37)

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationDa EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationValutazione: 4.5 su 5 stelle4.5/5 (46)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDa EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaValutazione: 4.5 su 5 stelle4.5/5 (14)

- The New Elite: Inside the Minds of the Truly WealthyDa EverandThe New Elite: Inside the Minds of the Truly WealthyValutazione: 4 su 5 stelle4/5 (10)

- Second Class: How the Elites Betrayed America's Working Men and WomenDa EverandSecond Class: How the Elites Betrayed America's Working Men and WomenNessuna valutazione finora