Potrebbero piacerti anche

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsDa EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNessuna valutazione finora

- Advanced Analysis and Appraisal of PerformanceDocumento7 pagineAdvanced Analysis and Appraisal of PerformanceAnn SalazarNessuna valutazione finora

- Return On InvestmentDocumento5 pagineReturn On Investmentela kikay100% (1)

- M3 Activity 1Documento6 pagineM3 Activity 1Ruffa May GonzalesNessuna valutazione finora

- Corporate Finance 3rd Edition Graham Solution ManualDocumento15 pagineCorporate Finance 3rd Edition Graham Solution ManualMark PanchitoNessuna valutazione finora

- MCI 01 Management ReviewDocumento3 pagineMCI 01 Management ReviewalexrferreiraNessuna valutazione finora

- Answer KeyDocumento19 pagineAnswer KeyRenNessuna valutazione finora

- Performance-Evaluation-and-Decentralization W - Answers PDFDocumento8 paginePerformance-Evaluation-and-Decentralization W - Answers PDFTh VNessuna valutazione finora

- Wokrplace Safety Bizsafe Audit Preparation Special ReportDocumento8 pagineWokrplace Safety Bizsafe Audit Preparation Special Reportisaych33zeNessuna valutazione finora

- Lecture 27Documento34 pagineLecture 27Riaz Baloch NotezaiNessuna valutazione finora

- Distributor Sales Force Performance ManagementDocumento15 pagineDistributor Sales Force Performance ManagementTomy Utomo75% (4)

- EVP Case StudyDocumento11 pagineEVP Case StudyMayuri Joshi DhavaleNessuna valutazione finora

- 13 Roi, Ri, EvaDocumento32 pagine13 Roi, Ri, EvaANSuciZahra100% (1)

- BASTRCSX Module 6 Self-Test Responsibility Accounting Part 2Documento8 pagineBASTRCSX Module 6 Self-Test Responsibility Accounting Part 2Alyssa CaddawanNessuna valutazione finora

- Performance MGMT Discussion QuestionsDocumento7 paginePerformance MGMT Discussion QuestionsSritel Boutique HotelNessuna valutazione finora

- Responsibility Accounting and Transfer PricingDocumento26 pagineResponsibility Accounting and Transfer PricingfoglaabhishekNessuna valutazione finora

- Solution Manual For Financial Management Theory and Practice Third Canadian EditionDocumento36 pagineSolution Manual For Financial Management Theory and Practice Third Canadian Editionejecthalibutudoh0100% (31)

- Responsibility AccountingDocumento10 pagineResponsibility AccountingCheny MabiniNessuna valutazione finora

- Akmen Chapter 12 (Putri Ramadhani)Documento22 pagineAkmen Chapter 12 (Putri Ramadhani)Putri RamadhaniNessuna valutazione finora

- Raport Anual Accor HotelDocumento404 pagineRaport Anual Accor HotelIsrati Valeriu100% (3)

- 8a. Responsibility and Segment Accounting CRDocumento20 pagine8a. Responsibility and Segment Accounting CRAngelica Gaspay EstalillaNessuna valutazione finora

- GroupeAriel S.ADocumento3 pagineGroupeAriel S.AEina GuptaNessuna valutazione finora

- Akmen CH 12 KelarDocumento19 pagineAkmen CH 12 KelarFadhliyaFNessuna valutazione finora

- Seminar in Management AccountingDocumento6 pagineSeminar in Management AccountinglolaNessuna valutazione finora

- Segment Reporting, Decentralization and The Balanced ScorecardDocumento20 pagineSegment Reporting, Decentralization and The Balanced ScorecardSneha SureshNessuna valutazione finora

- 2008 Acct 212 Chapter 10 Resp Accg NotesDocumento6 pagine2008 Acct 212 Chapter 10 Resp Accg NotesBrandon HookerNessuna valutazione finora

- EXERCISE 12-2 (15 Minutes)Documento9 pagineEXERCISE 12-2 (15 Minutes)Mari Louis Noriell MejiaNessuna valutazione finora

- ShitDocumento6 pagineShitgejayan memanggilNessuna valutazione finora

- Responsibility and Segment Accounting CRDocumento24 pagineResponsibility and Segment Accounting CRAshy LeeNessuna valutazione finora

- Problem1 - The Following Data Are From The Giant Oreo Division at Keebler CookiesDocumento29 pagineProblem1 - The Following Data Are From The Giant Oreo Division at Keebler CookiesFerl ElardoNessuna valutazione finora

- Full Download Solutions Manual To Accompany Construction Accounting Financial Management 2nd Edition 9780135017111 PDF Full ChapterDocumento36 pagineFull Download Solutions Manual To Accompany Construction Accounting Financial Management 2nd Edition 9780135017111 PDF Full Chapterurocelespinningnuyu100% (20)

- Solutions Manual To Accompany Construction Accounting Financial Management 2nd Edition 9780135017111Documento36 pagineSolutions Manual To Accompany Construction Accounting Financial Management 2nd Edition 9780135017111epha.thialol.lqoc100% (50)

- Corporate FinanceDocumento9 pagineCorporate FinancePrince HussainNessuna valutazione finora

- AMA Lecture 2Documento54 pagineAMA Lecture 2Mohammed FouadNessuna valutazione finora

- Tugas AulaDocumento5 pagineTugas AulaZuriafNessuna valutazione finora

- ACC702 - Week 7 Tutorial SOLUTIONS CH 13 ROI EVADocumento6 pagineACC702 - Week 7 Tutorial SOLUTIONS CH 13 ROI EVAankit dhimanNessuna valutazione finora

- CASE 5-33 Solution: Nabeeda ShaheenDocumento4 pagineCASE 5-33 Solution: Nabeeda ShaheenhadiNessuna valutazione finora

- Performance Measurement in Decentralized Organizations: ERLINDA SACHARISSA (201850021) CINDY (201850046)Documento37 paginePerformance Measurement in Decentralized Organizations: ERLINDA SACHARISSA (201850021) CINDY (201850046)cindy chandraNessuna valutazione finora

- Investment Centers and Transfer PricingDocumento53 pagineInvestment Centers and Transfer PricingArlene DacpanoNessuna valutazione finora

- Soal Latihan Pertemuan KelimaDocumento7 pagineSoal Latihan Pertemuan KelimaErvian RidhoNessuna valutazione finora

- Performance Mesurement of OrganizationDocumento10 paginePerformance Mesurement of OrganizationbbasNessuna valutazione finora

- 5684 SampleDocumento1 pagina5684 SampleChessking Siew HeeNessuna valutazione finora

- Solution Manual For Cfin 5Th Edition by Besley and Brigham Isbn 1305661656 9781305661653 Full Chapter PDFDocumento36 pagineSolution Manual For Cfin 5Th Edition by Besley and Brigham Isbn 1305661656 9781305661653 Full Chapter PDFtiffany.kunst387100% (9)

- 317 Midterm 1 Practice Exam SolutionsDocumento9 pagine317 Midterm 1 Practice Exam Solutionskinyuadavid000Nessuna valutazione finora

- Dwnload Full Cfin 5th Edition Besley Solutions Manual PDFDocumento35 pagineDwnload Full Cfin 5th Edition Besley Solutions Manual PDFandrefloresxudd100% (11)

- Cfin 5th Edition Besley Solutions ManualDocumento35 pagineCfin 5th Edition Besley Solutions Manualghebre.comatula.75ew100% (28)

- Acc 223a - Answers To CH 15 AssignmentDocumento7 pagineAcc 223a - Answers To CH 15 AssignmentAna Leah DelfinNessuna valutazione finora

- GainersDocumento17 pagineGainersborn2grow100% (1)

- Afm AssignmentDocumento17 pagineAfm AssignmentHabtamuNessuna valutazione finora

- Quiz 6 NotesDocumento14 pagineQuiz 6 NotesEmily SNessuna valutazione finora

- Dwnload Full Cfin 4 4th Edition Besley Solutions Manual PDFDocumento35 pagineDwnload Full Cfin 4 4th Edition Besley Solutions Manual PDFbrandihansenjoqll2100% (13)

- Cfin 4 4th Edition Besley Solutions ManualDocumento35 pagineCfin 4 4th Edition Besley Solutions Manualghebre.comatula.75ew100% (22)

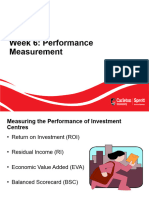

- Week 6 Performance MeasurementDocumento56 pagineWeek 6 Performance MeasurementMichel BanvoNessuna valutazione finora

- Exercise 1Documento4 pagineExercise 1Nyster Ann RebenitoNessuna valutazione finora

- PacificDocumento3 paginePacificThanh SangNessuna valutazione finora

- Reviewer MactwoDocumento17 pagineReviewer MactwoJessa Iloso PerezNessuna valutazione finora

- Revenue (Sales) XXX (-) Variable Costs XXXDocumento10 pagineRevenue (Sales) XXX (-) Variable Costs XXXNageshwar SinghNessuna valutazione finora

- PREP COF Sample Exam QuestionsDocumento10 paginePREP COF Sample Exam QuestionsLNessuna valutazione finora

- Management Accounting: Segment Reporting & DecentralizationDocumento20 pagineManagement Accounting: Segment Reporting & DecentralizationSamiul AzamNessuna valutazione finora

- CH09Documento62 pagineCH09Lê Chấn PhongNessuna valutazione finora

- 601 13,14 SolutionsDocumento37 pagine601 13,14 SolutionsRudi SyafputraNessuna valutazione finora

- Lecture 28Documento34 pagineLecture 28Riaz Baloch NotezaiNessuna valutazione finora

- Responsibilty AccountingDocumento3 pagineResponsibilty AccountingRenu PoddarNessuna valutazione finora

- Acct 3503 Test 2 Format, Instuctions and Review Section A FridayDocumento22 pagineAcct 3503 Test 2 Format, Instuctions and Review Section A Fridayyahye ahmedNessuna valutazione finora

- PERMALINO - Learning Activity 19. Working Capital ManagementDocumento3 paginePERMALINO - Learning Activity 19. Working Capital ManagementAra Joyce PermalinoNessuna valutazione finora

- Explain The Role of The Financial System and Why It Is ImportantDocumento1 paginaExplain The Role of The Financial System and Why It Is ImportantMangala PrasetiaNessuna valutazione finora

- Mylab2: Jason Qin, Lulu Jin, Thanh Thai Nguyen, Chairach Kraiisarin 5 August 2016 Jqin17, Ljin47, Tngu251, Ckra4Documento4 pagineMylab2: Jason Qin, Lulu Jin, Thanh Thai Nguyen, Chairach Kraiisarin 5 August 2016 Jqin17, Ljin47, Tngu251, Ckra4Mangala PrasetiaNessuna valutazione finora

- MYLab 3Documento4 pagineMYLab 3Mangala PrasetiaNessuna valutazione finora

- Semester 2 2016 Week 1 Tutorial Solutions PDFDocumento7 pagineSemester 2 2016 Week 1 Tutorial Solutions PDFMangala PrasetiaNessuna valutazione finora

- Introduction To Industrial Relations - Chapter IDocumento9 pagineIntroduction To Industrial Relations - Chapter IKamal KatariaNessuna valutazione finora

- 1060-2022 PO ATL M.S Bismillah AccessoriesDocumento1 pagina1060-2022 PO ATL M.S Bismillah AccessoriesYounus SheikhNessuna valutazione finora

- CMS Introduction To Measures ManagementDocumento27 pagineCMS Introduction To Measures ManagementiggybauNessuna valutazione finora

- PEL PakistanDocumento27 paginePEL Pakistanjutt707100% (1)

- Doors Offer Il BagnoDocumento1 paginaDoors Offer Il Bagnosellitt ngNessuna valutazione finora

- What You Should Know About The Cap RateDocumento4 pagineWhat You Should Know About The Cap RateJacob YangNessuna valutazione finora

- PESTEL Analysis of Hindustan Unilever HUL PDFDocumento4 paginePESTEL Analysis of Hindustan Unilever HUL PDFparulNessuna valutazione finora

- Chapter 4 - Part 1Documento14 pagineChapter 4 - Part 1billtanNessuna valutazione finora

- The Systems Development Environment: True-False QuestionsDocumento262 pagineThe Systems Development Environment: True-False Questionslouisa_wanNessuna valutazione finora

- Part A / Bahagian A Instruction / Arahan: BBAP2103 (SAMPLE 1)Documento10 paginePart A / Bahagian A Instruction / Arahan: BBAP2103 (SAMPLE 1)Faidz FuadNessuna valutazione finora

- Virgin Trains Case StudyDocumento5 pagineVirgin Trains Case StudyPage MirerzNessuna valutazione finora

- 2023 BusinessKids Convention ReportDocumento18 pagine2023 BusinessKids Convention ReportClaudia Isabel MirelesNessuna valutazione finora

- Product Management Maturity Model: Tools LeadershipDocumento1 paginaProduct Management Maturity Model: Tools LeadershipAlexandre NascimentoNessuna valutazione finora

- Jcpenney Analysis: Background StoryDocumento13 pagineJcpenney Analysis: Background StoryAakarshan MundraNessuna valutazione finora

- Ifrs Us Gaap Ind As and Indian Gaap Similarities and DifferencesDocumento4 pagineIfrs Us Gaap Ind As and Indian Gaap Similarities and DifferencesDrpranav SaraswatNessuna valutazione finora

- A. Find The Values of The Missing Variables, Which Are Defined As FollowsDocumento3 pagineA. Find The Values of The Missing Variables, Which Are Defined As FollowsHermione Eyer - TanNessuna valutazione finora

- Foreign Exchange Management - An Overview of Current Account TransactionsDocumento50 pagineForeign Exchange Management - An Overview of Current Account Transactionsrebalap15Nessuna valutazione finora

- Collaboration Business Plan TemplateDocumento18 pagineCollaboration Business Plan TemplateThu A. PhamNessuna valutazione finora

- Chap01 Tutorial QuestionsDocumento3 pagineChap01 Tutorial QuestionsThắng Nguyễn HuyNessuna valutazione finora

- C1H021021 - Almas Delian - Resume MIS Bab 1Documento2 pagineC1H021021 - Almas Delian - Resume MIS Bab 1Almas DelianNessuna valutazione finora

- SM Prime Holdings, Inc. - Sec Form 17-A-2020Documento265 pagineSM Prime Holdings, Inc. - Sec Form 17-A-2020Lorraine AlboNessuna valutazione finora

- Accounting Cycle StepsDocumento4 pagineAccounting Cycle StepsAntiiasmawatiiNessuna valutazione finora

- Rapport Annuel Awb - Vangl PDFDocumento86 pagineRapport Annuel Awb - Vangl PDFcasaNessuna valutazione finora

- PT KaoDocumento9 paginePT KaoVincent OwenNessuna valutazione finora