Potrebbero piacerti anche

- Ifrs at A Glance: IAS 39 Financial InstrumentsDocumento8 pagineIfrs at A Glance: IAS 39 Financial InstrumentsvivekchokshiNessuna valutazione finora

- TAX-502 (Excise Tax Rates - Part 2)Documento3 pagineTAX-502 (Excise Tax Rates - Part 2)Princess ManaloNessuna valutazione finora

- Process Cost Accounting Additional Procedures: Accounting For Joint Products and By-ProductsDocumento23 pagineProcess Cost Accounting Additional Procedures: Accounting For Joint Products and By-ProductsMudassar HassanNessuna valutazione finora

- Investment Property: By:-Yohannes Negatu (Acca, DipifrDocumento31 pagineInvestment Property: By:-Yohannes Negatu (Acca, DipifrEshetie Mekonene AmareNessuna valutazione finora

- Philippine Standard On AuditingDocumento19 paginePhilippine Standard On AuditingHavanaNessuna valutazione finora

- Pas 32Documento34 paginePas 32Iris SarigumbaNessuna valutazione finora

- Share-Based Compensation: Learning ObjectivesDocumento48 pagineShare-Based Compensation: Learning ObjectivesJola MairaloNessuna valutazione finora

- Module1 - Foreign Currency Transaction and TranslationDocumento3 pagineModule1 - Foreign Currency Transaction and TranslationGerome Echano0% (1)

- Pfrs 16 LeasesDocumento4 paginePfrs 16 LeasesR.A.Nessuna valutazione finora

- Ias 24 Related Party Disclosure PDFDocumento5 pagineIas 24 Related Party Disclosure PDFsimply PrettyNessuna valutazione finora

- Valuation of SharesDocumento45 pagineValuation of Shares7laxmanNessuna valutazione finora

- ASC 718 Stock-Based Compensation Student)Documento30 pagineASC 718 Stock-Based Compensation Student)scottyuNessuna valutazione finora

- Auditing Theory Review Notes (AT-3) Page 1 of 13: Industry ConditionsDocumento13 pagineAuditing Theory Review Notes (AT-3) Page 1 of 13: Industry ConditionsJane Michelle EmanNessuna valutazione finora

- Taxation of IndividualsDocumento12 pagineTaxation of Individualsaj lopezNessuna valutazione finora

- Chapter 4 DerivativesDocumento38 pagineChapter 4 DerivativesTamrat KindeNessuna valutazione finora

- Philippine Interpretations Committee (Pic) Questions and Answers (Q&As)Documento6 paginePhilippine Interpretations Committee (Pic) Questions and Answers (Q&As)Mary Jo Lariz OcliasoNessuna valutazione finora

- Pfrs 7 Financial Instruments DisclosuresDocumento3 paginePfrs 7 Financial Instruments DisclosuresR.A.Nessuna valutazione finora

- PSA220 Quality Management For An Audit of Financial StatementsDocumento45 paginePSA220 Quality Management For An Audit of Financial StatementsKrizel rochaNessuna valutazione finora

- Accrual Vs Cash AccountingDocumento13 pagineAccrual Vs Cash AccountingNurul Baiyah100% (1)

- Presentation On Operational AuditDocumento57 paginePresentation On Operational AuditctcamatNessuna valutazione finora

- Accounting For Partnership OperationDocumento26 pagineAccounting For Partnership OperationJOANNA ROSE MANALONessuna valutazione finora

- Chapter 4Documento30 pagineChapter 4Siti AishahNessuna valutazione finora

- Auditing: Module 4 Forming An Opinion and Reporting On Financial StatementsDocumento48 pagineAuditing: Module 4 Forming An Opinion and Reporting On Financial StatementsJohn Archie AntonioNessuna valutazione finora

- Cfas ReviewerDocumento6 pagineCfas ReviewerMaycacayan, Charlene M.Nessuna valutazione finora

- Module 12 - Audit ReportingDocumento10 pagineModule 12 - Audit ReportingRufina B VerdeNessuna valutazione finora

- Hand OutDocumento8 pagineHand OutziahnepostreliNessuna valutazione finora

- At TestbankDocumento5 pagineAt TestbankMartinez JomarNessuna valutazione finora

- Chapter On CVP 2015 - Acc 2Documento16 pagineChapter On CVP 2015 - Acc 2nur aqilah ridzuanNessuna valutazione finora

- Throughput Accounting F5 NotesDocumento7 pagineThroughput Accounting F5 NotesSiddiqua KashifNessuna valutazione finora

- Toa - 2011Documento7 pagineToa - 2011EugeneDumalagNessuna valutazione finora

- Espineli - Isa 210Documento18 pagineEspineli - Isa 210Ghelo Meruena EspineliNessuna valutazione finora

- IFRS 4 Insurance Contracts Phase II: Preparing For ActionDocumento53 pagineIFRS 4 Insurance Contracts Phase II: Preparing For Actionsai madhavNessuna valutazione finora

- Afar MCQ PracticeDocumento79 pagineAfar MCQ PracticeAlysa dawn CabrestanteNessuna valutazione finora

- Lease 12 AprilDocumento32 pagineLease 12 Aprilr4vemaster100% (1)

- IAS 21 - Effects of Changes in Foreign Exchange PDFDocumento22 pagineIAS 21 - Effects of Changes in Foreign Exchange PDFJanelle SentinaNessuna valutazione finora

- Fund, Which Is Separate From The Reporting Entity For The Purpose ofDocumento7 pagineFund, Which Is Separate From The Reporting Entity For The Purpose ofNaddieNessuna valutazione finora

- FINALS - Theory of AccountsDocumento8 pagineFINALS - Theory of AccountsAngela ViernesNessuna valutazione finora

- AFAR 2305 Not-for-Profit OrganizationsDocumento14 pagineAFAR 2305 Not-for-Profit OrganizationsDzulija Talipan100% (1)

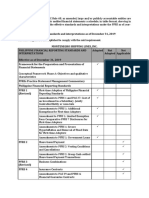

- Montenegro Tabular Schedule of Standards and Interpretations 2019Documento6 pagineMontenegro Tabular Schedule of Standards and Interpretations 2019Kathleen LeynesNessuna valutazione finora

- Chapter 2-Audits of Financial Statements PDFDocumento23 pagineChapter 2-Audits of Financial Statements PDFCaryll Joy BisnanNessuna valutazione finora

- Partnership LiquidationDocumento37 paginePartnership LiquidationDe Gala ShailynNessuna valutazione finora

- A Roadmap To Accounting For Share-Based Payment Awards - Third EditionDocumento488 pagineA Roadmap To Accounting For Share-Based Payment Awards - Third EditionBeth Bush100% (1)

- Lecture On Share Based Payments Share Appreciation RightsDocumento8 pagineLecture On Share Based Payments Share Appreciation RightsChristine AltamarinoNessuna valutazione finora

- Acetate On Corporate Governance Principles Under The Corporation CodeDocumento24 pagineAcetate On Corporate Governance Principles Under The Corporation CodeGusty Ong VañoNessuna valutazione finora

- Error Detection and CorrectionDocumento38 pagineError Detection and CorrectionKipkirui TopiasNessuna valutazione finora

- Module 9 Reports On Audited Financial StatementsDocumento53 pagineModule 9 Reports On Audited Financial StatementsDjunah ArellanoNessuna valutazione finora

- The Code of Ethics For Cpas in The Philippines: Chapter SixDocumento24 pagineThe Code of Ethics For Cpas in The Philippines: Chapter SixQueenie QuisidoNessuna valutazione finora

- At 1 Theory Palang With Questions 1Documento12 pagineAt 1 Theory Palang With Questions 1Sharmaine JoyceNessuna valutazione finora

- Toa Interim ReportingDocumento17 pagineToa Interim ReportingEmmanuel SarmientoNessuna valutazione finora

- AC2401 Assurance and Auditing BibleDocumento57 pagineAC2401 Assurance and Auditing BibleStreak CalmNessuna valutazione finora

- RR 16 2008Documento8 pagineRR 16 2008Ruby ReyesNessuna valutazione finora

- FAR 2 Finals Cheat SheetDocumento8 pagineFAR 2 Finals Cheat SheetILOVE MATURED FANSNessuna valutazione finora

- Ias 24 Related Party DisclosuresDocumento3 pagineIas 24 Related Party DisclosurescaarunjiNessuna valutazione finora

- International Financial Reporting Standards (IFRS)Documento10 pagineInternational Financial Reporting Standards (IFRS)soorajsooNessuna valutazione finora

- Factory Overhead VarianceDocumento8 pagineFactory Overhead VarianceLovely Mae LariosaNessuna valutazione finora

- Accntg4 Non-Current Assets Held For Sale and Discontinued Operations NewDocumento32 pagineAccntg4 Non-Current Assets Held For Sale and Discontinued Operations NewALYSSA MAE ABAAGNessuna valutazione finora

- Direct Tax CodeDocumento4 pagineDirect Tax CodeHardip MatholiyaNessuna valutazione finora

- The Balanced Scorecard: A Tool To Implement StrategyDocumento39 pagineThe Balanced Scorecard: A Tool To Implement StrategyAilene QuintoNessuna valutazione finora

- Sa 260Documento24 pagineSa 260Wael AshajiNessuna valutazione finora

- Isa 260Documento17 pagineIsa 260baabasaamNessuna valutazione finora

- FMD PPT For SeminarDocumento15 pagineFMD PPT For Seminarucantseeme0000Nessuna valutazione finora

- Notice Format For Madhyamik ParikshaDocumento5 pagineNotice Format For Madhyamik ParikshaSuvadip SanyalNessuna valutazione finora

- Notes PCDocumento35 pagineNotes PCSwapnil NanawareNessuna valutazione finora

- Viltam User Manual enDocumento13 pagineViltam User Manual enszol888Nessuna valutazione finora

- Photo-Realistic 3D Model Extraction From Camera Array CaptureDocumento11 paginePhoto-Realistic 3D Model Extraction From Camera Array CaptureJohn NaylorNessuna valutazione finora

- Eindhoven University of Technology: Award Date: 2008Documento65 pagineEindhoven University of Technology: Award Date: 2008Jay Mark VillarealNessuna valutazione finora

- BTP ReportDocumento27 pagineBTP ReportAayush Ghosh ChoudhuryNessuna valutazione finora

- Appendix - F2 - RAPDocumento156 pagineAppendix - F2 - RAPMecha MartiniNessuna valutazione finora

- Data Gathering Advantage and DisadvantageDocumento4 pagineData Gathering Advantage and DisadvantageJuan VeronNessuna valutazione finora

- A New Four-Scroll Chaotic System With A Self-Excited Attractor and Circuit ImplementationDocumento5 pagineA New Four-Scroll Chaotic System With A Self-Excited Attractor and Circuit ImplementationMada Sanjaya WsNessuna valutazione finora

- Kindergarten Weekly Lesson Plan TemplateDocumento2 pagineKindergarten Weekly Lesson Plan TemplateRobin Escoses MallariNessuna valutazione finora

- Habitat Lesson PlanDocumento2 pagineHabitat Lesson Planapi-177886209Nessuna valutazione finora

- Interpersonel Need of Management Student-Acilitor in The Choice of ElectivesDocumento180 pagineInterpersonel Need of Management Student-Acilitor in The Choice of ElectivesnerdjumboNessuna valutazione finora

- Therapeutic Effects of DrummingDocumento3 pagineTherapeutic Effects of DrummingMichael Drake100% (4)

- Sel KompetenDocumento12 pagineSel KompetenEnung Warsita DahlanNessuna valutazione finora

- Go Betweens For HitlerDocumento402 pagineGo Betweens For HitlerSagyan Regmi Regmi100% (1)

- Family Day by Day - The Guide To A Successful Family LifeDocumento212 pagineFamily Day by Day - The Guide To A Successful Family Lifeprajya100% (3)

- Solutions ExercisesDocumento109 pagineSolutions ExercisesDNessuna valutazione finora

- Guide SauvegardeDocumento688 pagineGuide SauvegardemitrailleNessuna valutazione finora

- TractatusDocumento185 pagineTractatusSattyaki BasuNessuna valutazione finora

- C2 - Linear ProgramingDocumento76 pagineC2 - Linear ProgramingLy LêNessuna valutazione finora

- ForensicDocumento23 pagineForensicKamya ChandokNessuna valutazione finora

- Service Manual: Digital Laser Copier/ Digital Multifunctional SystemDocumento132 pagineService Manual: Digital Laser Copier/ Digital Multifunctional SystemViktor FehlerNessuna valutazione finora

- Qlikview 10 Accesspoint SSODocumento21 pagineQlikview 10 Accesspoint SSOAlberto AlavezNessuna valutazione finora

- Disconnected ManDocumento4 pagineDisconnected ManBecky100% (1)

- Chapter 1 Introduction To Emergency Medical CareDocumento19 pagineChapter 1 Introduction To Emergency Medical Carejmmos207064100% (1)

- Eju Maths Samp PaperDocumento29 pagineEju Maths Samp PapersravanarajNessuna valutazione finora

- Toc GMP Manual Ud12Documento34 pagineToc GMP Manual Ud12navas1972100% (2)

- Vxworks Kernel Programmers Guide 6.8Documento802 pagineVxworks Kernel Programmers Guide 6.8hisahinNessuna valutazione finora