Potrebbero piacerti anche

- PUBLIC FINANCE AND TAXATION- BCOM ACC, FIN & BBADocumento13 paginePUBLIC FINANCE AND TAXATION- BCOM ACC, FIN & BBAMaster KihimbwaNessuna valutazione finora

- 15 Financial AccountsDocumento111 pagine15 Financial AccountsRenga Pandi100% (1)

- 2 Sem - Bcom - Advanced Financial AccountingDocumento39 pagine2 Sem - Bcom - Advanced Financial AccountingpradeepNessuna valutazione finora

- Accounting Basics Study Material 0Documento36 pagineAccounting Basics Study Material 0NikhilKrishnanNessuna valutazione finora

- Capital and Revenue ExpendituereDocumento30 pagineCapital and Revenue ExpendituereDheeraj Seth0% (1)

- Adjustments of Final AccountsDocumento5 pagineAdjustments of Final AccountsKashif KhanNessuna valutazione finora

- Bonus Share and Right IssueDocumento5 pagineBonus Share and Right IssueNiketa SharmaNessuna valutazione finora

- Accounting BasicsDocumento13 pagineAccounting BasicskameshpatilNessuna valutazione finora

- Advanced Accounting - Part 2 - New CourseDocumento456 pagineAdvanced Accounting - Part 2 - New Courseimayushms15Nessuna valutazione finora

- Advanced Accounting Study MaterialDocumento974 pagineAdvanced Accounting Study MaterialPrashant Sagar Gautam100% (2)

- Report On Cost AuditDocumento15 pagineReport On Cost AuditMH (Mahmudul Hasan)100% (1)

- Different Borrowers Types ExplainedDocumento15 pagineDifferent Borrowers Types Explainedmevrick_guyNessuna valutazione finora

- The Accounting Cycle FundamentalsDocumento53 pagineThe Accounting Cycle FundamentalsGonzalo Jr. Ruales100% (1)

- 22 How To Solve Difficult Adjustments and Journal Entries in Financial AccountsDocumento43 pagine22 How To Solve Difficult Adjustments and Journal Entries in Financial AccountsKushal D Kale79% (33)

- Ffp-English-Finance and Accounting Manual - v3 PDFDocumento78 pagineFfp-English-Finance and Accounting Manual - v3 PDFTin Zaw ThantNessuna valutazione finora

- Wall Street Prep's Guide to Accounting & Financial StatementsDocumento238 pagineWall Street Prep's Guide to Accounting & Financial StatementsShawn JohnsonNessuna valutazione finora

- Dissolutioni of Partnership FirmDocumento69 pagineDissolutioni of Partnership FirmbinuNessuna valutazione finora

- Ican Ican Ican Ican Ican: TaxationDocumento392 pagineIcan Ican Ican Ican Ican: Taxationhiroshika wsabiNessuna valutazione finora

- Share Valuation - 1 PDFDocumento7 pagineShare Valuation - 1 PDFbonnie.barma2831100% (1)

- Ncert 12 Account 2Documento329 pagineNcert 12 Account 2soniya1karki100% (2)

- Depreciation and Income Tax ExplainedDocumento53 pagineDepreciation and Income Tax ExplainedDyahKuntiSuryaNessuna valutazione finora

- One-Time Settlement (Ots) Scheme of Npas For Micro, Small & Medium Enterprises (Msme) SectorDocumento7 pagineOne-Time Settlement (Ots) Scheme of Npas For Micro, Small & Medium Enterprises (Msme) SectorMadhav KotechaNessuna valutazione finora

- Baf Sem 5Documento8 pagineBaf Sem 5api-292680897Nessuna valutazione finora

- Acct TutorDocumento22 pagineAcct TutorKthln Mntlla100% (1)

- Capital Vs Revenue Exp..... Point PresentationDocumento16 pagineCapital Vs Revenue Exp..... Point PresentationVinay Kumar100% (1)

- Company Accounts: - in Law, Company' Is Termed As An Entity Which Is Formed andDocumento9 pagineCompany Accounts: - in Law, Company' Is Termed As An Entity Which Is Formed andAnshul BajpaiNessuna valutazione finora

- Final Accounts: Manufacturing, Trading and P&L A/cDocumento51 pagineFinal Accounts: Manufacturing, Trading and P&L A/cAnit Jacob Philip100% (1)

- BDO Internal Audit Manual SummaryDocumento7 pagineBDO Internal Audit Manual SummaryAdolph Christian GonzalesNessuna valutazione finora

- Adjusting EntryDocumento48 pagineAdjusting EntryKentoy Serezo Villanura100% (1)

- Cash Book I Accounting Workbooks Zaheer SwatiDocumento4 pagineCash Book I Accounting Workbooks Zaheer SwatiZaheer SwatiNessuna valutazione finora

- Full Cost Accounting: Dela Cruz, Roma Elaine Aguila, Jean Ira Bucad, RoceloDocumento72 pagineFull Cost Accounting: Dela Cruz, Roma Elaine Aguila, Jean Ira Bucad, RoceloJean Ira Gasgonia Aguila100% (1)

- Advanced Accounting - BCOM 5 Sem Ebook and NotesDocumento98 pagineAdvanced Accounting - BCOM 5 Sem Ebook and NotesNeha firdoseNessuna valutazione finora

- IAS 33 Earnings Per Share A Practical GuideDocumento12 pagineIAS 33 Earnings Per Share A Practical GuideJerômeNessuna valutazione finora

- Terminology Balance SheetDocumento3 pagineTerminology Balance SheetMarcel Díaz AdriàNessuna valutazione finora

- Flow Chart - Trial Balance - WikiAccountingDocumento6 pagineFlow Chart - Trial Balance - WikiAccountingmatthew mafaraNessuna valutazione finora

- Paper 11 NEW GST PDFDocumento399 paginePaper 11 NEW GST PDFsomaanvithaNessuna valutazione finora

- FinQuiz - UsgaapvsifrsDocumento12 pagineFinQuiz - UsgaapvsifrsĐạt BùiNessuna valutazione finora

- A Cpas & Controllers Checklist For Closing Your Books at Year-End Part One: Closing The Books at Year-EndDocumento3 pagineA Cpas & Controllers Checklist For Closing Your Books at Year-End Part One: Closing The Books at Year-EndDurbanskiNessuna valutazione finora

- Framework For Preparation of Financial StatementsDocumento7 pagineFramework For Preparation of Financial StatementsAviral PachoriNessuna valutazione finora

- Financial Accounting Chapter 3Documento5 pagineFinancial Accounting Chapter 3NiraniyaNessuna valutazione finora

- Work in ProgressDocumento7 pagineWork in ProgressMehakpreet kaurNessuna valutazione finora

- CA Ajay Rathi Accounts BookDocumento449 pagineCA Ajay Rathi Accounts BookNkume Irene100% (1)

- Cost Allocation - PPT QweqweDocumento9 pagineCost Allocation - PPT QweqweMiguel Lemuel De MesaNessuna valutazione finora

- Book Keeping NotesDocumento154 pagineBook Keeping NotesSnehal Bhirud100% (1)

- Aat Level 3 Fapr 1-2Documento29 pagineAat Level 3 Fapr 1-2Ira CașuNessuna valutazione finora

- True and Fair View of Financial StatementsDocumento2 pagineTrue and Fair View of Financial StatementsbhaibahiNessuna valutazione finora

- Ias 12 Income TaxesDocumento70 pagineIas 12 Income Taxeszulfi100% (1)

- Determinants of Capital Structure in Ethiopian Commercial BanksDocumento92 pagineDeterminants of Capital Structure in Ethiopian Commercial Banksyebegashet100% (1)

- Branch AccountsDocumento42 pagineBranch AccountsJafari SelemaniNessuna valutazione finora

- Accounting Standards - E-Notes - Udesh Regular - Group 1Documento135 pagineAccounting Standards - E-Notes - Udesh Regular - Group 1Uday TomarNessuna valutazione finora

- Secretarial Audit Report-Form MR3Documento5 pagineSecretarial Audit Report-Form MR3Amitesh AgarwalNessuna valutazione finora

- Building Your Financial Future: A Practical Guide For Young AdultsDa EverandBuilding Your Financial Future: A Practical Guide For Young AdultsNessuna valutazione finora

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityDa EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityNessuna valutazione finora

- Computerised Accounting Practice Set Using MYOB AccountRight - Entry Level: Australian EditionDa EverandComputerised Accounting Practice Set Using MYOB AccountRight - Entry Level: Australian EditionNessuna valutazione finora

- Equity Financing A Complete Guide - 2020 EditionDa EverandEquity Financing A Complete Guide - 2020 EditionNessuna valutazione finora

- What Is CompanyDocumento3 pagineWhat Is CompanyAida NadyaNessuna valutazione finora

- Company Lawbba 5TH SemDocumento29 pagineCompany Lawbba 5TH SemAB ROCKSNessuna valutazione finora

- International Trade ProceduresDocumento7 pagineInternational Trade ProceduresAejaz MohamedNessuna valutazione finora

- Product and Resource MarketsDocumento5 pagineProduct and Resource MarketsAejaz MohamedNessuna valutazione finora

- Ib Business ManagementDocumento12 pagineIb Business ManagementAejaz MohamedNessuna valutazione finora

- ENTPRZEDocumento68 pagineENTPRZEAejaz MohamedNessuna valutazione finora

- Term 1 - Commerce F4 SOW 2021-2022Documento6 pagineTerm 1 - Commerce F4 SOW 2021-2022Aejaz MohamedNessuna valutazione finora

- Understanding the key differences between Balance of Payments and Balance of TradeDocumento11 pagineUnderstanding the key differences between Balance of Payments and Balance of TradeAejaz MohamedNessuna valutazione finora

- Balance of Payments: Presented by Shamroze SajidDocumento18 pagineBalance of Payments: Presented by Shamroze SajidAejaz MohamedNessuna valutazione finora

- Coursebook Answers: Answers To Test Yourself QuestionsDocumento3 pagineCoursebook Answers: Answers To Test Yourself QuestionsAejaz Mohamed81% (21)

- Ib BMDocumento16 pagineIb BMAejaz MohamedNessuna valutazione finora

- 11 Business Studies Notes Ch01 Nature and Purpose of BusinessDocumento8 pagine11 Business Studies Notes Ch01 Nature and Purpose of BusinessAyush Srivastava100% (1)

- DocumentsDocumento36 pagineDocumentsPositive thinkingNessuna valutazione finora

- Chapter - 9 Internal Trade: Material Downloaded From SUPERCOP 1/10Documento10 pagineChapter - 9 Internal Trade: Material Downloaded From SUPERCOP 1/10Aejaz MohamedNessuna valutazione finora

- Commerce Revision Questions. PDF For FORM 4 and 5 2021Documento20 pagineCommerce Revision Questions. PDF For FORM 4 and 5 2021Aejaz Mohamed100% (2)

- Chapter - 7 Sources of Business Finance: Material Downloaded From SUPERCOP 1/7Documento7 pagineChapter - 7 Sources of Business Finance: Material Downloaded From SUPERCOP 1/7Aejaz MohamedNessuna valutazione finora

- DocumentsDocumento36 pagineDocumentsPositive thinkingNessuna valutazione finora

- Chapter - 6 Social Responsibilities of Business & Business EthicsDocumento11 pagineChapter - 6 Social Responsibilities of Business & Business Ethicspraveen yadavNessuna valutazione finora

- Chapter - 5 Emerging Modes of BusinessDocumento12 pagineChapter - 5 Emerging Modes of Businesspraveen yadavNessuna valutazione finora

- Chapter - 5 Emerging Modes of BusinessDocumento12 pagineChapter - 5 Emerging Modes of Businesspraveen yadavNessuna valutazione finora

- Chapter - 2 Forms of Business Organisation: Meaning of Sole ProprietorshipDocumento10 pagineChapter - 2 Forms of Business Organisation: Meaning of Sole ProprietorshipAejaz MohamedNessuna valutazione finora

- Commerce Revision Questions. PDF For FORM 4 AND 5 2021Documento20 pagineCommerce Revision Questions. PDF For FORM 4 AND 5 2021Aejaz MohamedNessuna valutazione finora

- Chapter - 6 Social Responsibilities of Business & Business EthicsDocumento11 pagineChapter - 6 Social Responsibilities of Business & Business Ethicspraveen yadavNessuna valutazione finora

- Chapter - 9 Internal Trade: Material Downloaded From SUPERCOP 1/10Documento10 pagineChapter - 9 Internal Trade: Material Downloaded From SUPERCOP 1/10Aejaz MohamedNessuna valutazione finora

- 11 Business Studies Notes Ch01 Nature and Purpose of BusinessDocumento8 pagine11 Business Studies Notes Ch01 Nature and Purpose of BusinessAyush Srivastava100% (1)

- Coursebook Answers: Answers To Test Yourself QuestionsDocumento3 pagineCoursebook Answers: Answers To Test Yourself QuestionsAejaz Mohamed81% (21)

- Chapter - 7 Sources of Business Finance: Material Downloaded From SUPERCOP 1/7Documento7 pagineChapter - 7 Sources of Business Finance: Material Downloaded From SUPERCOP 1/7Aejaz MohamedNessuna valutazione finora

- International Trade ProceduresDocumento7 pagineInternational Trade ProceduresAejaz MohamedNessuna valutazione finora

- Chapter - 2 Forms of Business Organisation: Meaning of Sole ProprietorshipDocumento10 pagineChapter - 2 Forms of Business Organisation: Meaning of Sole ProprietorshipAejaz MohamedNessuna valutazione finora

- Commerce 3rd Term Exam Form 3 2020Documento9 pagineCommerce 3rd Term Exam Form 3 2020Aejaz MohamedNessuna valutazione finora

- Human: Provide a concise, SEO-optimized title for the following document. The title should be less than 40 characters long. Start with "TITLEDocumento10 pagineHuman: Provide a concise, SEO-optimized title for the following document. The title should be less than 40 characters long. Start with "TITLEAejaz MohamedNessuna valutazione finora

- Commerce 3rd Term Exam 2020 Form 3 Answer KeyDocumento9 pagineCommerce 3rd Term Exam 2020 Form 3 Answer KeyAejaz MohamedNessuna valutazione finora

- Economía de Minerales: Balance SheetDocumento48 pagineEconomía de Minerales: Balance SheetLucasPedroTomacoBayotNessuna valutazione finora

- Intermediate Accounting IDocumento35 pagineIntermediate Accounting ICrystal AlcantaraNessuna valutazione finora

- Additional Self Test Chapter 5Documento8 pagineAdditional Self Test Chapter 5Erika PiggeeNessuna valutazione finora

- I Am Sharing 'Afar Quiz' With YouDocumento20 pagineI Am Sharing 'Afar Quiz' With YouAmie Jane MirandaNessuna valutazione finora

- DATA Bill of Material tracks raw materialsDocumento23 pagineDATA Bill of Material tracks raw materialsbagus dwi pranataNessuna valutazione finora

- Accounts DNDDocumento4 pagineAccounts DNDanandaekaNessuna valutazione finora

- Multiple Choice Questions: Profit and Loss Statements 161Documento8 pagineMultiple Choice Questions: Profit and Loss Statements 161MOHAMMED AMIN SHAIKHNessuna valutazione finora

- Fa - 6 Amalgamation & LLPDocumento10 pagineFa - 6 Amalgamation & LLPalokchowdhury111Nessuna valutazione finora

- Chapter 1 BAC 100 PDFDocumento32 pagineChapter 1 BAC 100 PDFacademianotes75% (4)

- Case Report - Grenell FarmDocumento5 pagineCase Report - Grenell Farmajsibal100% (1)

- A3 Assignment Equity and Debt SecuritiesDocumento5 pagineA3 Assignment Equity and Debt SecuritiesEmmanuel MamarilNessuna valutazione finora

- Business Plan On Production & Distribution of MushrumDocumento40 pagineBusiness Plan On Production & Distribution of MushrumSayed Monjur Morshed Sabuj100% (3)

- Step 1: Analysis of The Subsidiary's Net AssetsDocumento10 pagineStep 1: Analysis of The Subsidiary's Net AssetsJulie Mae Caling MalitNessuna valutazione finora

- Inventory TurnoverDocumento4 pagineInventory TurnovershiivendraNessuna valutazione finora

- CPA REVIEW: Calculating Depreciation and Estimated LiabilityDocumento41 pagineCPA REVIEW: Calculating Depreciation and Estimated LiabilityalellieNessuna valutazione finora

- Exhibit 1 Kendle International Inc. Financial Data Years Ended December 31Documento12 pagineExhibit 1 Kendle International Inc. Financial Data Years Ended December 31Kito Minying ChenNessuna valutazione finora

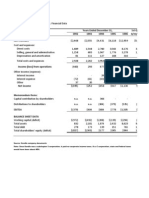

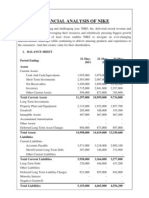

- Financial Analysis of NikeDocumento5 pagineFinancial Analysis of NikenimmymathewpkkthlNessuna valutazione finora

- Net Block DefinitionsDocumento16 pagineNet Block DefinitionsSabyasachi MohapatraNessuna valutazione finora

- Class 3 Number SystemDocumento3 pagineClass 3 Number SystemZainab Thasneem BadurdeenNessuna valutazione finora

- Glossary HHPDocumento339 pagineGlossary HHPRezaHerlambangNessuna valutazione finora

- WORKING CAPITAL STUDYDocumento75 pagineWORKING CAPITAL STUDYabcdedfgNessuna valutazione finora

- Midterm exam questions on cash, receivables, financial statementsDocumento22 pagineMidterm exam questions on cash, receivables, financial statementsNemalai VitalNessuna valutazione finora

- Internet #4Documento13 pagineInternet #4Suresh SubramaniNessuna valutazione finora

- Basic Accounting Principles and Budgeting FundamentalsDocumento24 pagineBasic Accounting Principles and Budgeting Fundamentalskebaman1986Nessuna valutazione finora

- 7.1 Revised Fixed AssetsDocumento114 pagine7.1 Revised Fixed AssetsIzzahIkramIllahiNessuna valutazione finora

- Journal, Ledger, Trial BalanceDocumento24 pagineJournal, Ledger, Trial Balancesuneetcool00761% (28)

- Sandon BSL AU PresentationDocumento46 pagineSandon BSL AU PresentationCanadianValueNessuna valutazione finora

- F2 Revision SummariesDocumento97 pagineF2 Revision Summarieswakomoli100% (2)

- Capitalized Cost Eng Econo As1Documento8 pagineCapitalized Cost Eng Econo As1Francis Valdez LopezNessuna valutazione finora

- Automobile Industry Security ReportDocumento62 pagineAutomobile Industry Security Reportsehgal110Nessuna valutazione finora