Potrebbero piacerti anche

- Visayas Avenue, Diliman, Quezon CityDocumento9 pagineVisayas Avenue, Diliman, Quezon CityJoy Valera RapaconNessuna valutazione finora

- Stem Cell Therapeutic CentreDocumento19 pagineStem Cell Therapeutic Centreentabs2016Nessuna valutazione finora

- PH - Philippine Tobacco Institute VDocumento10 paginePH - Philippine Tobacco Institute VLimVianesseNessuna valutazione finora

- Authorization LetterDocumento1 paginaAuthorization LetterLimVianesseNessuna valutazione finora

- RA9184 Overview1-PresentDocumento53 pagineRA9184 Overview1-PresentLimVianesse100% (1)

- AFFIDAVITSDocumento3 pagineAFFIDAVITSChelly MishyNessuna valutazione finora

- Affidavit To Use The Surname of The Father - , - Filipino - , - Single - , - 27 - , Years Old, ADocumento2 pagineAffidavit To Use The Surname of The Father - , - Filipino - , - Single - , - 27 - , Years Old, ALimVianesseNessuna valutazione finora

- Presentation StreamDocumento12 paginePresentation StreamLimVianesseNessuna valutazione finora

- Chapter 2Documento8 pagineChapter 2LimVianesseNessuna valutazione finora

- ScienceDocumento5 pagineScienceLimVianesseNessuna valutazione finora

- Human Rights Victim S Claim Application Form and FAQsDocumento23 pagineHuman Rights Victim S Claim Application Form and FAQsLimVianesseNessuna valutazione finora

- SYLLABUSDocumento7 pagineSYLLABUSLimVianesseNessuna valutazione finora

- GarmentsDocumento12 pagineGarmentsLimVianesseNessuna valutazione finora

- Ampatuan DecisionDocumento761 pagineAmpatuan DecisionGMA News Online100% (1)

- Different Kinds of ObligationDocumento7 pagineDifferent Kinds of ObligationLimVianesse100% (2)

- Obligations of debtor and creditor in real obligationsDocumento7 pagineObligations of debtor and creditor in real obligationsLimVianesseNessuna valutazione finora

- Cancellation of Lease AgreementDocumento1 paginaCancellation of Lease AgreementLimVianesseNessuna valutazione finora

- OCA Circular No. 90 2018Documento90 pagineOCA Circular No. 90 2018LimVianesseNessuna valutazione finora

- Seatwork 2Documento1 paginaSeatwork 2LimVianesseNessuna valutazione finora

- What Is Government Itself, But TheDocumento18 pagineWhat Is Government Itself, But TheLimVianesseNessuna valutazione finora

- PPMP 2018 Entire SPDocumento17 paginePPMP 2018 Entire SPLimVianesseNessuna valutazione finora

- Acceptance FormDocumento2 pagineAcceptance FormLimVianesse100% (1)

- Cancellation of Lease AgreementDocumento1 paginaCancellation of Lease AgreementLimVianesseNessuna valutazione finora

- Work Experience Sheet: Instructions: 1. Include Only The Work Experiences Relevant To The Position Being Applied ForDocumento1 paginaWork Experience Sheet: Instructions: 1. Include Only The Work Experiences Relevant To The Position Being Applied ForLimVianesseNessuna valutazione finora

- GSIS Retirement Benefit Options Under RA 8291Documento2 pagineGSIS Retirement Benefit Options Under RA 8291LimVianesseNessuna valutazione finora

- Loan Agreement With Real Estate MortgageDocumento3 pagineLoan Agreement With Real Estate MortgageLimVianesse100% (2)

- MCLE Form No. 13Documento1 paginaMCLE Form No. 13LimVianesseNessuna valutazione finora

- Board Resolution Change in Signatories PDFDocumento5 pagineBoard Resolution Change in Signatories PDFRea Ann Autor LiraNessuna valutazione finora

- Loan Agreement With Real Estate MortgageDocumento3 pagineLoan Agreement With Real Estate MortgageLimVianesse100% (2)

- Election Protest FormatDocumento1 paginaElection Protest FormatLimVianesseNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- UBP Corp Credit Card Application Form - New FillableDocumento7 pagineUBP Corp Credit Card Application Form - New FillableAdam Albert DomendenNessuna valutazione finora

- CCBCDocumento7 pagineCCBCapi-325149905Nessuna valutazione finora

- Delivery Challan DetailsDocumento4 pagineDelivery Challan Detailsmrcopy xeroxNessuna valutazione finora

- Tax Planning.: Dhruv Desai. Shriyans JainDocumento13 pagineTax Planning.: Dhruv Desai. Shriyans JainShreyans JainNessuna valutazione finora

- Tata Power Compensation 2013Documento5 pagineTata Power Compensation 2013Vivek SinghNessuna valutazione finora

- Aguinaldo Vs CIR #Tax-1Documento2 pagineAguinaldo Vs CIR #Tax-1Earl TagraNessuna valutazione finora

- ASSIGNMENT 1 (Corporate TAX)Documento10 pagineASSIGNMENT 1 (Corporate TAX)SandeepNessuna valutazione finora

- Husky 2015Documento12 pagineHusky 2015sonicbooahxxxNessuna valutazione finora

- Income Tax Department: Computerized Payment Receipt (CPR - It)Documento2 pagineIncome Tax Department: Computerized Payment Receipt (CPR - It)desaya3859Nessuna valutazione finora

- ERES ApplicationDocumento4 pagineERES ApplicationSnovia MohsinNessuna valutazione finora

- Ref No ECILDocumento1 paginaRef No ECILjude francoNessuna valutazione finora

- Bank Fees and Charges Guide for Peso TransactionsDocumento9 pagineBank Fees and Charges Guide for Peso TransactionsRod LaquintaNessuna valutazione finora

- WAY4 Overview SmallDocumento8 pagineWAY4 Overview SmallDipanwita BhuyanNessuna valutazione finora

- RG1575748 PDFDocumento1 paginaRG1575748 PDFJohn BakerNessuna valutazione finora

- InvoiceDocumento1 paginaInvoiceLe NgocNessuna valutazione finora

- c.11. Filipinas Synthetic Fiber Corp v. CADocumento1 paginac.11. Filipinas Synthetic Fiber Corp v. CAArbie LlesisNessuna valutazione finora

- Electronic Credit LedgerDocumento2 pagineElectronic Credit LedgerAakshaNessuna valutazione finora

- GST On Construction Done For Landlords Under Joint Development Agreement PDFDocumento7 pagineGST On Construction Done For Landlords Under Joint Development Agreement PDFAman JainNessuna valutazione finora

- 10.20.22 Letter Gretchen Sierra CTC PRDocumento2 pagine10.20.22 Letter Gretchen Sierra CTC PRMetro Puerto RicoNessuna valutazione finora

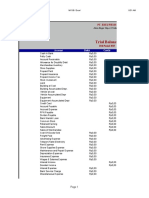

- Trial Balance - Melvino YDocumento4 pagineTrial Balance - Melvino YTrainingDigital Marketing BandungNessuna valutazione finora

- Offshore Vessel InvoiceDocumento3 pagineOffshore Vessel Invoicemichael seanNessuna valutazione finora

- Question Analysis ICAB Application Level TAXATION-II (Syllabus Weight Based) PDFDocumento50 pagineQuestion Analysis ICAB Application Level TAXATION-II (Syllabus Weight Based) PDFTwsif Tanvir Tanoy92% (13)

- GMG Vendor FormDocumento2 pagineGMG Vendor FormsandyNessuna valutazione finora

- View bank statement online for Mr Juan RamosDocumento2 pagineView bank statement online for Mr Juan RamosLong Home ProductsNessuna valutazione finora

- CA Final Idt GST Customs Flow Charts May June 2019Documento187 pagineCA Final Idt GST Customs Flow Charts May June 2019yogeshaggarwal09Nessuna valutazione finora

- PS 202106070069Documento1 paginaPS 202106070069Vivek VermaNessuna valutazione finora

- Electronic Reservation Slip (ERS) : 4355018466 07436/NCJ KCG SPL Ac 3 Tier Sleeper (3A)Documento3 pagineElectronic Reservation Slip (ERS) : 4355018466 07436/NCJ KCG SPL Ac 3 Tier Sleeper (3A)Navin KumarNessuna valutazione finora

- Hindustan Petroleum Corp. Ltd. Price ListDocumento19 pagineHindustan Petroleum Corp. Ltd. Price Listyeaturi96Nessuna valutazione finora

- FI - Tabelas Do SAPDocumento65 pagineFI - Tabelas Do SAPregis0009Nessuna valutazione finora

- Generation-Skipping Transfer Tax Return For Terminations: General InformationDocumento3 pagineGeneration-Skipping Transfer Tax Return For Terminations: General InformationIRSNessuna valutazione finora