Potrebbero piacerti anche

- Ninepoint Tec Private Credit Fund OmDocumento86 pagineNinepoint Tec Private Credit Fund OmleminhptnkNessuna valutazione finora

- Active Alpha: A Portfolio Approach to Selecting and Managing Alternative InvestmentsDa EverandActive Alpha: A Portfolio Approach to Selecting and Managing Alternative InvestmentsNessuna valutazione finora

- Accounting for Derivatives: Advanced Hedging under IFRSDa EverandAccounting for Derivatives: Advanced Hedging under IFRSNessuna valutazione finora

- Alternative Investment Strategies A Complete Guide - 2020 EditionDa EverandAlternative Investment Strategies A Complete Guide - 2020 EditionNessuna valutazione finora

- CLO Investing: With an Emphasis on CLO Equity & BB NotesDa EverandCLO Investing: With an Emphasis on CLO Equity & BB NotesNessuna valutazione finora

- Alternative Investments Complete Self-Assessment GuideDa EverandAlternative Investments Complete Self-Assessment GuideNessuna valutazione finora

- Alternative Investment FundsDocumento10 pagineAlternative Investment Fundskrishna sharmaNessuna valutazione finora

- Hedge Fund Due Diligence: Professional Tools to Investigate Hedge Fund ManagersDa EverandHedge Fund Due Diligence: Professional Tools to Investigate Hedge Fund ManagersNessuna valutazione finora

- Alternative Investment FundsDocumento10 pagineAlternative Investment Fundskrishna sharmaNessuna valutazione finora

- Investment Fund Leagle DocumentsDocumento6 pagineInvestment Fund Leagle Documentspradeebha100% (1)

- Private Equity Unchained: Strategy Insights for the Institutional InvestorDa EverandPrivate Equity Unchained: Strategy Insights for the Institutional InvestorNessuna valutazione finora

- Fund ManagementDocumento12 pagineFund ManagementstabrezhassanNessuna valutazione finora

- Private Equity Fund Of Funds A Complete Guide - 2020 EditionDa EverandPrivate Equity Fund Of Funds A Complete Guide - 2020 EditionNessuna valutazione finora

- Shubham Hedge FundDocumento71 pagineShubham Hedge FundfgersgtesrtgeNessuna valutazione finora

- Loan Workouts and Debt for Equity Swaps: A Framework for Successful Corporate RescuesDa EverandLoan Workouts and Debt for Equity Swaps: A Framework for Successful Corporate RescuesValutazione: 5 su 5 stelle5/5 (1)

- The Handbook for Investment Committee Members: How to Make Prudent Investments for Your OrganizationDa EverandThe Handbook for Investment Committee Members: How to Make Prudent Investments for Your OrganizationNessuna valutazione finora

- Buyouts: Success for Owners, Management, PEGs, ESOPs and Mergers and AcquisitionsDa EverandBuyouts: Success for Owners, Management, PEGs, ESOPs and Mergers and AcquisitionsNessuna valutazione finora

- Funds: Private Equity, Hedge and All Core StructuresDa EverandFunds: Private Equity, Hedge and All Core StructuresNessuna valutazione finora

- Behind the Curve: An Analysis of the Investment Behavior of Private Equity FundsDa EverandBehind the Curve: An Analysis of the Investment Behavior of Private Equity FundsNessuna valutazione finora

- Bond Portfolio Management StrategiesDocumento32 pagineBond Portfolio Management StrategiesSwati VermaNessuna valutazione finora

- Social Impact Bond CaseDocumento21 pagineSocial Impact Bond CaseTest123Nessuna valutazione finora

- Structured Finance and Insurance: The ART of Managing Capital and RiskDa EverandStructured Finance and Insurance: The ART of Managing Capital and RiskValutazione: 3 su 5 stelle3/5 (1)

- Risk Finance and Asset Pricing: Value, Measurements, and MarketsDa EverandRisk Finance and Asset Pricing: Value, Measurements, and MarketsNessuna valutazione finora

- Public Private Equity Partnerships and Climate ChangeDocumento52 paginePublic Private Equity Partnerships and Climate ChangeInternational Finance Corporation (IFC)Nessuna valutazione finora

- Reading 45-Private Equity Valuation-QuestionDocumento20 pagineReading 45-Private Equity Valuation-QuestionThekkla Zena100% (1)

- SS 01 Quiz 2 PDFDocumento60 pagineSS 01 Quiz 2 PDFYellow CarterNessuna valutazione finora

- Foreign Exchange Operations: Master Trading Agreements, Settlement, and CollateralDa EverandForeign Exchange Operations: Master Trading Agreements, Settlement, and CollateralNessuna valutazione finora

- The Handbook of Credit Risk Management: Originating, Assessing, and Managing Credit ExposuresDa EverandThe Handbook of Credit Risk Management: Originating, Assessing, and Managing Credit ExposuresNessuna valutazione finora

- Modern Investment Management: An Equilibrium ApproachDa EverandModern Investment Management: An Equilibrium ApproachValutazione: 3.5 su 5 stelle3.5/5 (4)

- Inside Private Equity: The Professional Investor's HandbookDa EverandInside Private Equity: The Professional Investor's HandbookNessuna valutazione finora

- Fund AccountingDocumento7 pagineFund AccountingMayuresh Shirsat100% (1)

- The Financial Advisor M&A Guidebook: Best Practices, Tools, and Resources for Technology Integration and BeyondDa EverandThe Financial Advisor M&A Guidebook: Best Practices, Tools, and Resources for Technology Integration and BeyondNessuna valutazione finora

- Private Equity Funds Performance EvaluationDocumento5 paginePrivate Equity Funds Performance Evaluationgnachev_4100% (1)

- Fund PerformanceDocumento13 pagineFund PerformanceHilal MilmoNessuna valutazione finora

- Kickstart Your Corporation: The Incorporated Professional's Financial Planning CoachDa EverandKickstart Your Corporation: The Incorporated Professional's Financial Planning CoachNessuna valutazione finora

- Investment Leadership and Portfolio Management: The Path to Successful Stewardship for Investment FirmsDa EverandInvestment Leadership and Portfolio Management: The Path to Successful Stewardship for Investment FirmsNessuna valutazione finora

- Alternative Invesmtents For Pension FundsDocumento35 pagineAlternative Invesmtents For Pension FundsQuantmetrixNessuna valutazione finora

- Leadership Risk: A Guide for Private Equity and Strategic InvestorsDa EverandLeadership Risk: A Guide for Private Equity and Strategic InvestorsNessuna valutazione finora

- 2 Real Options in Theory and PracticeDocumento50 pagine2 Real Options in Theory and Practicedxc12670Nessuna valutazione finora

- Process and Asset Valuation A Complete Guide - 2019 EditionDa EverandProcess and Asset Valuation A Complete Guide - 2019 EditionNessuna valutazione finora

- CAIA Candidate HandbookDocumento12 pagineCAIA Candidate HandbookAshlesh SonjeNessuna valutazione finora

- Career Guides - Leveraged Finance & Credit Risk Management Free GuideDocumento9 pagineCareer Guides - Leveraged Finance & Credit Risk Management Free GuideRublesNessuna valutazione finora

- Lecture 5 - A Note On Valuation in Private EquityDocumento85 pagineLecture 5 - A Note On Valuation in Private EquitySinan DenizNessuna valutazione finora

- Investment Management: Meeting the Noble Challenges of Funding Pensions, Deficits, and GrowthDa EverandInvestment Management: Meeting the Noble Challenges of Funding Pensions, Deficits, and GrowthWayne H. WagnerNessuna valutazione finora

- M&A Disputes: A Professional Guide to Accounting ArbitrationsDa EverandM&A Disputes: A Professional Guide to Accounting ArbitrationsNessuna valutazione finora

- Investment Leadership: Building a Winning Culture for Long-Term SuccessDa EverandInvestment Leadership: Building a Winning Culture for Long-Term SuccessNessuna valutazione finora

- Capital Structure A Complete Guide - 2020 EditionDa EverandCapital Structure A Complete Guide - 2020 EditionNessuna valutazione finora

- Punching Above Your Weight: Minority Investments in PE: Portfolio Media. Inc. - 111 West 19Documento4 paginePunching Above Your Weight: Minority Investments in PE: Portfolio Media. Inc. - 111 West 19Jon Van TuinNessuna valutazione finora

- Investment and Portfolio ManageemntDocumento2 pagineInvestment and Portfolio Manageemntumair aliNessuna valutazione finora

- Private Equity and Pricing Value CreationDocumento12 paginePrivate Equity and Pricing Value CreationANUSHKA GOYALNessuna valutazione finora

- The New Science of Asset Allocation: Risk Management in a Multi-Asset WorldDa EverandThe New Science of Asset Allocation: Risk Management in a Multi-Asset WorldNessuna valutazione finora

- PIPE Investments of Private Equity Funds: The temptation of public equity investments to private equity firmsDa EverandPIPE Investments of Private Equity Funds: The temptation of public equity investments to private equity firmsNessuna valutazione finora

- Investment Decision and Portfolio Management (ACFN 632)Documento23 pagineInvestment Decision and Portfolio Management (ACFN 632)Hussen AbdulkadirNessuna valutazione finora

- B Pension Risk TransferDocumento7 pagineB Pension Risk TransferMikhail FrancisNessuna valutazione finora

- 2017-11-01 Builders Line English EditionDocumento56 pagine2017-11-01 Builders Line English EditionBhaskar ShanmugamNessuna valutazione finora

- EY-RAI Pulse of Indian Retail Market FinalDocumento16 pagineEY-RAI Pulse of Indian Retail Market Finalnehal vaghelaNessuna valutazione finora

- The God's Destiny (Final)Documento179 pagineThe God's Destiny (Final)Bhaskar ShanmugamNessuna valutazione finora

- PMLAnnualReport 2014Documento224 paginePMLAnnualReport 2014Bhaskar ShanmugamNessuna valutazione finora

- Retail Realty in India Vs Asian CountriesDocumento28 pagineRetail Realty in India Vs Asian Countriesashimasehgal0112Nessuna valutazione finora

- Mumbai PremiumsDocumento1 paginaMumbai PremiumsBhaskar ShanmugamNessuna valutazione finora

- BLR Hyd 5893962462708 BSDocumento1 paginaBLR Hyd 5893962462708 BSBhaskar ShanmugamNessuna valutazione finora

- Annual Survey of Industries Vol I 2009-10Documento879 pagineAnnual Survey of Industries Vol I 2009-10Bhaskar Shanmugam0% (1)

- Office Traction@Glance - Dec 2012 - Bangalore PDFDocumento3 pagineOffice Traction@Glance - Dec 2012 - Bangalore PDFBhaskar ShanmugamNessuna valutazione finora

- Office Traction@Glance - Dec 2012 - Bangalore PDFDocumento3 pagineOffice Traction@Glance - Dec 2012 - Bangalore PDFBhaskar ShanmugamNessuna valutazione finora

- Annual Survey of Industries 2008-09 Vol. IDocumento671 pagineAnnual Survey of Industries 2008-09 Vol. IBhaskar ShanmugamNessuna valutazione finora

- 936 - III - BAngalore RuralDocumento221 pagine936 - III - BAngalore RuralBhaskar ShanmugamNessuna valutazione finora

- 56 SEIAA Meeting (3.10.2012) PDFDocumento91 pagine56 SEIAA Meeting (3.10.2012) PDFBhaskar ShanmugamNessuna valutazione finora

- 53rd SEIAA Meeting (06.07.2012) - 1Documento84 pagine53rd SEIAA Meeting (06.07.2012) - 1Bhaskar ShanmugamNessuna valutazione finora

- Is Real Estate in India in A BubbleDocumento3 pagineIs Real Estate in India in A BubbleBhaskar ShanmugamNessuna valutazione finora

- 53rd SEIAA Meeting (06.07.2012) - 1Documento84 pagine53rd SEIAA Meeting (06.07.2012) - 1Bhaskar ShanmugamNessuna valutazione finora

- 55th SEIAA Meeting - 03.09.2012Documento64 pagine55th SEIAA Meeting - 03.09.2012Bhaskar ShanmugamNessuna valutazione finora

- Bangalore Residential Report May 2012Documento44 pagineBangalore Residential Report May 2012Bhaskar ShanmugamNessuna valutazione finora

- Private Equity Buy Side Financial Model and ValuationDocumento19 paginePrivate Equity Buy Side Financial Model and ValuationBhaskar Shanmugam100% (3)

- E&R at Glance: JANUARY 2013Documento3 pagineE&R at Glance: JANUARY 2013Bhaskar ShanmugamNessuna valutazione finora

- Keys PreDocumento79 pagineKeys PreBhaskar ShanmugamNessuna valutazione finora

- IT Policy-Draft 2011Documento18 pagineIT Policy-Draft 2011Bhaskar ShanmugamNessuna valutazione finora

- Karnataka: An Overview: C Max. 40 CDocumento17 pagineKarnataka: An Overview: C Max. 40 CBhaskar Shanmugam100% (1)

- MOU's Bangalore UrbanDocumento5 pagineMOU's Bangalore UrbanBhaskar ShanmugamNessuna valutazione finora

- HybridDocumento22 pagineHybridBhaskar ShanmugamNessuna valutazione finora

- PRR Can Dry Up TG Halli Catchment AreaDocumento2 paginePRR Can Dry Up TG Halli Catchment AreaBhaskar ShanmugamNessuna valutazione finora

- L'Occitane Enters Indian Spa MarketDocumento1 paginaL'Occitane Enters Indian Spa MarketBhaskar ShanmugamNessuna valutazione finora

- MITOCW - 10. Financial System Challenges & OpportunitiesDocumento32 pagineMITOCW - 10. Financial System Challenges & OpportunitiesAnjali AhujaNessuna valutazione finora

- Fs SP Pan Arab CompositeDocumento6 pagineFs SP Pan Arab CompositeMarNessuna valutazione finora

- Old Bridge Mutual Fund - Factsheet March 2024Documento8 pagineOld Bridge Mutual Fund - Factsheet March 2024Bharathi 3280Nessuna valutazione finora

- Digital Marketing Channel and Celebrity Endorsement Analysis of Online Mutual Fund Purchase Decisions With Mutual Fund Performance MediationDocumento12 pagineDigital Marketing Channel and Celebrity Endorsement Analysis of Online Mutual Fund Purchase Decisions With Mutual Fund Performance MediationInternational Journal of Innovative Science and Research TechnologyNessuna valutazione finora

- Monthly Portfolio As On 30th June 2021Documento367 pagineMonthly Portfolio As On 30th June 2021muhsinNessuna valutazione finora

- Petition Against Starcomms PP and Chapel Hill Denham - 180512 - Morgan CapitalDocumento10 paginePetition Against Starcomms PP and Chapel Hill Denham - 180512 - Morgan CapitalProshareNessuna valutazione finora

- Islamic Financial Planner - Module One (Revision) Financial Planning Industry in MalaysiaDocumento16 pagineIslamic Financial Planner - Module One (Revision) Financial Planning Industry in MalaysiaShahizan Md Noh100% (1)

- Project Report On Tata Aia Life InsuranceDocumento52 pagineProject Report On Tata Aia Life Insurancevipinkathpal25% (4)

- 1Documento11 pagine1PHƯƠNG ĐẶNG DƯƠNG XUÂNNessuna valutazione finora

- Accelerating Capital Markets Development in Emerging EconomiesDocumento26 pagineAccelerating Capital Markets Development in Emerging EconomiesIchbin BinNessuna valutazione finora

- Investment Option Through BajajDocumento57 pagineInvestment Option Through BajajSiddiqua AnsariNessuna valutazione finora

- Mutual Fund: Mutual Funds in IndiaDocumento12 pagineMutual Fund: Mutual Funds in IndiaNirali AntaniNessuna valutazione finora

- Aequitas InvestmentsDocumento5 pagineAequitas InvestmentsSantosh RoutNessuna valutazione finora

- Sriram Insight Financial ProjectDocumento99 pagineSriram Insight Financial ProjectVinay Bhandari100% (1)

- DMS-IIT Delhi Compendium 2019-21Documento55 pagineDMS-IIT Delhi Compendium 2019-21Sounak Chatterjee100% (1)

- Key Investor Information: Vanguard Lifestrategy® 20% Equity Fund (The "Fund")Documento2 pagineKey Investor Information: Vanguard Lifestrategy® 20% Equity Fund (The "Fund")Cristian GherghiţăNessuna valutazione finora

- Project Mutual Funds Awareness 47Documento24 pagineProject Mutual Funds Awareness 47m.com22shiudkarsudarshanNessuna valutazione finora

- Security Bank - UITF Investment ReportDocumento2 pagineSecurity Bank - UITF Investment ReportgwapongkabayoNessuna valutazione finora

- Mutual Fund Investor Attitude Towards RiskDocumento67 pagineMutual Fund Investor Attitude Towards RiskBinoyNessuna valutazione finora

- Description of Securities and Risks Related To Securities EngDocumento7 pagineDescription of Securities and Risks Related To Securities EngNikhilparakhNessuna valutazione finora

- Project Report: Mutual FundDocumento32 pagineProject Report: Mutual FundArian HaqueNessuna valutazione finora

- HSBC Amfi Mock Test-1Documento10 pagineHSBC Amfi Mock Test-1Ankit Sharma100% (1)

- Analysis On Axis BankDocumento99 pagineAnalysis On Axis BankNiket_Verma_8763Nessuna valutazione finora

- Biitm-IFSS-Mutual Funds - ZoomDocumento55 pagineBiitm-IFSS-Mutual Funds - ZoomBikash Kumar DashNessuna valutazione finora

- Sudipta Shib-21bsp1265-Group 3 (Ibs-Mumbai)Documento9 pagineSudipta Shib-21bsp1265-Group 3 (Ibs-Mumbai)Joy OfficialNessuna valutazione finora

- IC VAR LIFE - Reviewer With Answer KeyDocumento15 pagineIC VAR LIFE - Reviewer With Answer KeyDalton Jay LuzaNessuna valutazione finora

- International FinanceDocumento47 pagineInternational Financedohongvinh40Nessuna valutazione finora

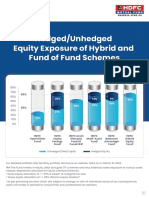

- Leaflet - Hedged and Unhedged Exposure of Hybrid FundsDocumento2 pagineLeaflet - Hedged and Unhedged Exposure of Hybrid FundsDeepakNessuna valutazione finora

- Self Attempt Questions - SolutionsDocumento5 pagineSelf Attempt Questions - SolutionsShermaine WanNessuna valutazione finora

- Research ProjectDocumento64 pagineResearch ProjectSaurabh RautNessuna valutazione finora