Potrebbero piacerti anche

- The Green to Gold Business Playbook: How to Implement Sustainability Practices for Bottom-Line Results in Every Business FunctionDa EverandThe Green to Gold Business Playbook: How to Implement Sustainability Practices for Bottom-Line Results in Every Business FunctionValutazione: 5 su 5 stelle5/5 (1)

- Chap 10Documento43 pagineChap 10Boo LeNessuna valutazione finora

- Horngrens Accounting 10Th Edition Nobles Solutions Manual Full Chapter PDFDocumento36 pagineHorngrens Accounting 10Th Edition Nobles Solutions Manual Full Chapter PDFelizabeth.hayes136100% (10)

- Topic 4 PP&EDocumento62 pagineTopic 4 PP&Efastidious_5100% (1)

- Principles of Accounting Chapter 9Documento43 paginePrinciples of Accounting Chapter 9myrentistoodamnhigh100% (1)

- CH 10Documento23 pagineCH 10Aftab MohammedNessuna valutazione finora

- Weygandt Accounting Principles 10e PowerPoint Ch10Documento79 pagineWeygandt Accounting Principles 10e PowerPoint Ch10billy93100% (1)

- Chapter 11 DepreciationDocumento18 pagineChapter 11 Depreciationyagnesh211733Nessuna valutazione finora

- ch10 Plant Assets, Natural Resources, and Intangible AssetsDocumento62 paginech10 Plant Assets, Natural Resources, and Intangible AssetsNuttakan Meesuk100% (5)

- 157 35295 EY121 2013 1 2 1 Chap010Documento46 pagine157 35295 EY121 2013 1 2 1 Chap010alaamabood6Nessuna valutazione finora

- 3415 Corporate Finance Assignment 2: Dean CulliganDocumento13 pagine3415 Corporate Finance Assignment 2: Dean CulliganAdam RogersNessuna valutazione finora

- Financial and Managerial Accounting 11th Edition Warren Solutions ManualDocumento10 pagineFinancial and Managerial Accounting 11th Edition Warren Solutions Manualcharlesdrakejth100% (14)

- Introduction To Financial Accounting: Long-Lived AssetsDocumento58 pagineIntroduction To Financial Accounting: Long-Lived AssetsShubham Kaushik100% (1)

- Acounting Aacounting Aacounting Aacounting ADocumento8 pagineAcounting Aacounting Aacounting Aacounting AFrankyLimNessuna valutazione finora

- Chapter 10 - SolutionsDocumento25 pagineChapter 10 - SolutionsGerald SusanteoNessuna valutazione finora

- Chapter 10 Plant Assets, Natural Resources, and Intangible Assets (13 E)Documento18 pagineChapter 10 Plant Assets, Natural Resources, and Intangible Assets (13 E)Raa100% (1)

- Accounting Chap10 - MKDocumento40 pagineAccounting Chap10 - MKavirgNessuna valutazione finora

- Long Live AssetsDocumento16 pagineLong Live AssetsLu CasNessuna valutazione finora

- CH 10Documento64 pagineCH 10anmonegamingNessuna valutazione finora

- Seminar 3Documento37 pagineSeminar 3hashtagjxNessuna valutazione finora

- Accounting For and Presentation of Property, Plant, and Equipment, and Other Noncurrent AssetsDocumento54 pagineAccounting For and Presentation of Property, Plant, and Equipment, and Other Noncurrent AssetsdanterozaNessuna valutazione finora

- Quiz QuestionsDocumento29 pagineQuiz QuestionsMuhammad M BhattiNessuna valutazione finora

- Prepare Financial Reports Edited HAND OUT1Documento34 paginePrepare Financial Reports Edited HAND OUT1getachewhabtamu361Nessuna valutazione finora

- Non Current AssetsDocumento44 pagineNon Current AssetsSandee Angeli Maceda Villarta100% (1)

- Control No 3 V MF XXVIII Tema B SolucionarioDocumento7 pagineControl No 3 V MF XXVIII Tema B SolucionarioJohnny TrujilloNessuna valutazione finora

- Accelerated Depreciation MethodsDocumento4 pagineAccelerated Depreciation MethodsIvan PachecoNessuna valutazione finora

- Acc101 - Chapter 8: Accounting For Long-Term AssetsDocumento18 pagineAcc101 - Chapter 8: Accounting For Long-Term AssetsMauricio Ace100% (1)

- Chap 11 KTTC2Documento9 pagineChap 11 KTTC2Viet Ha HoangNessuna valutazione finora

- ACCADocumento12 pagineACCAAbdulHameedAdamNessuna valutazione finora

- Adjustments To Financial StatementsDocumento7 pagineAdjustments To Financial StatementsClemyNessuna valutazione finora

- Plant Assets, Natural Resources and Intangibles: QuestionsDocumento42 paginePlant Assets, Natural Resources and Intangibles: QuestionsCh Radeel MurtazaNessuna valutazione finora

- IAS 7 - Statement of Cash FlowsDocumento21 pagineIAS 7 - Statement of Cash FlowsTD2 from Henry HarvinNessuna valutazione finora

- Analysis Solutions Acc 411Documento13 pagineAnalysis Solutions Acc 411dre_emNessuna valutazione finora

- Taller Uno Acco 112Documento44 pagineTaller Uno Acco 112api-274120622Nessuna valutazione finora

- Cash Flow & TaxesDocumento11 pagineCash Flow & TaxesPartha ChakaravartiNessuna valutazione finora

- Chapter 10 1Documento63 pagineChapter 10 1HEM CHEANessuna valutazione finora

- Chapter 12 Intangible Assets: Limited-Life Intangibles-Over Useful LifeDocumento19 pagineChapter 12 Intangible Assets: Limited-Life Intangibles-Over Useful LifespatelsalesforceNessuna valutazione finora

- CH 09Documento79 pagineCH 09Chang Chan ChongNessuna valutazione finora

- Topic Vii:: Long-Lived Nonmonetary AssetsDocumento23 pagineTopic Vii:: Long-Lived Nonmonetary AssetsDiana Maria100% (1)

- Review of Chapter 6Documento54 pagineReview of Chapter 6BookAddict721Nessuna valutazione finora

- Long-Lived Assets: 15.511 Corporate Accounting Summer 2004 Professor SP KothariDocumento24 pagineLong-Lived Assets: 15.511 Corporate Accounting Summer 2004 Professor SP KothariLu CasNessuna valutazione finora

- CHAPTER 5 - Depreciation and Equipment ReplacementDocumento22 pagineCHAPTER 5 - Depreciation and Equipment ReplacementruhamaNessuna valutazione finora

- Chapter 8 SolutionsDocumento66 pagineChapter 8 SolutionssevtenNessuna valutazione finora

- Engineering Economics - DepreciationDocumento13 pagineEngineering Economics - DepreciationAbdulrahman HaidarNessuna valutazione finora

- Lecture - 6 - Long - Term - Assets - NUS ACC1002 2020 SpringDocumento49 pagineLecture - 6 - Long - Term - Assets - NUS ACC1002 2020 SpringZenyui100% (1)

- Cash Flow Estimation and Capital BudgetingDocumento31 pagineCash Flow Estimation and Capital BudgetingjoanabudNessuna valutazione finora

- CH 09Documento37 pagineCH 09Gaurav KarkiNessuna valutazione finora

- CHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)Documento20 pagineCHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)VerrelyNessuna valutazione finora

- Problem 10Documento6 pagineProblem 10Atika DaretyNessuna valutazione finora

- Chapter 9 Summary: For Asset Disposal Through Discarding or SellingDocumento2 pagineChapter 9 Summary: For Asset Disposal Through Discarding or SellingAreeba QureshiNessuna valutazione finora

- QUIZ 3 CompileDocumento12 pagineQUIZ 3 CompileChanel AnnNessuna valutazione finora

- Trial BalanceDocumento27 pagineTrial Balancetaniya17Nessuna valutazione finora

- AccountingDocumento26 pagineAccountingHaris AliNessuna valutazione finora

- Reporting and Analyzing Long-Term Assets: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinDocumento71 pagineReporting and Analyzing Long-Term Assets: © The Mcgraw-Hill Companies, Inc., 2010 Mcgraw-Hill/IrwinYvonne Teo Yee VoonNessuna valutazione finora

- Auditing Problem ReviewerDocumento12 pagineAuditing Problem ReviewerJan Amora Pueblo0% (4)

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Da EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Valutazione: 3.5 su 5 stelle3.5/5 (17)

- CPA Review Notes 2019 - BEC (Business Environment Concepts)Da EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Valutazione: 4 su 5 stelle4/5 (9)

- Finance for IT Decision Makers: A practical handbookDa EverandFinance for IT Decision Makers: A practical handbookNessuna valutazione finora

- Marketing EducaționalDocumento13 pagineMarketing EducaționalPanus AlionaNessuna valutazione finora

- Robert Marciniak Manuscript Standardization As Key Issue in SSCDocumento10 pagineRobert Marciniak Manuscript Standardization As Key Issue in SSCMattNessuna valutazione finora

- Distribution Construction Standard Overhead SystemsDocumento620 pagineDistribution Construction Standard Overhead SystemsRickNessuna valutazione finora

- Environmental Economics Dissertation TopicsDocumento6 pagineEnvironmental Economics Dissertation TopicsWriteMyPaperOneDayUK100% (1)

- Lesson 13-COT 4TH QUARTERDocumento40 pagineLesson 13-COT 4TH QUARTERmaria genioNessuna valutazione finora

- Statement of Account: Republic of The Philippines Department of Health Southern Isabela Medical CenterDocumento1 paginaStatement of Account: Republic of The Philippines Department of Health Southern Isabela Medical CenterNHUJBETH INTERNET CAFENessuna valutazione finora

- Homework 2 DoneDocumento4 pagineHomework 2 Donemythien94Nessuna valutazione finora

- Was Milton Friedman A Socialist? Yes.: MEST Journal January 2013Documento17 pagineWas Milton Friedman A Socialist? Yes.: MEST Journal January 2013Raphaël FromEverNessuna valutazione finora

- Apptitude Model G12 2015Documento13 pagineApptitude Model G12 2015Emebet Debissa100% (1)

- Genealogical Sketch of William SimondsDocumento39 pagineGenealogical Sketch of William SimondsseanredmondNessuna valutazione finora

- Master Fee Schedule (Policy-Fees) 2022 Draft Plus MemoDocumento109 pagineMaster Fee Schedule (Policy-Fees) 2022 Draft Plus MemoNBC MontanaNessuna valutazione finora

- Turning Great Strategy Into Great PerformanceDocumento22 pagineTurning Great Strategy Into Great PerformanceCathy Jeny Jeny Catherine100% (2)

- NS ES 0048 Steam Generator - ALLDocumento2 pagineNS ES 0048 Steam Generator - ALLbartney chenNessuna valutazione finora

- Tutorial 5Documento3 pagineTutorial 5Nur Arisya AinaaNessuna valutazione finora

- Crochet PatternsDocumento25 pagineCrochet PatternsDoris LiNessuna valutazione finora

- CRL 0001 GDocumento6 pagineCRL 0001 GLuong LeNessuna valutazione finora

- 1.62 How To Handle Advance Purchase Bookings PDFDocumento1 pagina1.62 How To Handle Advance Purchase Bookings PDFsNessuna valutazione finora

- VISUALS IN ECONOMICS (Deped)Documento4 pagineVISUALS IN ECONOMICS (Deped)Ceres B. LuzarragaNessuna valutazione finora

- 1 Introduction To Cost AccountingDocumento3 pagine1 Introduction To Cost AccountingRonn Robby RosalesNessuna valutazione finora

- Customer Request Form (Front)Documento2 pagineCustomer Request Form (Front)noel bandaNessuna valutazione finora

- Ibuyan Joseph Me150-2 E02 Quiz5Documento30 pagineIbuyan Joseph Me150-2 E02 Quiz5joseph ibuyanNessuna valutazione finora

- Dependency Theory and The Latin American ExperienceDocumento2 pagineDependency Theory and The Latin American ExperienceKate Angellou Jawood100% (1)

- Utex Plunger PackingDocumento7 pagineUtex Plunger Packinganandkumar.mauryaNessuna valutazione finora

- Annexure-I Proforma of Application For Registration As A Political Party Under Section 29A of The Representation of The People Act, 1951Documento36 pagineAnnexure-I Proforma of Application For Registration As A Political Party Under Section 29A of The Representation of The People Act, 1951Ravi SharmaNessuna valutazione finora

- Peningkatan Kapasitas Pemerintahan Daerah Dalam Proses Masyarakat Ekonomi AseanDocumento8 paginePeningkatan Kapasitas Pemerintahan Daerah Dalam Proses Masyarakat Ekonomi AseanZex CeedNessuna valutazione finora

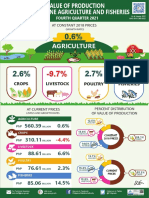

- Infographics, Value of Production in Philippine Agriculture and Fisheries, Fourth Quarter 2021Documento1 paginaInfographics, Value of Production in Philippine Agriculture and Fisheries, Fourth Quarter 2021Cart LaneNessuna valutazione finora

- Kunci JWB Soal B 2015 PDFDocumento29 pagineKunci JWB Soal B 2015 PDFAnisaa Okta100% (5)

- Fa1 1Documento2 pagineFa1 1RyanNessuna valutazione finora

- GHMC Property Tax PDFDocumento1 paginaGHMC Property Tax PDFSrinubabu MaddukuriNessuna valutazione finora

- 2 Cost Behavior 2 (20 Pages)Documento21 pagine2 Cost Behavior 2 (20 Pages)Raju RiadNessuna valutazione finora