Potrebbero piacerti anche

- Introduction to Negotiable Instruments: As per Indian LawsDa EverandIntroduction to Negotiable Instruments: As per Indian LawsValutazione: 5 su 5 stelle5/5 (1)

- Principles of Insurance Law with Case StudiesDa EverandPrinciples of Insurance Law with Case StudiesValutazione: 5 su 5 stelle5/5 (1)

- Contracts Mnemonics and Definitions: Mnemonics, #2Da EverandContracts Mnemonics and Definitions: Mnemonics, #2Nessuna valutazione finora

- Annexure - 2 COS 38 Joint Hindu Family LetterDocumento2 pagineAnnexure - 2 COS 38 Joint Hindu Family LetterRahul Kumar50% (2)

- Concepts and Kinds of Negotiable InstrumentsDocumento37 pagineConcepts and Kinds of Negotiable InstrumentsMohd YasinNessuna valutazione finora

- Funds Transfer Form - For Wholesale Banking Customers Only: Debit Account DetailsDocumento1 paginaFunds Transfer Form - For Wholesale Banking Customers Only: Debit Account Detailsdon EzeNessuna valutazione finora

- Gregory Feb 2020 Wells StatementDocumento4 pagineGregory Feb 2020 Wells StatementYoooNessuna valutazione finora

- PayPass - MChip Reader Card Application Interface Specification (V2.0)Documento80 paginePayPass - MChip Reader Card Application Interface Specification (V2.0)Kiran Kumar Kuppa100% (3)

- Col. House and The League of NationsDocumento5 pagineCol. House and The League of NationsSolomon Cosmin Ionut100% (1)

- Consumer Protection in India: A brief Guide on the Subject along with the Specimen form of a ComplaintDa EverandConsumer Protection in India: A brief Guide on the Subject along with the Specimen form of a ComplaintNessuna valutazione finora

- Contract of Sale of GoodsDocumento6 pagineContract of Sale of GoodsweygandtNessuna valutazione finora

- ERM Case Studies of an FMCG Company and a Multinational BankDocumento22 pagineERM Case Studies of an FMCG Company and a Multinational BankgordukhanNessuna valutazione finora

- Vdocuments - MX Btmm-Ebook PDFDocumento11 pagineVdocuments - MX Btmm-Ebook PDFmudey100% (1)

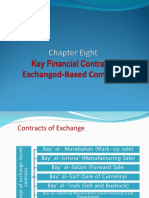

- Bay' Al-Istisna'Documento16 pagineBay' Al-Istisna'Mahyuddin Khalid100% (7)

- "Quasi-Contract": Law of Contracts-1Documento21 pagine"Quasi-Contract": Law of Contracts-1Muhammad MahatabNessuna valutazione finora

- Murabaha Facility AgreementDocumento18 pagineMurabaha Facility AgreementEthica Institute of Islamic Finance™Nessuna valutazione finora

- Sale of Goods Act 1930 ExplainedDocumento12 pagineSale of Goods Act 1930 Explainedhsha mo100% (2)

- Islamic Financial - Bai Al-IstinaDocumento18 pagineIslamic Financial - Bai Al-IstinaDaud Farook IINessuna valutazione finora

- Assignment IstisnaDocumento5 pagineAssignment IstisnaFarrah AinNessuna valutazione finora

- Accounting For Istisna and Parallel IstisnaDocumento6 pagineAccounting For Istisna and Parallel IstisnaSuazhari IbrahimNessuna valutazione finora

- Istisna' - Mira&nadDocumento11 pagineIstisna' - Mira&nadknadhirah100% (2)

- Islamic Mode of Finance IstisnaDocumento15 pagineIslamic Mode of Finance IstisnaMuhammad Asif100% (2)

- Islamic Banking 8552Documento16 pagineIslamic Banking 8552MAZHAR NISARNessuna valutazione finora

- Islamic Finance - Istisna, An OverviewDocumento10 pagineIslamic Finance - Istisna, An OverviewHussene Waziri حُسين وَزيريNessuna valutazione finora

- Shariah Opinion (Fatwa)Documento166 pagineShariah Opinion (Fatwa)Fa Omar SanyangNessuna valutazione finora

- Chapter 6 - Shariah Contract in Islamic FinanceDocumento25 pagineChapter 6 - Shariah Contract in Islamic FinanceNur Hasanah IsharNessuna valutazione finora

- Istisna': in Islamic Banking: Concept and ApplicationDocumento10 pagineIstisna': in Islamic Banking: Concept and ApplicationMr BalochNessuna valutazione finora

- Chapter 8Documento40 pagineChapter 8otaku himeNessuna valutazione finora

- Istisna in Islamic Banking Concept and Application (MS 99-108)Documento10 pagineIstisna in Islamic Banking Concept and Application (MS 99-108)johzyNessuna valutazione finora

- Istisna (Order Contract)Documento2 pagineIstisna (Order Contract)proffina786Nessuna valutazione finora

- Law of Contracts-II (Difference Between Sale and Agreement To Sell)Documento19 pagineLaw of Contracts-II (Difference Between Sale and Agreement To Sell)Namisha ChoudharyNessuna valutazione finora

- IstisnaaDocumento5 pagineIstisnaaOGETO WESLEYNessuna valutazione finora

- Sale of GoodsDocumento41 pagineSale of GoodsKellyNessuna valutazione finora

- Sale of Goods Act Full PPTsDocumento28 pagineSale of Goods Act Full PPTsDr. Manvinder Singh PahwaNessuna valutazione finora

- Contracts ProjectDocumento13 pagineContracts ProjectUdhithaa S K KotaNessuna valutazione finora

- Samad ContractDocumento11 pagineSamad ContractishankhaliqueNessuna valutazione finora

- Ijarah: Basic Rules of Ijarah/LeasingDocumento6 pagineIjarah: Basic Rules of Ijarah/Leasingali_zain_7Nessuna valutazione finora

- Samad ContractDocumento11 pagineSamad ContractishankhaliqueNessuna valutazione finora

- Consolidated Report 2FDocumento158 pagineConsolidated Report 2Fble maNessuna valutazione finora

- Group 1-Credit-Report-2fDocumento46 pagineGroup 1-Credit-Report-2fble maNessuna valutazione finora

- Legal Aspects of Business Master NotesDocumento44 pagineLegal Aspects of Business Master NotesJessica Terry75% (4)

- Uqud in Islamic Financial TransactionsDocumento40 pagineUqud in Islamic Financial Transactionsmohamed saidNessuna valutazione finora

- Legal Aspects ProjectDocumento18 pagineLegal Aspects ProjectakshayNessuna valutazione finora

- Consumer Protection & Sale of Goods Act 1930Documento76 pagineConsumer Protection & Sale of Goods Act 1930Aniket_Aroskar_1560Nessuna valutazione finora

- Philippines strengthens secured transactions frameworkDocumento45 paginePhilippines strengthens secured transactions frameworkAnton Ric Delos ReyesNessuna valutazione finora

- Sharvani Shukla: Start Download PDF NowDocumento9 pagineSharvani Shukla: Start Download PDF NowDasvinderSinghNessuna valutazione finora

- Welcome To Contract Law II: Law of Sale of Goods 1.1 (Definition & Formation)Documento50 pagineWelcome To Contract Law II: Law of Sale of Goods 1.1 (Definition & Formation)yashovardhan rathoreNessuna valutazione finora

- Understanding Istisna Contracts: Definition, Types, Conditions and MechanismDocumento9 pagineUnderstanding Istisna Contracts: Definition, Types, Conditions and MechanismgwegNessuna valutazione finora

- Defined Under Sec 4 (1) of The Sale of Goods Act, 1930. As Defined Under Sec 4 (2) of The Sale of Goods Act, 1930. As Defined Under Sec 5 (1) of The Sale of Goods Act, 1930Documento16 pagineDefined Under Sec 4 (1) of The Sale of Goods Act, 1930. As Defined Under Sec 4 (2) of The Sale of Goods Act, 1930. As Defined Under Sec 5 (1) of The Sale of Goods Act, 1930Anonymous naXzms1FNessuna valutazione finora

- Bba 4 Semester (Morning) SESSION 2014-2018 Submitted byDocumento11 pagineBba 4 Semester (Morning) SESSION 2014-2018 Submitted byAnonymous qBJv2A8RANessuna valutazione finora

- Ang Yu Asuncion V CADocumento12 pagineAng Yu Asuncion V CAAnne Mary Celine TumalaNessuna valutazione finora

- Consumer CreditDocumento5 pagineConsumer CreditAlaiza Joy V AlcazarNessuna valutazione finora

- A SalamDocumento3 pagineA Salamali_zain_7Nessuna valutazione finora

- Formation of Sale: Preparatory StageDocumento4 pagineFormation of Sale: Preparatory StageBrian PapellerasNessuna valutazione finora

- Exposé Sur Les Produits DérivésDocumento13 pagineExposé Sur Les Produits DérivésAnonymous mmbK7QLyhNessuna valutazione finora

- National Law Institute University: BhopalDocumento19 pagineNational Law Institute University: BhopalIbban JavidNessuna valutazione finora

- Agreemant Must Be LawfulDocumento12 pagineAgreemant Must Be LawfulMUNASHE KAZUWANessuna valutazione finora

- Contract Management - Emodule - BasicsDocumento12 pagineContract Management - Emodule - BasicsnagarajuNessuna valutazione finora

- Islamic Modes of FinancingDocumento38 pagineIslamic Modes of FinancingMuhammad Shahzeb KhanNessuna valutazione finora

- Free PDF Law of Contract & Specific Relief PDFDocumento39 pagineFree PDF Law of Contract & Specific Relief PDFDeenAurDnya with Rana Zeeshan Ali KhanNessuna valutazione finora

- Analysis of General Principles of Sale of Goods Law in BangladeshDocumento15 pagineAnalysis of General Principles of Sale of Goods Law in Bangladeshoni siddikNessuna valutazione finora

- Final FD ReportDocumento17 pagineFinal FD ReportKumar SunnyNessuna valutazione finora

- Unit 2 Sales of Goods ActDocumento30 pagineUnit 2 Sales of Goods ActrohanNessuna valutazione finora

- A Term Paper: Submitted To MST - RezwanakarimDocumento6 pagineA Term Paper: Submitted To MST - RezwanakarimMd. Abul Hossen MilonNessuna valutazione finora

- Chapter 5 PpleDocumento24 pagineChapter 5 PpleanisharoysamantNessuna valutazione finora

- Bai Salam, Bai Istisna and Bai Al-Inah (Yayasuha)Documento26 pagineBai Salam, Bai Istisna and Bai Al-Inah (Yayasuha)Nur NasuhaNessuna valutazione finora

- Statement PDFDocumento5 pagineStatement PDFmudeyNessuna valutazione finora

- Bias GameDocumento3 pagineBias GamemudeyNessuna valutazione finora

- Barclays ScansDocumento5 pagineBarclays ScansmudeyNessuna valutazione finora

- Day Balance Daily % Growth Daily Profit Goal TP: Necessary Lot Size Based On ONE Trade Per DayDocumento8 pagineDay Balance Daily % Growth Daily Profit Goal TP: Necessary Lot Size Based On ONE Trade Per DaymudeyNessuna valutazione finora

- TCM MGMT AgreementDocumento5 pagineTCM MGMT AgreementmudeyNessuna valutazione finora

- Day Balance Daily % Growth Daily Profit Goal TP: Necessary Lot Size Based On ONE Trade Per DayDocumento8 pagineDay Balance Daily % Growth Daily Profit Goal TP: Necessary Lot Size Based On ONE Trade Per DaymudeyNessuna valutazione finora

- Declaration in Support of Share Transfer PDFDocumento1 paginaDeclaration in Support of Share Transfer PDFmudeyNessuna valutazione finora

- Day Balance Daily % Growth Daily Profit Goal TP: Necessary Lot Size Based On ONE Trade Per DayDocumento8 pagineDay Balance Daily % Growth Daily Profit Goal TP: Necessary Lot Size Based On ONE Trade Per DaymudeyNessuna valutazione finora

- Day Balance Daily % Growth Daily Profit Goal TP: Necessary Lot Size Based On ONE Trade Per DayDocumento8 pagineDay Balance Daily % Growth Daily Profit Goal TP: Necessary Lot Size Based On ONE Trade Per DaymudeyNessuna valutazione finora

- HASSAN MOHAMED MUDEY - HD324COO559882015 FinalDocumento36 pagineHASSAN MOHAMED MUDEY - HD324COO559882015 FinalmudeyNessuna valutazione finora

- Bias GameDocumento3 pagineBias GamemudeyNessuna valutazione finora

- Ch4 2 Muhiim Ijems-V4i8p105Documento10 pagineCh4 2 Muhiim Ijems-V4i8p105mudeyNessuna valutazione finora

- Thesis Chapter One Mudey - Comment Corrections Dr. Wakesa - Doc Final DraftDocumento46 pagineThesis Chapter One Mudey - Comment Corrections Dr. Wakesa - Doc Final DraftmudeyNessuna valutazione finora

- Chapter One Corrected FardowsaDocumento4 pagineChapter One Corrected FardowsamudeyNessuna valutazione finora

- Wanjau - Factors Influencing Completion of Building Projects in Kenya, Ministry of Land, Housing and Urban Development PDFDocumento78 pagineWanjau - Factors Influencing Completion of Building Projects in Kenya, Ministry of Land, Housing and Urban Development PDFFarheen BanoNessuna valutazione finora

- Contracted Pelvis: Causes, Diagnosis and ManagementDocumento13 pagineContracted Pelvis: Causes, Diagnosis and ManagementCuteness Romney100% (1)

- Wanjau - Factors Influencing Completion of Building Projects in Kenya, Ministry of Land, Housing and Urban DevelopmentDocumento104 pagineWanjau - Factors Influencing Completion of Building Projects in Kenya, Ministry of Land, Housing and Urban DevelopmentmudeyNessuna valutazione finora

- ApplicationevaDocumento2 pagineApplicationevamudeyNessuna valutazione finora

- MODULE 4: Obstetrics and Gynecology Topic 5Documento33 pagineMODULE 4: Obstetrics and Gynecology Topic 5mudeyNessuna valutazione finora

- Examination Questions 2016Documento9 pagineExamination Questions 2016mudeyNessuna valutazione finora

- AgeDocumento7 pagineAgemudeyNessuna valutazione finora

- CHAPTER ONE Nutritional Status Among Elementary School in Heliwa DistinctDocumento6 pagineCHAPTER ONE Nutritional Status Among Elementary School in Heliwa Distinctmudey100% (1)

- Contractedpelvis 111008054821 Phpapp01Documento15 pagineContractedpelvis 111008054821 Phpapp01Baldeep GrewalNessuna valutazione finora

- Chapter 1 Draft 2Documento5 pagineChapter 1 Draft 2mudeyNessuna valutazione finora

- Duties and ResponsibilitiesDocumento3 pagineDuties and ResponsibilitiesmudeyNessuna valutazione finora

- Narrow Pelvis. Anomalies of Position and Fetal Presentation. Pregnancy and Childbirth During Pelvic Presentation.Documento18 pagineNarrow Pelvis. Anomalies of Position and Fetal Presentation. Pregnancy and Childbirth During Pelvic Presentation.mudeyNessuna valutazione finora

- Aml and OfacDocumento1 paginaAml and OfacmudeyNessuna valutazione finora

- Related WordDocumento118 pagineRelated WordmudeyNessuna valutazione finora

- Letter of Confirmation LetterDocumento1 paginaLetter of Confirmation LettermudeyNessuna valutazione finora

- Cardiff Cash Management V2.0Documento108 pagineCardiff Cash Management V2.0elsa7er2000Nessuna valutazione finora

- Multination Finance Butler 5th EditionDocumento3 pagineMultination Finance Butler 5th EditionUnostudent2014Nessuna valutazione finora

- 09304079.pdf New Foreign PDFDocumento44 pagine09304079.pdf New Foreign PDFJannatul FerdousNessuna valutazione finora

- Financial InclusionDocumento6 pagineFinancial InclusionsignNessuna valutazione finora

- Chap 009Documento19 pagineChap 009van tinh khucNessuna valutazione finora

- Salary CalculatorDocumento19 pagineSalary Calculatorvirag_shahsNessuna valutazione finora

- Topic 5 Working Capital and Current Asset ManagementDocumento65 pagineTopic 5 Working Capital and Current Asset ManagementbriogeliqueNessuna valutazione finora

- Financial Accounting AssignmentDocumento15 pagineFinancial Accounting AssignmentEdward MtethiwaNessuna valutazione finora

- CompendiumDocumento18 pagineCompendiumpranithroyNessuna valutazione finora

- Tianjin PlasticsDocumento9 pagineTianjin PlasticsmalikatjuhNessuna valutazione finora

- Banking Sector Overview: Definitions, Regulation, FunctionsDocumento39 pagineBanking Sector Overview: Definitions, Regulation, FunctionsDieu NguyenNessuna valutazione finora

- Comparison of loan and deposit schemes of Indian Overseas Bank and Development Credit Bank of IndiaDocumento13 pagineComparison of loan and deposit schemes of Indian Overseas Bank and Development Credit Bank of IndiaKaran GujralNessuna valutazione finora

- RecoveriesDocumento45 pagineRecoveriesSona ElvisNessuna valutazione finora

- Basel NormsDocumento23 pagineBasel NormsPranu PranuNessuna valutazione finora

- Balancing Design Costs in EPC Projects: In-Office Design vs. The Site Engineering AdjustmentsDocumento5 pagineBalancing Design Costs in EPC Projects: In-Office Design vs. The Site Engineering AdjustmentsLik Dan FongNessuna valutazione finora

- Ibps RRB Po 2017 Capsule by Gopal Sir NewDocumento83 pagineIbps RRB Po 2017 Capsule by Gopal Sir NewPraveen ChaudharyNessuna valutazione finora

- Annual Report 2017Documento400 pagineAnnual Report 2017Md. Tareq Aziz100% (1)

- Statement DEC2022 265757521Documento6 pagineStatement DEC2022 265757521Ranjit LengureNessuna valutazione finora

- CF Chapter 4Documento25 pagineCF Chapter 4ASHWIN MOHANTYNessuna valutazione finora

- Australian Visa Subclass 600 - Tourist - Stream - Checklist - June - 2018Documento2 pagineAustralian Visa Subclass 600 - Tourist - Stream - Checklist - June - 2018Ronald King BernalNessuna valutazione finora

- ABU ROAD SHOE MARKET SANJAY PLACE ACCOUNTANTS LISTDocumento209 pagineABU ROAD SHOE MARKET SANJAY PLACE ACCOUNTANTS LISTDev SharmaNessuna valutazione finora

- E-Banking and Customer Satisfaction in BangladeshDocumento9 pagineE-Banking and Customer Satisfaction in BangladeshlamizaNessuna valutazione finora

- Indian Institute of Banking & FinanceDocumento8 pagineIndian Institute of Banking & FinanceAnonymous QqGiVVKwDGNessuna valutazione finora

- TN Comptroller's Report: Volunteer Energy CooperativeDocumento6 pagineTN Comptroller's Report: Volunteer Energy CooperativeDan LehrNessuna valutazione finora