Potrebbero piacerti anche

- IEA Report 13th DecemberDocumento23 pagineIEA Report 13th DecembernarnoliaNessuna valutazione finora

- IEA Report: 7th Dec, 2016Documento19 pagineIEA Report: 7th Dec, 2016narnoliaNessuna valutazione finora

- IEA Report 31st JanuaryDocumento24 pagineIEA Report 31st JanuarynarnoliaNessuna valutazione finora

- IEA Report 21st DecemberDocumento21 pagineIEA Report 21st DecembernarnoliaNessuna valutazione finora

- India Equity Analytics Today: Hold Rating On Prestige Estates StockDocumento25 pagineIndia Equity Analytics Today: Hold Rating On Prestige Estates StockNarnolia Securities LimitedNessuna valutazione finora

- Investment Funds Advisory For Today: Buy Stock of Powergrid and IFGL Refractories LTDDocumento23 pagineInvestment Funds Advisory For Today: Buy Stock of Powergrid and IFGL Refractories LTDNarnolia Securities LimitedNessuna valutazione finora

- IEA Report 10th May 2017Documento28 pagineIEA Report 10th May 2017narnoliaNessuna valutazione finora

- Stock Advisory For Today - But Stock of Coal India LTD and Cipla LimitedDocumento24 pagineStock Advisory For Today - But Stock of Coal India LTD and Cipla LimitedNarnolia Securities LimitedNessuna valutazione finora

- IEA Report 19th JanuaryDocumento28 pagineIEA Report 19th JanuarynarnoliaNessuna valutazione finora

- IEA Report 22th DecemberDocumento21 pagineIEA Report 22th DecembernarnoliaNessuna valutazione finora

- IEA Report 23rd DecemberDocumento24 pagineIEA Report 23rd DecembernarnoliaNessuna valutazione finora

- India Equity Analytics Today: Buy Stock of KPIT TechDocumento24 pagineIndia Equity Analytics Today: Buy Stock of KPIT TechNarnolia Securities LimitedNessuna valutazione finora

- As Slower Economic Growth Narnolia Securities Limited Recommended Buy Stock of Bank of IndiaDocumento20 pagineAs Slower Economic Growth Narnolia Securities Limited Recommended Buy Stock of Bank of IndiaNarnolia Securities LimitedNessuna valutazione finora

- Indian Equity Market Capitalization Today - Buy Stocks of Emami LTD With Target Price Rs 635.Documento21 pagineIndian Equity Market Capitalization Today - Buy Stocks of Emami LTD With Target Price Rs 635.Narnolia Securities LimitedNessuna valutazione finora

- India Equity Analytics For Today - Buy Stocks of CMC With Target Price From Rs 1490 To Rs 1690.Documento23 pagineIndia Equity Analytics For Today - Buy Stocks of CMC With Target Price From Rs 1490 To Rs 1690.Narnolia Securities LimitedNessuna valutazione finora

- Stock Market Today Tips - Book Profit On The Stock CMCDocumento21 pagineStock Market Today Tips - Book Profit On The Stock CMCNarnolia Securities LimitedNessuna valutazione finora

- 10 MidcapsDocumento1 pagina10 MidcapspuneetdubeyNessuna valutazione finora

- IEA Report: 23rd January, 2017Documento27 pagineIEA Report: 23rd January, 2017narnoliaNessuna valutazione finora

- Quick Note: Sintex IndustriesDocumento6 pagineQuick Note: Sintex Industriesred cornerNessuna valutazione finora

- IEA Report 18th JanuaryDocumento25 pagineIEA Report 18th JanuarynarnoliaNessuna valutazione finora

- Stock Investment Tips Recommendation - Buy Stocks of Shree Cement With Target Price Rs.4791Documento20 pagineStock Investment Tips Recommendation - Buy Stocks of Shree Cement With Target Price Rs.4791Narnolia Securities LimitedNessuna valutazione finora

- BIMBSec - Dialog Company Update - Higher and Deeper - 20120625Documento2 pagineBIMBSec - Dialog Company Update - Higher and Deeper - 20120625Bimb SecNessuna valutazione finora

- Sharekhan Top Picks: Absolute Returns (Top Picks Vs Benchmark Indices) % Sharekhan Sensex Nifty CNX (Top Picks) Mid-CapDocumento7 pagineSharekhan Top Picks: Absolute Returns (Top Picks Vs Benchmark Indices) % Sharekhan Sensex Nifty CNX (Top Picks) Mid-CapRajesh KarriNessuna valutazione finora

- IEA Report 17th JanuaryDocumento28 pagineIEA Report 17th JanuarynarnoliaNessuna valutazione finora

- India Equity Analytics For Today - Buy Stocks of Infosys With A Price Target of Rs 3620Documento20 pagineIndia Equity Analytics For Today - Buy Stocks of Infosys With A Price Target of Rs 3620Narnolia Securities LimitedNessuna valutazione finora

- 4QFY14E Results Preview: Institutional ResearchDocumento22 pagine4QFY14E Results Preview: Institutional ResearchGunjan ShethNessuna valutazione finora

- La Opala RG - Initiating Coverage - Centrum 30062014Documento21 pagineLa Opala RG - Initiating Coverage - Centrum 30062014Jeevan PatwaNessuna valutazione finora

- Gulf Oil Lubricants: Melting Crude Puts It in A Sweet SpotDocumento2 pagineGulf Oil Lubricants: Melting Crude Puts It in A Sweet SpotsanjeevpandaNessuna valutazione finora

- Top Recommendation - 140911Documento51 pagineTop Recommendation - 140911chaltrikNessuna valutazione finora

- Market Outlook Market Outlook: Dealer's DiaryDocumento13 pagineMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNessuna valutazione finora

- Top Picks: Research TeamDocumento30 pagineTop Picks: Research Team3bandhuNessuna valutazione finora

- BIMBSec - Bumi Armada Company Update - Deeper Into Caspian Sea - 20120417Documento2 pagineBIMBSec - Bumi Armada Company Update - Deeper Into Caspian Sea - 20120417Bimb SecNessuna valutazione finora

- IEA Report 18th May 2017Documento26 pagineIEA Report 18th May 2017narnoliaNessuna valutazione finora

- Sharekhan Top Picks: CMP As On September 01, 2014 Under ReviewDocumento7 pagineSharekhan Top Picks: CMP As On September 01, 2014 Under Reviewrohitkhanna1180Nessuna valutazione finora

- HSBC Report On Two-Wheeler IndustryDocumento64 pagineHSBC Report On Two-Wheeler Industrymanishsharma33Nessuna valutazione finora

- APOLLO TYREs 26032012100430Documento2 pagineAPOLLO TYREs 26032012100430After Burn FirebrowlNessuna valutazione finora

- Stock Update Wonderla Holidays Viewpoint Zee Learn: IndexDocumento4 pagineStock Update Wonderla Holidays Viewpoint Zee Learn: IndexRajasekhar Reddy AnekalluNessuna valutazione finora

- Sharekhan Top Picks: October 26, 2012Documento7 pagineSharekhan Top Picks: October 26, 2012Soumik DasNessuna valutazione finora

- IEA Report 27th April 2017Documento30 pagineIEA Report 27th April 2017narnoliaNessuna valutazione finora

- 2013-04-08 CORD - Si (Phillip Secur) Cordlife - Strong FCF Generation at A Reasonable PriceDocumento21 pagine2013-04-08 CORD - Si (Phillip Secur) Cordlife - Strong FCF Generation at A Reasonable PriceKelvin FuNessuna valutazione finora

- Nivesh Stock PicksDocumento13 pagineNivesh Stock PicksAnonymous W7lVR9qs25Nessuna valutazione finora

- India Equity Analytics For Today - Buy Stocks of Reliance Industries Limited With Target Price Rs 1040Documento20 pagineIndia Equity Analytics For Today - Buy Stocks of Reliance Industries Limited With Target Price Rs 1040Narnolia Securities LimitedNessuna valutazione finora

- Ashiana Crisil PDFDocumento22 pagineAshiana Crisil PDFJaimin ShahNessuna valutazione finora

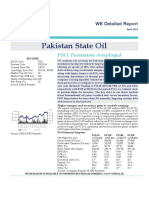

- PSO Detailed Report 2Documento9 paginePSO Detailed Report 2Javaid IqbalNessuna valutazione finora

- KPIT 2QFY16 Outlook ReviewDocumento5 pagineKPIT 2QFY16 Outlook ReviewgirishrajsNessuna valutazione finora

- Top 10 Mid-Cap Ideas: Find Below Our Top Mid Cap Buys and The Rationale For The SameDocumento4 pagineTop 10 Mid-Cap Ideas: Find Below Our Top Mid Cap Buys and The Rationale For The Sameapi-234474152Nessuna valutazione finora

- Corp LTD: (GMDV)Documento3 pagineCorp LTD: (GMDV)api-234474152Nessuna valutazione finora

- Selan Exploration TechnologyDocumento3 pagineSelan Exploration TechnologyPaul GeorgeNessuna valutazione finora

- Sharekhan Top PicksDocumento7 pagineSharekhan Top PicksLaharii MerugumallaNessuna valutazione finora

- Name - Ashu Sharma Class/Section - UID - 19BBA1299: Analysis of Prime Securities LTDDocumento14 pagineName - Ashu Sharma Class/Section - UID - 19BBA1299: Analysis of Prime Securities LTDKartik GuleriaNessuna valutazione finora

- Pakistan State Oil: SecuritiesDocumento16 paginePakistan State Oil: SecuritiesAmmad SheikhNessuna valutazione finora

- First Source Solutions LTD - Karvy Recommendation 11 Mar 2016Documento5 pagineFirst Source Solutions LTD - Karvy Recommendation 11 Mar 2016AdityaKumarNessuna valutazione finora

- JMV PreferredDocumento25 pagineJMV PreferredAnonymous W7lVR9qs25Nessuna valutazione finora

- Ten Baggers Portfolio AmbitDocumento18 pagineTen Baggers Portfolio AmbitPuneet367Nessuna valutazione finora

- Best Performing Stock Advice For Today - Neutral Rating On GAIL Stock With A Target Price of Rs.346Documento22 pagineBest Performing Stock Advice For Today - Neutral Rating On GAIL Stock With A Target Price of Rs.346Narnolia Securities LimitedNessuna valutazione finora

- Top Picks: Research TeamDocumento30 pagineTop Picks: Research TeamPooja AgarwalNessuna valutazione finora

- Name - Anup Sharma UID - 19BBA1299: Analysis of Prime Securities LTDDocumento14 pagineName - Anup Sharma UID - 19BBA1299: Analysis of Prime Securities LTDKartik GuleriaNessuna valutazione finora

- IEA Report 27th MarchDocumento24 pagineIEA Report 27th MarchnarnoliaNessuna valutazione finora

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryDa EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNessuna valutazione finora

- IEA Report 10th May 2017Documento28 pagineIEA Report 10th May 2017narnoliaNessuna valutazione finora

- IEA Report 18th May 2017Documento26 pagineIEA Report 18th May 2017narnoliaNessuna valutazione finora

- IEA Report 4th May 2017Documento25 pagineIEA Report 4th May 2017narnoliaNessuna valutazione finora

- IEA Report 26th April 2017Documento33 pagineIEA Report 26th April 2017narnoliaNessuna valutazione finora

- IEA Report 25th April 2017Documento37 pagineIEA Report 25th April 2017narnoliaNessuna valutazione finora

- IEA Report 27th April 2017Documento30 pagineIEA Report 27th April 2017narnoliaNessuna valutazione finora

- IEA Report 24th April 2017Documento35 pagineIEA Report 24th April 2017narnoliaNessuna valutazione finora

- IEA Report 20th April 2017Documento30 pagineIEA Report 20th April 2017narnoliaNessuna valutazione finora

- IEA Report 21st April 2017Documento35 pagineIEA Report 21st April 2017narnoliaNessuna valutazione finora

- TQU 21st April 2017Documento12 pagineTQU 21st April 2017narnoliaNessuna valutazione finora

- TQU 19th April 2017Documento19 pagineTQU 19th April 2017narnoliaNessuna valutazione finora

- TQU 20th April 2017Documento12 pagineTQU 20th April 2017narnoliaNessuna valutazione finora

- Process Costing Exercises Series 1Documento23 pagineProcess Costing Exercises Series 1sarahbeeNessuna valutazione finora

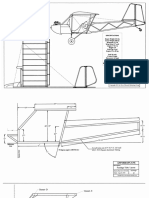

- Flight Vehicle Design:: Example 2 (Uav)Documento43 pagineFlight Vehicle Design:: Example 2 (Uav)Anmol KumarNessuna valutazione finora

- Plans PDFDocumento49 paginePlans PDFEstevam Gomes de Azevedo85% (34)

- Bulacan Agricultural State College: Lesson Plan in Science 4 Life Cycle of Humans, Animals and PlantsDocumento6 pagineBulacan Agricultural State College: Lesson Plan in Science 4 Life Cycle of Humans, Animals and PlantsHarmonica PellazarNessuna valutazione finora

- Math COT 3Documento18 pagineMath COT 3Icy Mae SenadosNessuna valutazione finora

- Biophoton RevolutionDocumento3 pagineBiophoton RevolutionVyavasayaha Anita BusicNessuna valutazione finora

- PIX4D Simply PowerfulDocumento43 paginePIX4D Simply PowerfulJUAN BAQUERONessuna valutazione finora

- LET General Math ReviewerDocumento7 pagineLET General Math ReviewerMarco Rhonel Eusebio100% (1)

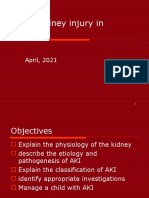

- AKI in ChildrenDocumento43 pagineAKI in ChildrenYonas AwgichewNessuna valutazione finora

- Bảng giá FLUKEDocumento18 pagineBảng giá FLUKEVăn Long NguyênNessuna valutazione finora

- Food Taste Panel Evaluation Form 2Documento17 pagineFood Taste Panel Evaluation Form 2Akshat JainNessuna valutazione finora

- Tugas Dikumpulkan Pada Hari Sabtu, 11 April 2020. Apabila Email Bermasalah Dapat Mengirimkan Via WA PribadiDocumento4 pagineTugas Dikumpulkan Pada Hari Sabtu, 11 April 2020. Apabila Email Bermasalah Dapat Mengirimkan Via WA PribadiFebry SugiantaraNessuna valutazione finora

- IV. Network Modeling, Simple SystemDocumento16 pagineIV. Network Modeling, Simple SystemJaya BayuNessuna valutazione finora

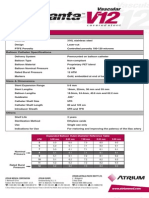

- Advanta V12 Data SheetDocumento2 pagineAdvanta V12 Data SheetJuliana MiyagiNessuna valutazione finora

- Nivel VV-VW Board User Guide enDocumento5 pagineNivel VV-VW Board User Guide enHarveyWishtartNessuna valutazione finora

- Paediatric Intake Form Modern OT 2018Documento6 paginePaediatric Intake Form Modern OT 2018SefNessuna valutazione finora

- Bible World History Timeline - 4004-3004BCDocumento1 paginaBible World History Timeline - 4004-3004BCSagitonette DadapNessuna valutazione finora

- Electric ScootorDocumento40 pagineElectric Scootor01fe19bme079Nessuna valutazione finora

- Release From Destructive Covenants - D. K. OlukoyaDocumento178 pagineRelease From Destructive Covenants - D. K. OlukoyaJemima Manzo100% (1)

- 4 Force & ExtensionDocumento13 pagine4 Force & ExtensionSelwah Hj AkipNessuna valutazione finora

- Catalogo Aesculap PDFDocumento16 pagineCatalogo Aesculap PDFHansNessuna valutazione finora

- JC Series Jaw Crusher PDFDocumento8 pagineJC Series Jaw Crusher PDFgarrybieber100% (1)

- Halfen Cast-In Channels: HTA-CE 50/30P HTA-CE 40/22PDocumento92 pagineHalfen Cast-In Channels: HTA-CE 50/30P HTA-CE 40/22PTulusNessuna valutazione finora

- Ali Erdemir: Professional ExperienceDocumento3 pagineAli Erdemir: Professional ExperienceDunkMeNessuna valutazione finora

- Murata High Voltage CeramicDocumento38 pagineMurata High Voltage CeramictycristinaNessuna valutazione finora

- Percent by VolumeDocumento19 paginePercent by VolumeSabrina LavegaNessuna valutazione finora

- 2015 Nos-Dcp National Oil Spill Disaster Contingency PlanDocumento62 pagine2015 Nos-Dcp National Oil Spill Disaster Contingency PlanVaishnavi Jayakumar100% (1)

- Crouse Hinds XPL Led BrochureDocumento12 pagineCrouse Hinds XPL Led BrochureBrayan Galaz BelmarNessuna valutazione finora

- Soldier of Fortune PDFDocumento208 pagineSoldier of Fortune PDFNixel SpielNessuna valutazione finora

- Better - Homes.and - Gardens.usa - TruePDF December.2018Documento136 pagineBetter - Homes.and - Gardens.usa - TruePDF December.2018MadaMadutsaNessuna valutazione finora