Potrebbero piacerti anche

- Corporate Finance - Hill Country Snack FoodDocumento11 pagineCorporate Finance - Hill Country Snack FoodNell MizunoNessuna valutazione finora

- Hill Country Snack Foods Case AnalysisDocumento5 pagineHill Country Snack Foods Case Analysisdivakar62Nessuna valutazione finora

- Hill Country Snack Foods CoDocumento1 paginaHill Country Snack Foods CoKriti AhujaNessuna valutazione finora

- Hill Country CaseDocumento5 pagineHill Country CaseDeepansh Kakkar100% (1)

- Case Study - Hill Country Snack Foods Co.Documento2 pagineCase Study - Hill Country Snack Foods Co.Spencer123455678967% (3)

- Hill Country Snack Food Co.Documento7 pagineHill Country Snack Food Co.Anish NarulaNessuna valutazione finora

- Case Study - Hill Country Snack Foods Co.Documento4 pagineCase Study - Hill Country Snack Foods Co.Saurabh Agarwal0% (1)

- Case Study: Hill Country Snack Foods " HCSF " (With Soluion )Documento12 pagineCase Study: Hill Country Snack Foods " HCSF " (With Soluion )Kamran Shabbir50% (2)

- Hill CountryDocumento8 pagineHill CountryAtif Raza AkbarNessuna valutazione finora

- Hill Country Snack Foods Co - UDocumento4 pagineHill Country Snack Foods Co - Unipun9143Nessuna valutazione finora

- Hill Country Snack Foods Co - UDocumento4 pagineHill Country Snack Foods Co - Unipun9143Nessuna valutazione finora

- Hill Country Solution ExcelDocumento1 paginaHill Country Solution Excelankujai88Nessuna valutazione finora

- New Heritage Doll CompanyDocumento5 pagineNew Heritage Doll CompanyRahul LalwaniNessuna valutazione finora

- Case Study Q4 - Hill Country Snack FoodsDocumento2 pagineCase Study Q4 - Hill Country Snack FoodsSpencer1234556789Nessuna valutazione finora

- Case 26 Assignment AnalysisDocumento1 paginaCase 26 Assignment AnalysisNiyanthesh Reddy50% (2)

- MEG CV 2 CaseDocumento10 pagineMEG CV 2 Casegabal_m50% (2)

- Midland Energy Group A5Documento3 pagineMidland Energy Group A5Deepesh Moolchandani0% (1)

- LinearDocumento6 pagineLinearjackedup211Nessuna valutazione finora

- Hill Country Snack Foods CompanyDocumento14 pagineHill Country Snack Foods CompanyVeni GuptaNessuna valutazione finora

- Continental CarriersDocumento10 pagineContinental Carriersnipun9143Nessuna valutazione finora

- BBBY Case ExerciseDocumento7 pagineBBBY Case ExerciseSue McGinnisNessuna valutazione finora

- This Study Resource Was: 1 Hill Country Snack Foods CoDocumento9 pagineThis Study Resource Was: 1 Hill Country Snack Foods CoPavithra TamilNessuna valutazione finora

- Winfield CaseDocumento8 pagineWinfield CaseAbhinandan Singh67% (3)

- DeluxeDocumento4 pagineDeluxeshielamaeNessuna valutazione finora

- Buffet Bid For Media GeneralDocumento21 pagineBuffet Bid For Media GeneralDahagam Saumith100% (1)

- Bidding On The Yell Group - Prasann S - 2015PGP334Documento3 pagineBidding On The Yell Group - Prasann S - 2015PGP334Prasann ShahNessuna valutazione finora

- Session 19 - Dividend Policy at Linear TechDocumento2 pagineSession 19 - Dividend Policy at Linear TechRichBrook7Nessuna valutazione finora

- American Home Products Corporation CaseDocumento3 pagineAmerican Home Products Corporation CaseSatish Dabhade100% (1)

- Case AnalysisDocumento11 pagineCase AnalysisSagar Bansal50% (2)

- Midland Energy ReportDocumento13 pagineMidland Energy Reportkiller dramaNessuna valutazione finora

- Loewen Group CaseDocumento2 pagineLoewen Group CaseSu_NeilNessuna valutazione finora

- Sealed Air Corporation's Leveraged Recapitalization (A)Documento7 pagineSealed Air Corporation's Leveraged Recapitalization (A)Jyoti GuptaNessuna valutazione finora

- Midland CaseDocumento5 pagineMidland CaseJessica Bill100% (3)

- Monmouth CaseDocumento6 pagineMonmouth CaseMohammed Akhtab Ul HudaNessuna valutazione finora

- Friendly CS SolutionDocumento8 pagineFriendly CS SolutionEfendiNessuna valutazione finora

- American Chemical CorporationDocumento8 pagineAmerican Chemical CorporationAnastasiaNessuna valutazione finora

- Case 3: Rockboro Machine Tools Corporation Executive SummaryDocumento1 paginaCase 3: Rockboro Machine Tools Corporation Executive SummaryMaricel GuarinoNessuna valutazione finora

- Boeing 777Documento5 pagineBoeing 777Tanvir Ahmed100% (1)

- Jones Electrical DistributionDocumento5 pagineJones Electrical DistributionAsif AliNessuna valutazione finora

- Scott & Sons Company Case Solution From Syndicate 3Documento3 pagineScott & Sons Company Case Solution From Syndicate 3Murni Fitri FatimahNessuna valutazione finora

- Hill Country Snack Foods CoDocumento9 pagineHill Country Snack Foods CoZjiajiajiajiaPNessuna valutazione finora

- American Home Products CorporationDocumento7 pagineAmerican Home Products Corporationpancaspe100% (2)

- 2839 MEG CV 2 CaseDocumento10 pagine2839 MEG CV 2 CasegueigunNessuna valutazione finora

- Infineon Technologies Case FMDocumento7 pagineInfineon Technologies Case FMArjit Gupta100% (2)

- Winfield ManagementDocumento5 pagineWinfield Managementmadhav1111Nessuna valutazione finora

- Sealed Air Co Case Study Queestions Why Did Sealed Air Undertake A LeveragDocumento9 pagineSealed Air Co Case Study Queestions Why Did Sealed Air Undertake A Leveragvichenyu100% (1)

- Destin Brass Case Study SolutionDocumento5 pagineDestin Brass Case Study SolutionAmruta Turmé100% (2)

- Jones Electrical DistributionDocumento4 pagineJones Electrical Distributioncagc333Nessuna valutazione finora

- Midland WACCDocumento2 pagineMidland WACCDeniz Minican100% (3)

- Midland Energy ResourcesDocumento21 pagineMidland Energy ResourcesSavageNessuna valutazione finora

- Sealed AirDocumento10 pagineSealed AirHimanshu KumarNessuna valutazione finora

- Questions:: 1. Is Mercury An Appropriate Target For AGI? Why or Why Not?Documento5 pagineQuestions:: 1. Is Mercury An Appropriate Target For AGI? Why or Why Not?Cuong NguyenNessuna valutazione finora

- MidlandDocumento9 pagineMidlandvenom_ftw100% (1)

- CH 6 Model 14 Free Cash Flow CalculationDocumento12 pagineCH 6 Model 14 Free Cash Flow CalculationrealitNessuna valutazione finora

- Assumptions For Forecasting Model: Income StatementDocumento9 pagineAssumptions For Forecasting Model: Income StatementRadhika SarawagiNessuna valutazione finora

- Class Exercise Fashion Company Three Statements Model - CompletedDocumento16 pagineClass Exercise Fashion Company Three Statements Model - CompletedbobNessuna valutazione finora

- Financial Statements Analysis Case StudyDocumento15 pagineFinancial Statements Analysis Case StudyNelly Yulinda50% (2)

- Financial Statements Analysis Case StudyDocumento15 pagineFinancial Statements Analysis Case Studyดวงยี่หวา จิระวงศ์สันติสุขNessuna valutazione finora

- 10408065Documento4 pagine10408065Joel Christian MascariñaNessuna valutazione finora

- Amazon ValuationDocumento22 pagineAmazon ValuationDr Sakshi SharmaNessuna valutazione finora

- Nedbank Case Study - FinalDocumento2 pagineNedbank Case Study - Finalkiller dramaNessuna valutazione finora

- Key Takeaways From E&Y WebinarDocumento2 pagineKey Takeaways From E&Y Webinarkiller dramaNessuna valutazione finora

- PAnelDocumento11 paginePAnelkiller dramaNessuna valutazione finora

- Combined SPSS in Excel 456Documento89 pagineCombined SPSS in Excel 456killer dramaNessuna valutazione finora

- SDDocumento1 paginaSDkiller dramaNessuna valutazione finora

- Looper Height TagsDocumento1 paginaLooper Height Tagskiller dramaNessuna valutazione finora

- 1.1. Brief of The CaseDocumento6 pagine1.1. Brief of The Casekiller dramaNessuna valutazione finora

- Oep SCMP A5 Minibrochure WebDocumento8 pagineOep SCMP A5 Minibrochure Webkiller dramaNessuna valutazione finora

- Ucalgary 2013 Kano LienaDocumento349 pagineUcalgary 2013 Kano Lienakiller dramaNessuna valutazione finora

- Paper More-Excel SheetDocumento133 paginePaper More-Excel Sheetkiller dramaNessuna valutazione finora

- Scale For EFA For Resilience ModelDocumento9 pagineScale For EFA For Resilience Modelkiller dramaNessuna valutazione finora

- Reliance Trend Store ProjectDocumento9 pagineReliance Trend Store Projectkiller dramaNessuna valutazione finora

- Research Papers Ref 30th JanDocumento33 pagineResearch Papers Ref 30th Jankiller dramaNessuna valutazione finora

- Specification For - OGPCS008 (Online Grading System)Documento1 paginaSpecification For - OGPCS008 (Online Grading System)killer dramaNessuna valutazione finora

- Doe PracticeDocumento237 pagineDoe Practicekiller dramaNessuna valutazione finora

- Syntax GG PlotDocumento3 pagineSyntax GG Plotkiller dramaNessuna valutazione finora

- Boeing 777 ADocumento3 pagineBoeing 777 Akiller dramaNessuna valutazione finora

- Manual For Building ANP Decision ModelsDocumento84 pagineManual For Building ANP Decision Modelskiller dramaNessuna valutazione finora

- Type I and Type II Errror in ACCDocumento3 pagineType I and Type II Errror in ACCkiller dramaNessuna valutazione finora

- Macro Note BookDocumento56 pagineMacro Note Bookkiller dramaNessuna valutazione finora

- Executive Summary:: Sl. No. Areas Implications Under GSTDocumento2 pagineExecutive Summary:: Sl. No. Areas Implications Under GSTkiller dramaNessuna valutazione finora

- Zonal Grievance Redressal Officers: Zone States Covered Name & Designation Email Id Tel No. With STD CodeDocumento1 paginaZonal Grievance Redressal Officers: Zone States Covered Name & Designation Email Id Tel No. With STD Codekiller dramaNessuna valutazione finora

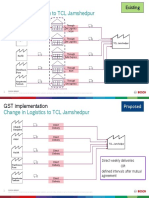

- Annexure 2 - Change in Logistics To TCL JamshedpurDocumento2 pagineAnnexure 2 - Change in Logistics To TCL Jamshedpurkiller dramaNessuna valutazione finora

- Case Study: Incomplete SolutionsDocumento6 pagineCase Study: Incomplete Solutionskiller dramaNessuna valutazione finora

- Sqms QueryDocumento2 pagineSqms Querykiller dramaNessuna valutazione finora

- What Is The Difference Between Tier 1 Capital and Tier 2 Capital - InvestopediaDocumento6 pagineWhat Is The Difference Between Tier 1 Capital and Tier 2 Capital - Investopediakiller dramaNessuna valutazione finora

- Mo Os Best Post GST PDFDocumento60 pagineMo Os Best Post GST PDFkiller dramaNessuna valutazione finora

- Advertising & Sales Promotion: Salesforce & Channel Distribution AssignmentDocumento6 pagineAdvertising & Sales Promotion: Salesforce & Channel Distribution Assignmentkiller dramaNessuna valutazione finora

- Sgco GST PPT 2017Documento46 pagineSgco GST PPT 2017killer dramaNessuna valutazione finora

- PH Case Mexico BOPDocumento6 paginePH Case Mexico BOPkiller dramaNessuna valutazione finora

- Boge FLEX PET SystemsDocumento4 pagineBoge FLEX PET SystemsAir Repair, LLCNessuna valutazione finora

- Textile Reinforced - Cold Splice - Final 14 MRCH 2018Documento25 pagineTextile Reinforced - Cold Splice - Final 14 MRCH 2018Shariq KhanNessuna valutazione finora

- LNG Simulation PDFDocumento28 pagineLNG Simulation PDFRobert WatersNessuna valutazione finora

- Energies: Numerical Simulations On The Application of A Closed-Loop Lake Water Heat Pump System in The Lake Soyang, KoreaDocumento16 pagineEnergies: Numerical Simulations On The Application of A Closed-Loop Lake Water Heat Pump System in The Lake Soyang, KoreaMvikeli DlaminiNessuna valutazione finora

- Retrenchment in Malaysia Employers Right PDFDocumento8 pagineRetrenchment in Malaysia Employers Right PDFJeifan-Ira DizonNessuna valutazione finora

- EarthmattersDocumento7 pagineEarthmattersfeafvaevsNessuna valutazione finora

- Neurovascular Assessment PDFDocumento5 pagineNeurovascular Assessment PDFNasrullah UllahNessuna valutazione finora

- Medicina 57 00032 (01 14)Documento14 pagineMedicina 57 00032 (01 14)fauzan nandana yoshNessuna valutazione finora

- Question Bank Chemistry (B.Tech.) : Solid StateDocumento10 pagineQuestion Bank Chemistry (B.Tech.) : Solid StatenraiinNessuna valutazione finora

- Profile of RespondentsDocumento36 pagineProfile of RespondentsPratibha SharmaNessuna valutazione finora

- ANNEX I of Machinery Directive 2006 - 42 - EC - Summary - Machinery Directive 2006 - 42 - CE - Functional Safety & ATEX Directive 2014 - 34 - EUDocumento6 pagineANNEX I of Machinery Directive 2006 - 42 - EC - Summary - Machinery Directive 2006 - 42 - CE - Functional Safety & ATEX Directive 2014 - 34 - EUAnandababuNessuna valutazione finora

- Service Manual - DM0412SDocumento11 pagineService Manual - DM0412SStefan Jovanovic100% (1)

- CHAPTER 3 Formwork Part 1Documento39 pagineCHAPTER 3 Formwork Part 1nasNessuna valutazione finora

- Accomplishment Report Rle Oct.Documento7 pagineAccomplishment Report Rle Oct.krull243Nessuna valutazione finora

- Development of Elevator Ropes: Tech Tip 15Documento2 pagineDevelopment of Elevator Ropes: Tech Tip 15أحمد دعبسNessuna valutazione finora

- Muet Topic 10 City Life Suggested Answer and IdiomsDocumento3 pagineMuet Topic 10 City Life Suggested Answer and IdiomsMUHAMAD FAHMI BIN SHAMSUDDIN MoeNessuna valutazione finora

- BMC Brochure WebDocumento4 pagineBMC Brochure WebVikram Pratap SinghNessuna valutazione finora

- Eaton Current Limiting FusesDocumento78 pagineEaton Current Limiting FusesEmmanuel EntzanaNessuna valutazione finora

- JIDMR SCOPUS Ke 4 Anwar MallongiDocumento4 pagineJIDMR SCOPUS Ke 4 Anwar Mallongiadhe yuniarNessuna valutazione finora

- Dearcán Ó Donnghaile: ProfileDocumento2 pagineDearcán Ó Donnghaile: Profileapi-602752895Nessuna valutazione finora

- Insurance CodeDocumento18 pagineInsurance CodeKenneth Holasca100% (1)

- Theory of Accounts On Business CombinationDocumento2 pagineTheory of Accounts On Business CombinationheyNessuna valutazione finora

- ECO-321 Development Economics: Instructor Name: Syeda Nida RazaDocumento10 pagineECO-321 Development Economics: Instructor Name: Syeda Nida RazaLaiba MalikNessuna valutazione finora

- Timberwolf TW 230DHB Wood Chipper Instruction ManualDocumento59 pagineTimberwolf TW 230DHB Wood Chipper Instruction Manualthuan100% (1)

- 756S PDFDocumento248 pagine756S PDFShahzad FidaNessuna valutazione finora

- Stepanenko DermatologyDocumento556 pagineStepanenko DermatologySanskar DeyNessuna valutazione finora

- A0002 HR Operations Manual Quick Reference FileDocumento6 pagineA0002 HR Operations Manual Quick Reference FileRaffy Pax Galang RafaelNessuna valutazione finora

- Water Security STD 9th Textbook by Techy BagDocumento86 pagineWater Security STD 9th Textbook by Techy Bagpooja TiwariNessuna valutazione finora

- DefibrillatorDocumento2 pagineDefibrillatorVasanth VasanthNessuna valutazione finora

- PaperDocumento21 paginePaperAnonymous N2TkzrNessuna valutazione finora