Potrebbero piacerti anche

- Chapter 7Documento18 pagineChapter 7kathleenNessuna valutazione finora

- Cost Chapter 15 (1-13)Documento5 pagineCost Chapter 15 (1-13)Ericka Hazel Osorio0% (1)

- Standard Costing - Answer KeyDocumento6 pagineStandard Costing - Answer KeyRoselyn LumbaoNessuna valutazione finora

- 222Documento3 pagine222Carlo ParasNessuna valutazione finora

- Test Bank Chapter 4 Process CostingDocumento52 pagineTest Bank Chapter 4 Process Costingelaine100% (1)

- (Resa2017) Mas-A (Management Accounting)Documento4 pagine(Resa2017) Mas-A (Management Accounting)Adam SmithNessuna valutazione finora

- AssignmentDocumento2 pagineAssignmentspongebob squarepantsNessuna valutazione finora

- Acctg201 Exercises2Documento18 pagineAcctg201 Exercises2sarahbeeNessuna valutazione finora

- Psba Ac 15 Cost Accounting Lecture Note 2019 Answer KeyDocumento45 paginePsba Ac 15 Cost Accounting Lecture Note 2019 Answer KeyracabrerosNessuna valutazione finora

- This Study Resource Was: Award: 1.00 PointDocumento2 pagineThis Study Resource Was: Award: 1.00 PointAaron Jan FelicildaNessuna valutazione finora

- Final Term Quiz 3 On Cost of Production Report - FIFO CostingDocumento4 pagineFinal Term Quiz 3 On Cost of Production Report - FIFO CostingYhenuel Josh LucasNessuna valutazione finora

- DocDocumento8 pagineDocJAY AUBREY PINEDANessuna valutazione finora

- Quiz 6 Process Costing SolutionsDocumento7 pagineQuiz 6 Process Costing SolutionsralphalonzoNessuna valutazione finora

- Acctg201 PCLossesLectureNotesDocumento17 pagineAcctg201 PCLossesLectureNotesSophia Marie Eredia FerolinoNessuna valutazione finora

- SCM Sol 05 14Documento14 pagineSCM Sol 05 14bloomshing0% (1)

- COST ACCOUNTING 1-5 FinalDocumento12 pagineCOST ACCOUNTING 1-5 FinalChristian Blanza LlevaNessuna valutazione finora

- Final Quiz 1Documento4 pagineFinal Quiz 1maysel qtNessuna valutazione finora

- Product Costing: Quizzer (Do-It-Yourself Drill)Documento7 pagineProduct Costing: Quizzer (Do-It-Yourself Drill)loraine payuyoNessuna valutazione finora

- Just-in-Time and Backflushing 1Documento6 pagineJust-in-Time and Backflushing 1Claudette ClementeNessuna valutazione finora

- 1Documento2 pagine1Your MaterialsNessuna valutazione finora

- Practical AccountingDocumento25 paginePractical AccountingWed CornelNessuna valutazione finora

- MS 1806 Inventory ModelDocumento5 pagineMS 1806 Inventory ModelMariane MananganNessuna valutazione finora

- Chapter 5 - Solutions To Cost Accounting Book (Raiborn and Kinney, 2 Phil Edition)Documento22 pagineChapter 5 - Solutions To Cost Accounting Book (Raiborn and Kinney, 2 Phil Edition)Mark Johnrei GandiaNessuna valutazione finora

- ABCDocumento8 pagineABCanggandakonoh33% (3)

- CH2 QuizkeyDocumento5 pagineCH2 QuizkeyiamacrusaderNessuna valutazione finora

- Cost Accounting Quizzer No. 1: Basic ConceptsDocumento11 pagineCost Accounting Quizzer No. 1: Basic ConceptsLuming100% (1)

- Activity Based Costing ReviewerDocumento1 paginaActivity Based Costing ReviewerJonna LynneNessuna valutazione finora

- Backflush Costing System and Activity Based Costing QuestionsDocumento23 pagineBackflush Costing System and Activity Based Costing QuestionsMedalla NikkoNessuna valutazione finora

- Accounting For Joint Products/By-Products: Multiple ChoiceDocumento10 pagineAccounting For Joint Products/By-Products: Multiple ChoiceAldrin CabangbangNessuna valutazione finora

- CH 09Documento34 pagineCH 09Pj Jn NavarroNessuna valutazione finora

- Joint & by ProductsDocumento10 pagineJoint & by Productsharry severino0% (1)

- Acctg 13 - Midterm ExamDocumento8 pagineAcctg 13 - Midterm ExamMary Grace Castillo AlmonedaNessuna valutazione finora

- Activity Cost and AnalysisDocumento40 pagineActivity Cost and AnalysisChan ChanNessuna valutazione finora

- 2,436,630 (General Instruction: Use 4-Decimal PVF Use Separator, No Space, Round Off Final Answer To Whole Number)Documento2 pagine2,436,630 (General Instruction: Use 4-Decimal PVF Use Separator, No Space, Round Off Final Answer To Whole Number)max pNessuna valutazione finora

- Job Order Costing Difficult RoundDocumento8 pagineJob Order Costing Difficult RoundsarahbeeNessuna valutazione finora

- COST ACCOUNTING 1-6 FinalDocumento22 pagineCOST ACCOUNTING 1-6 FinalChristian Blanza Lleva0% (1)

- Cost Acctg. - HO#9Documento5 pagineCost Acctg. - HO#9JOSE COTONER0% (1)

- Voyager IncDocumento1 paginaVoyager IncLian GarlNessuna valutazione finora

- Cost ch03Documento25 pagineCost ch03Ahmed ShoushaNessuna valutazione finora

- 25 Profit-Performance Measurements & Intracompany Transfer PricingDocumento13 pagine25 Profit-Performance Measurements & Intracompany Transfer PricingLaurenz Simon ManaliliNessuna valutazione finora

- CH 02Documento53 pagineCH 02CloudKielGuiangNessuna valutazione finora

- Chapter5 JustinTimeandBackflushAccountingDocumento21 pagineChapter5 JustinTimeandBackflushAccountingFaye Nepomuceno-Valencia0% (1)

- Cost Accounting Quiz 4Documento4 pagineCost Accounting Quiz 4andreamrieNessuna valutazione finora

- What Are The Two Basic Systems of Cost Accounting and Under What Conditions May Each Be Used AdvantageouslyDocumento2 pagineWhat Are The Two Basic Systems of Cost Accounting and Under What Conditions May Each Be Used Advantageouslygazer beam100% (1)

- Midterms 201 NotesDocumento6 pagineMidterms 201 NotesLyn AbudaNessuna valutazione finora

- Cost Accounting IANDocumento10 pagineCost Accounting IANchris ian Lestino100% (2)

- Cabria Cpa Review Center: Tel. Nos. (043) 980-6659Documento2 pagineCabria Cpa Review Center: Tel. Nos. (043) 980-6659MaeNessuna valutazione finora

- Process 1-7Documento10 pagineProcess 1-7Christian Blanza LlevaNessuna valutazione finora

- Select The Letter of The Best Answer.: Process Costing BCSVDocumento20 pagineSelect The Letter of The Best Answer.: Process Costing BCSVAngelika NapolesNessuna valutazione finora

- Process Costing McqsDocumento4 pagineProcess Costing McqsJitesh Maheshwari100% (1)

- Chapter 04 Process Costing and Hybrid Product-Costing SystemsDocumento21 pagineChapter 04 Process Costing and Hybrid Product-Costing SystemsJc AdanNessuna valutazione finora

- COSTACCTGDocumento112 pagineCOSTACCTGMaria Emarla Grace CanozaNessuna valutazione finora

- Process and Job Order TheoriesDocumento12 pagineProcess and Job Order TheoriesAngelica ManaoisNessuna valutazione finora

- Chapter 4: Process Costing and Hybrid Product-Costing SystemsDocumento33 pagineChapter 4: Process Costing and Hybrid Product-Costing Systemsrandom17341Nessuna valutazione finora

- Chapter 05 Testbank: Wages Paid To A Supervisor in A Factory Are A Part ofDocumento52 pagineChapter 05 Testbank: Wages Paid To A Supervisor in A Factory Are A Part ofHiền DiệuNessuna valutazione finora

- MCQ CostDocumento13 pagineMCQ CostLouina Yncierto100% (1)

- A03 - Chapter 5 Job Order Costing (Theories)Documento4 pagineA03 - Chapter 5 Job Order Costing (Theories)Rigel Kent MansuetoNessuna valutazione finora

- Instructions. Write Your Final Answers On The Answer Sheet Provided. For Problem Solving Items, Please Write Solutions On The Answer Sheet AlsoDocumento8 pagineInstructions. Write Your Final Answers On The Answer Sheet Provided. For Problem Solving Items, Please Write Solutions On The Answer Sheet AlsoJozette TorinoNessuna valutazione finora

- Chapter 4 Accounting Flashcards - QuizletDocumento11 pagineChapter 4 Accounting Flashcards - QuizletEdi wow WowNessuna valutazione finora

- Process Costing TheoryDocumento3 pagineProcess Costing TheoryDaniel OngNessuna valutazione finora

- FINAL 99.1 1st SamplexDocumento6 pagineFINAL 99.1 1st SamplexMelissa FelicianoNessuna valutazione finora

- Compiled Exercises FAR 1Documento59 pagineCompiled Exercises FAR 1KianJohnCentenoTurico100% (7)

- Book 1Documento127 pagineBook 1MOORTHY.KENessuna valutazione finora

- Book Solution Accounting Principles Jerry J Weygandt Barbara TrenholmDocumento54 pagineBook Solution Accounting Principles Jerry J Weygandt Barbara TrenholmHuy AnhNessuna valutazione finora

- PDF Solution Manual Partnership Amp Corporation 2014 2015pdfDocumento85 paginePDF Solution Manual Partnership Amp Corporation 2014 2015pdfGenevieve Anne AlagonNessuna valutazione finora

- Sol. Man. - Chapter 13 - Partnership DissolutionDocumento8 pagineSol. Man. - Chapter 13 - Partnership DissolutionPeter PiperNessuna valutazione finora

- Acc 201 4Documento6 pagineAcc 201 4Trickster TwelveNessuna valutazione finora

- Cambridge IGCSE™: Accounting 0452/21 May/June 2022Documento14 pagineCambridge IGCSE™: Accounting 0452/21 May/June 2022lewisNessuna valutazione finora

- Things You Need To Know About Telstra Services c048Documento12 pagineThings You Need To Know About Telstra Services c048Tayntayn MugolNessuna valutazione finora

- Divya Designo Tiles 201920 Itr - 1Documento64 pagineDivya Designo Tiles 201920 Itr - 1Suman jhaNessuna valutazione finora

- CH 10Documento39 pagineCH 10anjo hosmerNessuna valutazione finora

- Final AccountsDocumento43 pagineFinal AccountsJincy Geevarghese100% (1)

- Cash and Cash Equivalents ReviewerDocumento4 pagineCash and Cash Equivalents ReviewerWinnie ToribioNessuna valutazione finora

- SOA Report UnlockedDocumento5 pagineSOA Report Unlockedcvaishnav820Nessuna valutazione finora

- Total Assets P2,888,000: Debit To ExpensesDocumento25 pagineTotal Assets P2,888,000: Debit To ExpensesLove FreddyNessuna valutazione finora

- 11 QP Final (2021-22)Documento4 pagine11 QP Final (2021-22)Flick OPNessuna valutazione finora

- JPMCStatementDocumento4 pagineJPMCStatementhealthymassagecs50% (2)

- Internship ReportDocumento24 pagineInternship ReportTushar Bhosale0% (1)

- Acc 103 - Day 25 - TGDocumento13 pagineAcc 103 - Day 25 - TGleisky3.07Nessuna valutazione finora

- PACRADocumento516 paginePACRABenjamin Banda100% (1)

- Grade 10 Provincial Case Study QP 2023Documento5 pagineGrade 10 Provincial Case Study QP 2023kwazy dlaminiNessuna valutazione finora

- SMChap 008Documento55 pagineSMChap 008Ine100% (2)

- 4Documento24 pagine4Kevin HaoNessuna valutazione finora

- Control Accounts NotesDocumento8 pagineControl Accounts NotesMehereen AubdoollahNessuna valutazione finora

- Advanced Accounting Part II Quiz 13 Intercompany Profits Long QuizDocumento14 pagineAdvanced Accounting Part II Quiz 13 Intercompany Profits Long QuizRarajNessuna valutazione finora

- To Record Estimate of Uncollectible AccountsDocumento2 pagineTo Record Estimate of Uncollectible AccountssaraNessuna valutazione finora

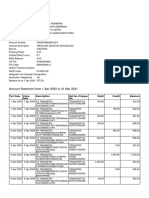

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento14 pagineAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceHyper GamingNessuna valutazione finora

- Salary AccountDocumento13 pagineSalary AccountMahdy MohamedNessuna valutazione finora

- The Double Entry System For Assets, Capital and LiabilitiesDocumento2 pagineThe Double Entry System For Assets, Capital and LiabilitiesAung Zaw HtweNessuna valutazione finora

- CPA Financial Accounting SyllabusDocumento11 pagineCPA Financial Accounting SyllabusKasujja AidenNessuna valutazione finora