Potrebbero piacerti anche

- Audit Findings and Recommendations Com AudDocumento10 pagineAudit Findings and Recommendations Com AudJubert DimakataeNessuna valutazione finora

- Sample Letter of TransmittalDocumento1 paginaSample Letter of TransmittalJubert DimakataeNessuna valutazione finora

- Survey Questionnaire SampleDocumento1 paginaSurvey Questionnaire SampleJubert DimakataeNessuna valutazione finora

- Resume FormatDocumento2 pagineResume FormatSheila Mae Guerta LaceronaNessuna valutazione finora

- Sources of Information For ObliConDocumento2 pagineSources of Information For ObliConJubert DimakataeNessuna valutazione finora

- Fishbone For Obladi ObladaDocumento1 paginaFishbone For Obladi ObladaJubert DimakataeNessuna valutazione finora

- ABC Company Audit Report FindingsDocumento3 pagineABC Company Audit Report FindingsJubert DimakataeNessuna valutazione finora

- Income Tax Principles ExplainedDocumento1 paginaIncome Tax Principles ExplainedJubert DimakataeNessuna valutazione finora

- Articles of Incorporation SampleDocumento7 pagineArticles of Incorporation SampleJubert DimakataeNessuna valutazione finora

- AIS Chapter 3 OutlineDocumento4 pagineAIS Chapter 3 OutlineJubert DimakataeNessuna valutazione finora

- 1-10 Findings For AuditDocumento2 pagine1-10 Findings For AuditJubert DimakataeNessuna valutazione finora

- Activity-Based Costing and ManagementDocumento22 pagineActivity-Based Costing and ManagementDaniel John Cañares LegaspiNessuna valutazione finora

- Difference Between "Director" and "TrusteeDocumento1 paginaDifference Between "Director" and "TrusteeJubert DimakataeNessuna valutazione finora

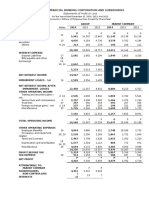

- Rizal Commercial Banking Corporation Financial StatementsDocumento2 pagineRizal Commercial Banking Corporation Financial StatementsJubert DimakataeNessuna valutazione finora

- Practical Accounting 1Documento3 paginePractical Accounting 1Angelo Otañes GasatanNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Bielomatik Calibration GuideDocumento8 pagineBielomatik Calibration Guide김동옥Nessuna valutazione finora

- Organic Pigments. Azo PigmentsDocumento7 pagineOrganic Pigments. Azo PigmentsLiliana HigueraNessuna valutazione finora

- An Efficient and Robust Access Method For Points and RectanglesDocumento38 pagineAn Efficient and Robust Access Method For Points and RectanglesAlok YadavNessuna valutazione finora

- ReviewerDocumento7 pagineReviewerDiana Marie Vargas CariñoNessuna valutazione finora

- SIMATIC S7 Connector Configurator enUS en-USDocumento104 pagineSIMATIC S7 Connector Configurator enUS en-USnemarc08Nessuna valutazione finora

- Lecture 7Documento28 pagineLecture 7Nkugwa Mark WilliamNessuna valutazione finora

- Extending The Message Pipeline With Masstransit Middleware: Roland GuijtDocumento18 pagineExtending The Message Pipeline With Masstransit Middleware: Roland GuijtPhuc VinhNessuna valutazione finora

- Week 2 Calculation ClassDocumento8 pagineWeek 2 Calculation ClassMuhamad Muhaiman MustafaNessuna valutazione finora

- Unified Modeling Language (UML) : An OverviewDocumento37 pagineUnified Modeling Language (UML) : An OverviewRaddad Al KingNessuna valutazione finora

- Encrypted TerrorismDocumento62 pagineEncrypted TerrorismUlisesodisseaNessuna valutazione finora

- Experiment No:01 Full Adder: Aim AlgorithmDocumento25 pagineExperiment No:01 Full Adder: Aim AlgorithmKiran AthaniNessuna valutazione finora

- How Do I Read My Friend'S Whatsapp Chat Without Taking His Phone?Documento6 pagineHow Do I Read My Friend'S Whatsapp Chat Without Taking His Phone?Mahesh KumarNessuna valutazione finora

- Amplitude Modulation Fundamental - Take Home Quiz 2Documento3 pagineAmplitude Modulation Fundamental - Take Home Quiz 2Janica Rheanne JapsayNessuna valutazione finora

- How To - Setup DDNS With The LG NAS - Techno-MuffinDocumento4 pagineHow To - Setup DDNS With The LG NAS - Techno-MuffinswagatarcNessuna valutazione finora

- Bachata MusicalityDocumento5 pagineBachata MusicalityDarren MooreNessuna valutazione finora

- Lenovo PresentationDocumento21 pagineLenovo PresentationAneel Amdani100% (1)

- Peoplesoft Row Level SecurityDocumento18 paginePeoplesoft Row Level Securityapi-262778560% (1)

- Hidraulico 246C JAYDocumento30 pagineHidraulico 246C JAYFranklin Labbe100% (3)

- VolvoDocumento220 pagineVolvoturbokolosabacNessuna valutazione finora

- Radio Interference PDFDocumento76 pagineRadio Interference PDFBorut ZaletelNessuna valutazione finora

- Top 5 Best Photo Editing App in HindiDocumento3 pagineTop 5 Best Photo Editing App in HindiTech Kashif0% (1)

- Energy Harvesting Sources, Storage Devices and System Topologies For Environmental Wireless Sensor Networks - A ReviewDocumento35 pagineEnergy Harvesting Sources, Storage Devices and System Topologies For Environmental Wireless Sensor Networks - A ReviewimaculateNessuna valutazione finora

- List of VirusesDocumento11 pagineList of Virusesfanboy25Nessuna valutazione finora

- Companies Registry Online System FAQsDocumento11 pagineCompanies Registry Online System FAQsVicard GibbingsNessuna valutazione finora

- Module 1 Ethernet and VLAN: Lab 1-1 Ethernet Interface and Link Configuration Learning ObjectivesDocumento15 pagineModule 1 Ethernet and VLAN: Lab 1-1 Ethernet Interface and Link Configuration Learning ObjectivesChaima BelhediNessuna valutazione finora

- Re 1999 11Documento100 pagineRe 1999 11Enéas BaroneNessuna valutazione finora

- Service Manual: Compact Component SystemDocumento32 pagineService Manual: Compact Component SystemNestor CastilloNessuna valutazione finora

- (Non-QU) Linear Algebra by DR - Gabriel Nagy PDFDocumento362 pagine(Non-QU) Linear Algebra by DR - Gabriel Nagy PDFamrNessuna valutazione finora

- Correlation AnalysisDocumento20 pagineCorrelation AnalysisVeerendra NathNessuna valutazione finora

- HashiCorp Packer in Production - John BoeroDocumento246 pagineHashiCorp Packer in Production - John BoerostroganovborisNessuna valutazione finora