Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Invoice TemplateDocumento9 pagineInvoice Templaten100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- GOVERNMENT SAMPLES - Resumes, Selection Criteria & Cover LettersDocumento45 pagineGOVERNMENT SAMPLES - Resumes, Selection Criteria & Cover LettersKellu Baba100% (3)

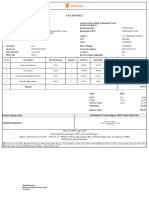

- Invoice SpeakerDocumento1 paginaInvoice Speakeranil kalraNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Your Investment Property GuideDocumento24 pagineYour Investment Property GuideCoana ArtistNessuna valutazione finora

- Facture Apple Store UsDocumento2 pagineFacture Apple Store Usmelgayla9Nessuna valutazione finora

- Employee Details Payment & Leave Details: Arrears Amount CurrentDocumento2 pagineEmployee Details Payment & Leave Details: Arrears Amount CurrentRamesh yaraboluNessuna valutazione finora

- Infrastructure Development Plan for Chhattisgarh - Road Project Viability OptionsDocumento3 pagineInfrastructure Development Plan for Chhattisgarh - Road Project Viability Optionsjavedarzoo50% (2)

- Barangay Micro Business Enterprise (Bmbe) Act: 13284-TOPIC 3Documento16 pagineBarangay Micro Business Enterprise (Bmbe) Act: 13284-TOPIC 3kim cheNessuna valutazione finora

- Behavioral Economics: Re-Modeling Standard Economic Models For Human IrrationalityDocumento8 pagineBehavioral Economics: Re-Modeling Standard Economic Models For Human IrrationalityPhillip Huff100% (1)

- Bills-Book & FuelDocumento2 pagineBills-Book & FuelEdwin DevdasNessuna valutazione finora

- Cake - Extra - James - SukreeDocumento72 pagineCake - Extra - James - SukreevaibhavdschoolNessuna valutazione finora

- Philippine Health Providers Tax LiabilityDocumento3 paginePhilippine Health Providers Tax Liabilityana ortizNessuna valutazione finora

- CIR Power to Interpret Tax LawsDocumento2 pagineCIR Power to Interpret Tax LawsTimothy Joel CabreraNessuna valutazione finora

- Selection of Warehouse LocationDocumento79 pagineSelection of Warehouse Locationlatifah 6698Nessuna valutazione finora

- The Sad State of PoliticsDocumento2 pagineThe Sad State of PoliticsPhillip HuffNessuna valutazione finora

- Four Loko: Dangerous Drink or The Next ScapegoatDocumento4 pagineFour Loko: Dangerous Drink or The Next ScapegoatPhillip HuffNessuna valutazione finora

- The 21 Year-Old Minimum Legal Drinking Age: Separating Truth From HypeDocumento13 pagineThe 21 Year-Old Minimum Legal Drinking Age: Separating Truth From HypePhillip HuffNessuna valutazione finora

- Coursera University of Melbourne Macro Economics Course Peer Assessment AssignmentDocumento7 pagineCoursera University of Melbourne Macro Economics Course Peer Assessment AssignmentpsstquestionNessuna valutazione finora

- BDU MSc in Accounting & Finance Course CatalogDocumento50 pagineBDU MSc in Accounting & Finance Course Catalogdrsrn100% (2)

- Tax Integration CookbookDocumento76 pagineTax Integration CookbookM.Medina100% (1)

- Three Basic Legal Forms of Business: Partnership vs CorporationDocumento107 pagineThree Basic Legal Forms of Business: Partnership vs CorporationJhaister Ashley LayugNessuna valutazione finora

- Characteristic of Vat-Business TaxationDocumento8 pagineCharacteristic of Vat-Business TaxationAthena LouiseNessuna valutazione finora

- Salary Scheme: - Marc Angelo Pilapil - Aaron Garcia - Mark Amosig - Raine GonzalesDocumento5 pagineSalary Scheme: - Marc Angelo Pilapil - Aaron Garcia - Mark Amosig - Raine GonzalesMarc Angelo PilapilNessuna valutazione finora

- Export Tax InvoiceDocumento1 paginaExport Tax InvoiceNavin RaviNessuna valutazione finora

- GST Practical Questions Vol - 1 (New) by CA Vivek GabaDocumento13 pagineGST Practical Questions Vol - 1 (New) by CA Vivek Gabavamshi9686Nessuna valutazione finora

- Adjust Maryland withholdingDocumento2 pagineAdjust Maryland withholdingsosureyNessuna valutazione finora

- Taco 0088166061500044Documento1 paginaTaco 0088166061500044Sourav ChakrabortyNessuna valutazione finora

- Ligj Nr. 34, Dt. 17.6.2019 Ligji I Ri - EN (1) OkDocumento15 pagineLigj Nr. 34, Dt. 17.6.2019 Ligji I Ri - EN (1) OkEgiNessuna valutazione finora

- ReviewerDocumento8 pagineReviewerjescy pauloNessuna valutazione finora

- Chapter Three: International Taxation IssuesDocumento39 pagineChapter Three: International Taxation Issuesembiale ayaluNessuna valutazione finora

- Mepco Online BilllDocumento1 paginaMepco Online Billlمحمد فصیح آفتابNessuna valutazione finora

- Introduction To Federal Income Taxation in Canada 43rd Edition 2022-2023 Edition by Nathalie Johnstone, Devan Mescall, Julie Robson Solution ManualDocumento22 pagineIntroduction To Federal Income Taxation in Canada 43rd Edition 2022-2023 Edition by Nathalie Johnstone, Devan Mescall, Julie Robson Solution ManualTest bank WorldNessuna valutazione finora

- A.Arulmozhi Shivam Pan No: Aayps8451P Income Tax Return For The Assessment Year 2003-2004Documento11 pagineA.Arulmozhi Shivam Pan No: Aayps8451P Income Tax Return For The Assessment Year 2003-2004api-19728905Nessuna valutazione finora

- CA PRANAV CHANDAK'S ERRORLESS TAXATION QUESTION BANKDocumento8 pagineCA PRANAV CHANDAK'S ERRORLESS TAXATION QUESTION BANKSimran MeherNessuna valutazione finora