Potrebbero piacerti anche

- Monetary Policy and Central Banking History of Philippine BankingDocumento14 pagineMonetary Policy and Central Banking History of Philippine BankingGloria MalabananNessuna valutazione finora

- History of Financial SystemDocumento5 pagineHistory of Financial SystemPauline Sy100% (1)

- Banking Institutions History Classifications and FunctionsDocumento13 pagineBanking Institutions History Classifications and FunctionsJessielyn GialogoNessuna valutazione finora

- The Philippine CurrencyDocumento72 pagineThe Philippine CurrencyKaren LaccayNessuna valutazione finora

- History of Banking in The PhilsDocumento12 pagineHistory of Banking in The PhilsLyka QuintanoNessuna valutazione finora

- Ma'am MaconDocumento7 pagineMa'am MaconKim Nicole Reyes100% (1)

- History of The CooperativeDocumento3 pagineHistory of The CooperativeNormae AnnNessuna valutazione finora

- Efficiency: Overview of The Financial SystemDocumento12 pagineEfficiency: Overview of The Financial SystemErika Anne Jaurigue100% (1)

- BSA2A WrittenReports Thrift-BanksDocumento5 pagineBSA2A WrittenReports Thrift-Banksrobert pilapilNessuna valutazione finora

- Financial InstitutionsDocumento76 pagineFinancial InstitutionsGaurav Rathaur100% (1)

- Basfin BSPDocumento30 pagineBasfin BSPCarabellona Rosales - UyNessuna valutazione finora

- Ethics ProjectDocumento16 pagineEthics ProjectMerrin MathewNessuna valutazione finora

- Introduction to Credit FundamentalsDocumento4 pagineIntroduction to Credit FundamentalsLemon OwNessuna valutazione finora

- The Structure of Financial MarketsDocumento7 pagineThe Structure of Financial MarketsVũ Thị Thu HiếuNessuna valutazione finora

- Global Finance With Electronic Banking - Prelim ExamDocumento5 pagineGlobal Finance With Electronic Banking - Prelim ExamAlfonso Joel GonzalesNessuna valutazione finora

- An Overview of the Philippine Financial SystemDocumento61 pagineAn Overview of the Philippine Financial SystemQuenie De la CruzNessuna valutazione finora

- BFC5935 - Tutorial 1 Solutions PDFDocumento7 pagineBFC5935 - Tutorial 1 Solutions PDFXue Xu100% (1)

- What Is Financial RiskDocumento9 pagineWhat Is Financial RiskDeboit BhattacharjeeNessuna valutazione finora

- Income and Business TaxationDocumento69 pagineIncome and Business TaxationMarie CarreraNessuna valutazione finora

- CB-03 Central Monetary AuthorityDocumento7 pagineCB-03 Central Monetary AuthorityJHERRY MIG SEVILLANessuna valutazione finora

- FinancialDocumento12 pagineFinancialCinco SyeteNessuna valutazione finora

- Banking Adbl EnglishDocumento74 pagineBanking Adbl Englishdevi ghimireNessuna valutazione finora

- Central Bank FunctionsDocumento3 pagineCentral Bank FunctionsPrithi Agarwal50% (2)

- Overview of Treasury Management ModuleDocumento11 pagineOverview of Treasury Management ModuleJordan Loren MaeNessuna valutazione finora

- LESSON 1 Financial MarketDocumento7 pagineLESSON 1 Financial MarketJames Deo CruzNessuna valutazione finora

- Financial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksDocumento5 pagineFinancial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksAnamMalikNessuna valutazione finora

- Finman ReviewerDocumento27 pagineFinman Reviewerben yiNessuna valutazione finora

- International Business and TradeDocumento6 pagineInternational Business and TradeAnton Biel De LeonNessuna valutazione finora

- Philippine Monetary Policy OverviewDocumento12 paginePhilippine Monetary Policy OverviewLyn AmbrayNessuna valutazione finora

- History of Banking IndustryDocumento7 pagineHistory of Banking IndustryKimberly PasaloNessuna valutazione finora

- Bank Supervision and Examination: Laws, Controls, and PurposeDocumento56 pagineBank Supervision and Examination: Laws, Controls, and PurposeKhaizar Moi OlaldeNessuna valutazione finora

- Chattel MortgageDocumento9 pagineChattel MortgageLess BalesoroNessuna valutazione finora

- History of Philippine MoneyDocumento12 pagineHistory of Philippine MoneysjlaNessuna valutazione finora

- Chapter 4 Commercial BanksDocumento33 pagineChapter 4 Commercial BanksChichay KarenJoyNessuna valutazione finora

- BTR Functions Draft 6-1-15Documento16 pagineBTR Functions Draft 6-1-15Hanna PentiñoNessuna valutazione finora

- Banking Supervision in the Philippines: Lessons Learned and Future DirectionsDocumento16 pagineBanking Supervision in the Philippines: Lessons Learned and Future DirectionsatoydequitNessuna valutazione finora

- Thrift Banks ActDocumento25 pagineThrift Banks ActMadelle Pineda100% (1)

- Chapter 1Documento17 pagineChapter 1mymajdahotmailNessuna valutazione finora

- I - P - Financial Markets Through TImeDocumento35 pagineI - P - Financial Markets Through TImeWeiyee ValenzuelaNessuna valutazione finora

- Morally Mute ManagersDocumento3 pagineMorally Mute ManagersMic BaldevaronaNessuna valutazione finora

- Metallic Monetary Systems Compared - Bimetallism vs MonometallismDocumento22 pagineMetallic Monetary Systems Compared - Bimetallism vs MonometallismMissVirginia1105Nessuna valutazione finora

- CASE STUDY 1 (Strategic Marketing Management) Mirela FashionsDocumento1 paginaCASE STUDY 1 (Strategic Marketing Management) Mirela FashionsKhyber MassoudyNessuna valutazione finora

- Chapter 2 - National Difference in Political EconomyDocumento52 pagineChapter 2 - National Difference in Political EconomyTroll Nguyễn VănNessuna valutazione finora

- What Is A Bank?: Key TakeawaysDocumento3 pagineWhat Is A Bank?: Key TakeawaysSAMNessuna valutazione finora

- Global Finance and Electronic BankingDocumento2 pagineGlobal Finance and Electronic BankingMhars Dela CruzNessuna valutazione finora

- BSP ReviewerDocumento3 pagineBSP ReviewerJA LAYUGNessuna valutazione finora

- International Financial Institutions: MMS (University of Mumbai)Documento28 pagineInternational Financial Institutions: MMS (University of Mumbai)asadNessuna valutazione finora

- Managerial Accounting Term Paper Sta. Lucia Land, Inc.Documento23 pagineManagerial Accounting Term Paper Sta. Lucia Land, Inc.Joan BasayNessuna valutazione finora

- Finman Chapter 7 SummaryDocumento2 pagineFinman Chapter 7 SummaryJoyce Anne Gevero CarreraNessuna valutazione finora

- Kinds of MoneyDocumento24 pagineKinds of MoneyIntet Nuestro100% (1)

- Philippine Deposit Insurance CorporationDocumento26 paginePhilippine Deposit Insurance CorporationAleks OpsNessuna valutazione finora

- Mutual Funds ExplainedDocumento11 pagineMutual Funds ExplainedjchazneyNessuna valutazione finora

- Good Governance and Social Responsibility ReviewerDocumento5 pagineGood Governance and Social Responsibility ReviewerDe Villa, Ivy JaneNessuna valutazione finora

- Evolution of Financial SystemDocumento12 pagineEvolution of Financial SystemGautam JayasuryaNessuna valutazione finora

- Role of Financial Markets and InstitutionsDocumento30 pagineRole of Financial Markets and InstitutionsĒsrar BalócNessuna valutazione finora

- Prelim - Int'l Business & TradeDocumento13 paginePrelim - Int'l Business & TradeGIGI BODO100% (1)

- Pse HistoryDocumento36 paginePse HistoryRyan Angelo MarasiganNessuna valutazione finora

- Central BankingDocumento43 pagineCentral BankingOche TjNessuna valutazione finora

- Asset Allocation 5E (PB): Balancing Financial Risk, Fifth EditionDa EverandAsset Allocation 5E (PB): Balancing Financial Risk, Fifth EditionValutazione: 4 su 5 stelle4/5 (13)

- Revised Withholding Tax TablesDocumento1 paginaRevised Withholding Tax TablesJonasAblangNessuna valutazione finora

- Excel ShortcutsDocumento12 pagineExcel ShortcutsmsNessuna valutazione finora

- Your Personal ConvictionsDocumento2 pagineYour Personal ConvictionsYasonsky CaptainNessuna valutazione finora

- Accounting GuideDocumento152 pagineAccounting GuidemsNessuna valutazione finora

- Chapter 10Documento4 pagineChapter 10Judith Salome Basquinas0% (1)

- Financial Statement AnalysisDocumento5 pagineFinancial Statement AnalysisErica CaliuagNessuna valutazione finora

- Wedding MSGDocumento1 paginaWedding MSGmsNessuna valutazione finora

- Time Value of MoneyDocumento54 pagineTime Value of MoneyJoyce Ann Basilio100% (5)

- Parts of BicycleDocumento1 paginaParts of BicyclemsNessuna valutazione finora

- Chapter 1Documento49 pagineChapter 1msNessuna valutazione finora

- Financial RatiosDocumento2 pagineFinancial RatiosmsNessuna valutazione finora

- The Rizal Family Lola Lolay of Bahay Na BatoDocumento32 pagineThe Rizal Family Lola Lolay of Bahay Na BatomsNessuna valutazione finora

- Sermon Notes: Making Wise DecisionsDocumento2 pagineSermon Notes: Making Wise DecisionsmsNessuna valutazione finora

- Post Greek PhilosophersDocumento3 paginePost Greek PhilosophersmsNessuna valutazione finora

- Theoretical FrameworkDocumento1 paginaTheoretical FrameworkmsNessuna valutazione finora

- Term or Phrase Literal Translation: From StrongerDocumento28 pagineTerm or Phrase Literal Translation: From StrongermsNessuna valutazione finora

- Fresh graduate interview answersDocumento1 paginaFresh graduate interview answersmsNessuna valutazione finora

- BLT PRTC Pre-BoardDocumento12 pagineBLT PRTC Pre-BoardJohanna CatahanNessuna valutazione finora

- Coso's ERM Executive SummaryDocumento16 pagineCoso's ERM Executive SummaryWa'el Bibi100% (8)

- The Role of Accounting in Enabling Strategic Corporate Social Responsibility: A Functionalist, Critical and Post-Modern Reading of A Case StudyDocumento2 pagineThe Role of Accounting in Enabling Strategic Corporate Social Responsibility: A Functionalist, Critical and Post-Modern Reading of A Case StudymsNessuna valutazione finora

- RebusesDocumento11 pagineRebusesmsNessuna valutazione finora

- Use Number Discs To Show These NumbersDocumento3 pagineUse Number Discs To Show These NumbersmsNessuna valutazione finora

- Term or Phrase Literal Translation: From StrongerDocumento28 pagineTerm or Phrase Literal Translation: From StrongermsNessuna valutazione finora

- Using The Data Below Construct A Double Horizontal Bar Graph. Favorite Ice Cream Number of Students Grade Level Vanilla-50 Chocolate-50 1Documento2 pagineUsing The Data Below Construct A Double Horizontal Bar Graph. Favorite Ice Cream Number of Students Grade Level Vanilla-50 Chocolate-50 1msNessuna valutazione finora

- Chapter 1Documento4 pagineChapter 1msNessuna valutazione finora

- Tax RateDocumento3 pagineTax Raterommel_007Nessuna valutazione finora

- Revised Withholding Tax TablesDocumento1 paginaRevised Withholding Tax TablesJonasAblangNessuna valutazione finora

- July 2016 CalendarDocumento1 paginaJuly 2016 CalendarmsNessuna valutazione finora

- Coso Full 2011Documento168 pagineCoso Full 2011AneuxAgamNessuna valutazione finora

- Research Methodology on Major Stock Market ScamsDocumento35 pagineResearch Methodology on Major Stock Market ScamsSameer VelaniNessuna valutazione finora

- Chief Financial Officer CFO in Los Angeles CA Resume David YodkovikDocumento2 pagineChief Financial Officer CFO in Los Angeles CA Resume David YodkovikDavidYodkovikNessuna valutazione finora

- Paper 12 - Company Accounts and Audit Syl2012Documento116 paginePaper 12 - Company Accounts and Audit Syl2012sumit4up6rNessuna valutazione finora

- Building an Islamic Venture Capital ModelDocumento12 pagineBuilding an Islamic Venture Capital ModelNader MehdawiNessuna valutazione finora

- Chapter 10Documento12 pagineChapter 10Ginnie G Cristal50% (2)

- Medfield Pharmaceuticals' Valuation and Strategic OptionsDocumento9 pagineMedfield Pharmaceuticals' Valuation and Strategic OptionsvATSALANessuna valutazione finora

- IBPS Clerk Main 2016 Capsule by AffairscloudDocumento91 pagineIBPS Clerk Main 2016 Capsule by AffairscloudMadhu SekharNessuna valutazione finora

- RSM230 Midterm Study NotesDocumento36 pagineRSM230 Midterm Study Noteshugocheung7Nessuna valutazione finora

- Annual Report 2017Documento400 pagineAnnual Report 2017Md. Tareq Aziz100% (1)

- BMO Annual Report 2020Documento218 pagineBMO Annual Report 2020Bilal MustafaNessuna valutazione finora

- Payment Bank Impact On Digital BankingDocumento78 paginePayment Bank Impact On Digital BankingSudharshan Reddy P0% (1)

- Birefps User Guide UpdatedDocumento20 pagineBirefps User Guide UpdatedIreneMackay GiraoNessuna valutazione finora

- Kerala Govt Raises House Building Loan Limit to Rs. 25 LakhDocumento2 pagineKerala Govt Raises House Building Loan Limit to Rs. 25 LakhnarenczNessuna valutazione finora

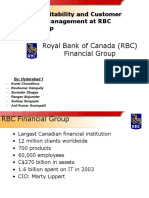

- RBC Case StudyDocumento20 pagineRBC Case StudyIshmeet SinghNessuna valutazione finora

- MCQ - BankingDocumento4 pagineMCQ - Bankingbhaskar51178Nessuna valutazione finora

- Specimen Paper 2014 - FINALDocumento33 pagineSpecimen Paper 2014 - FINALAbdulwahab AhmedNessuna valutazione finora

- Loan With Surety SampleDocumento5 pagineLoan With Surety SampleDnom GLNessuna valutazione finora

- Government Banking InstitutionDocumento3 pagineGovernment Banking Institutionjhoned parraNessuna valutazione finora

- 1 - GREPA v. CA G.R. No. 113899 October 13, 1999Documento2 pagine1 - GREPA v. CA G.R. No. 113899 October 13, 1999Emrico CabahugNessuna valutazione finora

- Open an NPS account in 40 charactersDocumento2 pagineOpen an NPS account in 40 charactersMOHIT GUPTA jiNessuna valutazione finora

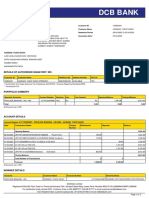

- DCB Bank: Statement of AccountDocumento2 pagineDCB Bank: Statement of AccounthasnainNessuna valutazione finora

- Garbemco StoryDocumento4 pagineGarbemco Storyᜇᜎᜄ ᜁᜄᜉNessuna valutazione finora

- Acknowledgment Receipt Insurance ConfirmationDocumento1 paginaAcknowledgment Receipt Insurance ConfirmationHERMAN DAGIONessuna valutazione finora

- Mr. Juan Dela Cruz's Sari-Sari Store Financial PositionDocumento34 pagineMr. Juan Dela Cruz's Sari-Sari Store Financial PositionPrecious chloe DelacruzNessuna valutazione finora

- 2010 FirstRand Annual Report 1Documento450 pagine2010 FirstRand Annual Report 1Sathya SeelanNessuna valutazione finora

- Tianjin PlasticsDocumento9 pagineTianjin PlasticsmalikatjuhNessuna valutazione finora

- Negotiable Instruments - Meaning, Types & UsesDocumento3 pagineNegotiable Instruments - Meaning, Types & UsesQuishNessuna valutazione finora

- Mohammad Renaldy - CVDocumento10 pagineMohammad Renaldy - CVSales ExecutiveNessuna valutazione finora

- How to add Primary TradelinesDocumento18 pagineHow to add Primary Tradelinesmatt96% (82)

- Bank Financing Proposal for Brick Factory ExpansionDocumento11 pagineBank Financing Proposal for Brick Factory ExpansionSudhakaar ShakyaNessuna valutazione finora