Potrebbero piacerti anche

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Tense Affirmative/Negative/Questi On Use Signal Words: Simple PresentDocumento6 pagineTense Affirmative/Negative/Questi On Use Signal Words: Simple PresentTigercubx9Nessuna valutazione finora

- Business IdiomsDocumento1 paginaBusiness IdiomsTigercubx9Nessuna valutazione finora

- Studies and Methods SensoryDocumento3 pagineStudies and Methods SensoryTigercubx9Nessuna valutazione finora

- Proces Prihvatanja ProizvodaDocumento15 pagineProces Prihvatanja ProizvodaTigercubx9Nessuna valutazione finora

- Business Development Specialist: - Trading Area South East Europe, Belgrade OfficeDocumento1 paginaBusiness Development Specialist: - Trading Area South East Europe, Belgrade OfficeTigercubx9Nessuna valutazione finora

- Uvod Market 2Documento16 pagineUvod Market 2Tigercubx9Nessuna valutazione finora

- 50 Tips For AttractionDocumento120 pagine50 Tips For AttractionTigercubx9Nessuna valutazione finora

- 08 - Bankarski MarketingDocumento23 pagine08 - Bankarski Marketingsladjana_krunic7819Nessuna valutazione finora

- DD Strateski Marketing Strat Mktga Novi Sad 2003Documento4 pagineDD Strateski Marketing Strat Mktga Novi Sad 2003Tigercubx9Nessuna valutazione finora

- Uvod Market 5Documento15 pagineUvod Market 5Tigercubx9Nessuna valutazione finora

- Kotler03 - Media (Scan Environment)Documento28 pagineKotler03 - Media (Scan Environment)Tigercubx9Nessuna valutazione finora

- Sadržaj: Razvoj I Upravljanje Finansijskim ProizvodomDocumento3 pagineSadržaj: Razvoj I Upravljanje Finansijskim ProizvodomTigercubx9Nessuna valutazione finora

- Human Resource Management: CoachingDocumento12 pagineHuman Resource Management: CoachingTigercubx9Nessuna valutazione finora

- Introduction To Leadership: Definition, Leadership and Management, Leadership and Power, Leadership Theories, Leadership StylesDocumento63 pagineIntroduction To Leadership: Definition, Leadership and Management, Leadership and Power, Leadership Theories, Leadership StylesTigercubx9Nessuna valutazione finora

- Political TheoryDocumento120 paginePolitical TheoryTigercubx9100% (1)

- Bmc-Iii Paper-Iv (Media Issues) Content: No. Lesson Writer Vetter Page NoDocumento132 pagineBmc-Iii Paper-Iv (Media Issues) Content: No. Lesson Writer Vetter Page NoTigercubx9Nessuna valutazione finora

- Advertising and PRDocumento140 pagineAdvertising and PRTigercubx9Nessuna valutazione finora

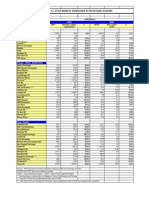

- Americas: Indicators - 4.5 Stock Markets' Significance in The National EconomyDocumento1 paginaAmericas: Indicators - 4.5 Stock Markets' Significance in The National EconomyTigercubx9Nessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- HR Manual-ICSILDocumento5 pagineHR Manual-ICSILpctmtstNessuna valutazione finora

- Change Roller Track and Change Bolt of Shoe Track CraneDocumento2 pagineChange Roller Track and Change Bolt of Shoe Track CraneaneshseNessuna valutazione finora

- Tips For Job Interview - PowerPointDocumento12 pagineTips For Job Interview - PowerPointDeniz MaximilianNessuna valutazione finora

- Lakambini R. Maputi, RN August 28, 2010Documento53 pagineLakambini R. Maputi, RN August 28, 2010praxis_anaelNessuna valutazione finora

- Study Questions 9 (Inflation and Phillips Curve)Documento8 pagineStudy Questions 9 (Inflation and Phillips Curve)Kiran KachhawahaNessuna valutazione finora

- Aug 2 Fresher JobsDocumento27 pagineAug 2 Fresher JobsAneesh DNessuna valutazione finora

- Peace Corps Medical Technical GuidelinesDocumento2 paginePeace Corps Medical Technical GuidelinesAccessible Journal Media: Peace Corps DocumentsNessuna valutazione finora

- A201013 PDFDocumento99 pagineA201013 PDFironcoreNessuna valutazione finora

- The Nature of Human Resource ManagementDocumento6 pagineThe Nature of Human Resource ManagementBrose CathieNessuna valutazione finora

- Vice President Human Resources in NYC NY Resume Amy CarpenterDocumento2 pagineVice President Human Resources in NYC NY Resume Amy Carpenteramycarpenter1Nessuna valutazione finora

- Computer Hardware Servicing NC II 1Documento69 pagineComputer Hardware Servicing NC II 1Jhon Rhem Escandor Hije100% (1)

- Motivation and Job Satisfaction DissertationDocumento5 pagineMotivation and Job Satisfaction DissertationHowToWriteMyPaperOmaha100% (1)

- Topic: Human Resource and PayrollDocumento11 pagineTopic: Human Resource and PayrollMelanie SamsonaNessuna valutazione finora

- ECONOMICS-III Project On: Industrialisation and Its RoleDocumento15 pagineECONOMICS-III Project On: Industrialisation and Its RoleDeepak Sharma100% (1)

- MGG VS NLRCDocumento8 pagineMGG VS NLRCMichelle Dulce Mariano CandelariaNessuna valutazione finora

- Oracle Fusion HCM Absence Management-EP, Abs Plans, Geo HierarchyDocumento48 pagineOracle Fusion HCM Absence Management-EP, Abs Plans, Geo HierarchyvallipoornimaNessuna valutazione finora

- Tell Me About Yourself: 2. What ProfileDocumento2 pagineTell Me About Yourself: 2. What Profilemegha mattaNessuna valutazione finora

- Well Timed Strategy PDFDocumento10 pagineWell Timed Strategy PDFmandaremNessuna valutazione finora

- FAQs (2 May)Documento9 pagineFAQs (2 May)irene.wongNessuna valutazione finora

- Informal Sectors in The Economy: Pertinent IssuesDocumento145 pagineInformal Sectors in The Economy: Pertinent IssuesshanNessuna valutazione finora

- Chapter 1Documento33 pagineChapter 1akinom24Nessuna valutazione finora

- Automation Anxiety: Daniel AkstDocumento13 pagineAutomation Anxiety: Daniel Akstbruna1498Nessuna valutazione finora

- Recruitment and Labor LawsDocumento5 pagineRecruitment and Labor LawsChris MwangiNessuna valutazione finora

- CV Format - Smart0702MeterDocumento2 pagineCV Format - Smart0702MeterNoorul KNessuna valutazione finora

- Task A.P. Møller - Group2 PDFDocumento12 pagineTask A.P. Møller - Group2 PDFSiddharthNessuna valutazione finora

- Factors Affecting The Turnover of Nurses in The Tertiary Hospitals in Davao CityDocumento17 pagineFactors Affecting The Turnover of Nurses in The Tertiary Hospitals in Davao CityshairaNessuna valutazione finora

- BOETT Registration FormDocumento3 pagineBOETT Registration FormJameel KhanNessuna valutazione finora

- A Case Study of The Kentex Fire TragedyDocumento24 pagineA Case Study of The Kentex Fire TragedyDianne Alarcon57% (7)

- Compentency ManagementDocumento6 pagineCompentency ManagementPrativa AryalNessuna valutazione finora

- KELDocumento58 pagineKELrajanathiraNessuna valutazione finora