Potrebbero piacerti anche

- Indonesian OIL PALM & REFINERY Directory, 2015"Documento3 pagineIndonesian OIL PALM & REFINERY Directory, 2015"Central Data MediatamaNessuna valutazione finora

- Horse & Other Equine Production in The US Industry Report PDFDocumento36 pagineHorse & Other Equine Production in The US Industry Report PDFOozax OozaxNessuna valutazione finora

- South African Sugar Industry DirectoryDocumento48 pagineSouth African Sugar Industry Directorynomcebo.msweli838091% (11)

- Finding Buyers Leather Footwear - Italy2Documento5 pagineFinding Buyers Leather Footwear - Italy2Rohit KhareNessuna valutazione finora

- Sunflower Oil Market Analysis 04052011 2Documento32 pagineSunflower Oil Market Analysis 04052011 2tnsamNessuna valutazione finora

- Export Marketing of Agricultural ProductsDocumento18 pagineExport Marketing of Agricultural ProductsRuchira ShuklaNessuna valutazione finora

- International Strategic ManagementDocumento17 pagineInternational Strategic ManagementVadher Amit100% (1)

- 9) Profile On Edible Oil ProductionDocumento80 pagine9) Profile On Edible Oil ProductionMehari Gizachew100% (3)

- Arab Fert Association Directory - 2011Documento120 pagineArab Fert Association Directory - 2011Gurnam Singh100% (2)

- Retail Foods Saudi ArabiaDocumento17 pagineRetail Foods Saudi ArabiaMohaChebi100% (1)

- Technical Report For Tyre Crumb and ShredDocumento47 pagineTechnical Report For Tyre Crumb and ShredMurugan ManiNessuna valutazione finora

- ChemicalsDocumento92 pagineChemicalsBrian KawaskiNessuna valutazione finora

- BOC List of Importers For Suspension-19-January 2017Documento9 pagineBOC List of Importers For Suspension-19-January 2017PortCalls100% (1)

- Client Profile FormDocumento4 pagineClient Profile FormBronwen Elizabeth MaddenNessuna valutazione finora

- Tapping Into Global MarketsDocumento5 pagineTapping Into Global MarketsAli RazzanNessuna valutazione finora

- 5.OliveOil Producers (AUS) !Documento47 pagine5.OliveOil Producers (AUS) !anamac08Nessuna valutazione finora

- EU Trade Shows For Home Decoration, Gifts and Home TextilesDocumento24 pagineEU Trade Shows For Home Decoration, Gifts and Home TextilesReinhard WernerNessuna valutazione finora

- Global Business Opportunities - June 2021Documento52 pagineGlobal Business Opportunities - June 2021VijaiNessuna valutazione finora

- Exporting To Europe Guide: PxhereDocumento28 pagineExporting To Europe Guide: Pxherezinga007Nessuna valutazione finora

- Copper SmelterDocumento13 pagineCopper Smeltermujib uddin siddiquiNessuna valutazione finora

- Palm Oil ShipmentsDocumento1 paginaPalm Oil ShipmentsmalikmobeenNessuna valutazione finora

- Buyers Commodity ListDocumento4 pagineBuyers Commodity ListvanNessuna valutazione finora

- OPTIMAL DISTRIBUTION CHANNEL FOR BROWN SUGARDocumento20 pagineOPTIMAL DISTRIBUTION CHANNEL FOR BROWN SUGARaliyah99Nessuna valutazione finora

- Food Report CGI Hong KongDocumento84 pagineFood Report CGI Hong Kongmehmetredd100% (1)

- The Classification of CottonDocumento23 pagineThe Classification of CottonTeka Weldekidan Abebe100% (1)

- Recycling Companies in LebanonDocumento3 pagineRecycling Companies in LebanonVonder100% (1)

- Azil 2012Documento196 pagineAzil 2012Nikos SakellariouNessuna valutazione finora

- Customer List For TmipDocumento5 pagineCustomer List For TmipTy PhanNessuna valutazione finora

- Egypt Chambers of Commerce and Business Association ContactsDocumento11 pagineEgypt Chambers of Commerce and Business Association ContactsYogesh SharmaNessuna valutazione finora

- PengimportDocumento10 paginePengimportAhmad BorhanudinNessuna valutazione finora

- Kit Kat Brand AnalysisDocumento53 pagineKit Kat Brand Analysisalex88% (24)

- Analysis of Surgical Industry of SialkotDocumento41 pagineAnalysis of Surgical Industry of SialkotMobashar Ali89% (9)

- Sunflower Oil Market Analysis - 04052011Documento32 pagineSunflower Oil Market Analysis - 04052011Ștefan SanduNessuna valutazione finora

- UK Market for Dried FruitsDocumento15 pagineUK Market for Dried FruitsBashar Magzoub100% (1)

- General Price List March2016Documento176 pagineGeneral Price List March2016hacker12345Nessuna valutazione finora

- Indian Label Industry OverviewDocumento21 pagineIndian Label Industry Overviewlalit2585100% (1)

- Bangladesh Exporter GuidelinesDocumento27 pagineBangladesh Exporter GuidelinesBaki HakimNessuna valutazione finora

- UK Examining Boards Contacts ListDocumento20 pagineUK Examining Boards Contacts ListYAGHMOURE ABDALRAHMAN0% (1)

- Group Marketing OPC & Chemicals Marketing Plan 2016Documento3 pagineGroup Marketing OPC & Chemicals Marketing Plan 2016bandithaguruNessuna valutazione finora

- GCC Guide For Control On Imported Foods - Final PDFDocumento69 pagineGCC Guide For Control On Imported Foods - Final PDFValeria DumitrescuNessuna valutazione finora

- MSDS Avi DC MF PDFDocumento5 pagineMSDS Avi DC MF PDFWim Rizki AgusthaNessuna valutazione finora

- Iran SektorlerDocumento49 pagineIran Sektorlersales officeNessuna valutazione finora

- 12 ListofFirmsRepresentedbyMembers PDFDocumento98 pagine12 ListofFirmsRepresentedbyMembers PDFBGNessuna valutazione finora

- Welcome To Our PresentationDocumento26 pagineWelcome To Our PresentationSha D ManNessuna valutazione finora

- WTP Catalog WebDocumento76 pagineWTP Catalog Webkenri hendarsyahNessuna valutazione finora

- Approved List of Manufacturers: CategoryDocumento5 pagineApproved List of Manufacturers: CategoryBernard SolisNessuna valutazione finora

- Firms represented by membersDocumento98 pagineFirms represented by membersBGNessuna valutazione finora

- IRAN - Gas Imports - 20091204Documento5 pagineIRAN - Gas Imports - 20091204Muhammad SiddiuqiNessuna valutazione finora

- The 14th Dhaka International Trade FairDocumento5 pagineThe 14th Dhaka International Trade FairImroz MahmudNessuna valutazione finora

- TOPL FSRU Buyer Supply Items Final ListDocumento52 pagineTOPL FSRU Buyer Supply Items Final ListPiyush KumarNessuna valutazione finora

- Applications and Market Research of PtfeDocumento16 pagineApplications and Market Research of PtfeHarsh GuptaNessuna valutazione finora

- Morocco Companies: Name Headquarters IndustryDocumento2 pagineMorocco Companies: Name Headquarters IndustryFaraz SMFZNessuna valutazione finora

- Business Plan: Billiard ClubDocumento41 pagineBusiness Plan: Billiard ClubMichaelRMilani0% (1)

- Electrical Electronics VOL.08 PDFDocumento148 pagineElectrical Electronics VOL.08 PDFFlorian Leordeanu50% (2)

- CATALOGUE Coprosider SRLDocumento64 pagineCATALOGUE Coprosider SRLwlmNessuna valutazione finora

- Turkish Metal Industry Report HighlightsDocumento25 pagineTurkish Metal Industry Report HighlightsRoman SuprunNessuna valutazione finora

- Cif Palm Kernel ShellDocumento14 pagineCif Palm Kernel ShellPanwascam PurwoharjoNessuna valutazione finora

- Marwari CommunityDocumento12 pagineMarwari Communityrony patelNessuna valutazione finora

- List Company Registered Bunker Supplier 050712Documento7 pagineList Company Registered Bunker Supplier 050712James CapplemanNessuna valutazione finora

- Retail Industry Global Report 2010Documento36 pagineRetail Industry Global Report 2010Yam NoomNessuna valutazione finora

- Potential Exports and Nontariff Barriers to Trade: Maldives National StudyDa EverandPotential Exports and Nontariff Barriers to Trade: Maldives National StudyNessuna valutazione finora

- Exporting Jif Peanut Butter To ChileDocumento26 pagineExporting Jif Peanut Butter To ChileclaudiaNessuna valutazione finora

- Embedded CompaniesDocumento14 pagineEmbedded CompaniesCharles NachaatNessuna valutazione finora

- Exporting Cocoa Products to EuropeDocumento18 pagineExporting Cocoa Products to EuropeKRITHIKANessuna valutazione finora

- What Is The Demand For Cocoa On The European Market - CBIDocumento10 pagineWhat Is The Demand For Cocoa On The European Market - CBITaio RogersNessuna valutazione finora

- World Market Profile Confectionery ProductsDocumento23 pagineWorld Market Profile Confectionery ProductsDivya PrakashNessuna valutazione finora

- 1a - Total ProductionDocumento10 pagine1a - Total ProductionbambangijoNessuna valutazione finora

- Daily FFB 30092022Documento2 pagineDaily FFB 30092022daidi andriasNessuna valutazione finora

- A Review of Key Sustainability Issues in Malaysian Palm Oil IndustryDocumento13 pagineA Review of Key Sustainability Issues in Malaysian Palm Oil IndustrybambangijoNessuna valutazione finora

- Gula PasirDocumento5 pagineGula PasirbambangijoNessuna valutazione finora

- Faktor-Faktor Yang Mempengaruhi Produksi Produk Turunan Minyak Sawit Di IndonesiaDocumento150 pagineFaktor-Faktor Yang Mempengaruhi Produksi Produk Turunan Minyak Sawit Di IndonesiabambangijoNessuna valutazione finora

- Bussiness Opportunity On Palm Oil Industri PerbaikanDocumento4 pagineBussiness Opportunity On Palm Oil Industri PerbaikanbambangijoNessuna valutazione finora

- Faktor-Faktor Yang Mempengaruhi Produksi Produk Turunan Minyak Sawit Di IndonesiaDocumento150 pagineFaktor-Faktor Yang Mempengaruhi Produksi Produk Turunan Minyak Sawit Di IndonesiabambangijoNessuna valutazione finora

- Faktor-Faktor Yang Mempengaruhi Produksi Produk Turunan Minyak Sawit Di IndonesiaDocumento150 pagineFaktor-Faktor Yang Mempengaruhi Produksi Produk Turunan Minyak Sawit Di IndonesiabambangijoNessuna valutazione finora

- Peluang Bisnis Industri Kalapa Sawit Dan Produk Turunannya 2016 - 2020Documento9 paginePeluang Bisnis Industri Kalapa Sawit Dan Produk Turunannya 2016 - 2020bambangijoNessuna valutazione finora

- Faktor-Faktor Yang Mempengaruhi Produksi Produk Turunan Minyak Sawit Di IndonesiaDocumento20 pagineFaktor-Faktor Yang Mempengaruhi Produksi Produk Turunan Minyak Sawit Di IndonesiabambangijoNessuna valutazione finora

- Studi of Palm Oil Industri and Its Derivatives in Indonesia 2016 - 2020Documento12 pagineStudi of Palm Oil Industri and Its Derivatives in Indonesia 2016 - 2020bambangijoNessuna valutazione finora

- Elevation map of Sumberbendo regionDocumento1 paginaElevation map of Sumberbendo regionbambangijoNessuna valutazione finora

- Cocoa Market Update As of 3.20.2012Documento7 pagineCocoa Market Update As of 3.20.2012bambangijoNessuna valutazione finora

- Worldbank-Wld Sugar WLDDocumento12 pagineWorldbank-Wld Sugar WLDbambangijoNessuna valutazione finora

- Мировые цены на сахарDocumento1 paginaМировые цены на сахарOlya MikhoNessuna valutazione finora

- Table 03 BDocumento2 pagineTable 03 BbambangijoNessuna valutazione finora

- EC-4-2 Cocoa Market Situation - English-WDocumento14 pagineEC-4-2 Cocoa Market Situation - English-WPusha PMNessuna valutazione finora

- Say No and Yes CigareteDocumento1 paginaSay No and Yes CigaretebambangijoNessuna valutazione finora

- Say No and Yes PizzaDocumento1 paginaSay No and Yes PizzabambangijoNessuna valutazione finora

- Presentation Title: My Name My Position, Contact Information or Project DescriptionDocumento5 paginePresentation Title: My Name My Position, Contact Information or Project DescriptionbambangijoNessuna valutazione finora

- Karikatur Self Defence (Compatibility Mode)Documento1 paginaKarikatur Self Defence (Compatibility Mode)bambangijoNessuna valutazione finora

- Equipmnt KarateDocumento2 pagineEquipmnt KaratebambangijoNessuna valutazione finora

- Say No and Yes CigarDocumento1 paginaSay No and Yes CigarbambangijoNessuna valutazione finora

- Say No and Yes (Compatibility Mode)Documento1 paginaSay No and Yes (Compatibility Mode)bambangijoNessuna valutazione finora

- Worldbank-Wld Sugar WLDDocumento13 pagineWorldbank-Wld Sugar WLDbambangijoNessuna valutazione finora

- Worldbank WLD PlywoodDocumento12 pagineWorldbank WLD PlywoodbambangijoNessuna valutazione finora

- The Karate 2Documento2 pagineThe Karate 2bambangijoNessuna valutazione finora

- The Karate 2Documento2 pagineThe Karate 2bambangijoNessuna valutazione finora

- Saravanan India's Foreign TradeDocumento25 pagineSaravanan India's Foreign TradeSaravanan TkNessuna valutazione finora

- Module 1Documento8 pagineModule 1AdityaNessuna valutazione finora

- Elle Ourso Writing SamplesDocumento6 pagineElle Ourso Writing SampleselleoursoNessuna valutazione finora

- Import ExportDocumento16 pagineImport ExportYuvrajgreatNessuna valutazione finora

- Valid Arguments For Tariffs or Export SubsidiDocumento1 paginaValid Arguments For Tariffs or Export SubsidiTrang Chử ThuNessuna valutazione finora

- The Agricultural and Processed Food Products Export Development AuthorityDocumento14 pagineThe Agricultural and Processed Food Products Export Development AuthorityAnubhav JainNessuna valutazione finora

- Notification No. 95 of 2018 CUSTOMS N.T PDFDocumento176 pagineNotification No. 95 of 2018 CUSTOMS N.T PDFARJUNNessuna valutazione finora

- Q2 H1-FY20 Concall HighlightsDocumento188 pagineQ2 H1-FY20 Concall HighlightsRazesh BoradNessuna valutazione finora

- Development of Coal Mining and Its Impact On Industrial DevelopmentDocumento5 pagineDevelopment of Coal Mining and Its Impact On Industrial DevelopmentAnkitNessuna valutazione finora

- Draft ReportDocumento138 pagineDraft ReportDanudear Daniel100% (1)

- Print Version Vol 17 No 845Documento52 paginePrint Version Vol 17 No 845Henizion100% (1)

- Proiect ComertDocumento49 pagineProiect ComertAnonymous oQaW4Kx2Nessuna valutazione finora

- 5chestnutcover ENDocumento30 pagine5chestnutcover ENErmal IlirjaniNessuna valutazione finora

- Bcom Semv Export MKTGDocumento9 pagineBcom Semv Export MKTGChetan RajputNessuna valutazione finora

- Pestel of Aci PharmaDocumento6 paginePestel of Aci Pharmatahrimafaruq50% (2)

- Final Mondernization TheoryDocumento15 pagineFinal Mondernization TheoryAdrian De Goal Getter100% (1)

- India Foreign Trade Policy CourseDocumento1 paginaIndia Foreign Trade Policy CoursePrerna SidanaNessuna valutazione finora

- Business Plan ReportDocumento19 pagineBusiness Plan ReportHàMềmNessuna valutazione finora

- How Do Foreign Cosmetics Companies Align Their Supply Chains and Distribution Channels in ChinaDocumento30 pagineHow Do Foreign Cosmetics Companies Align Their Supply Chains and Distribution Channels in ChinaMinh Thuy VincyNessuna valutazione finora

- Technology Agreements in ChinaDocumento24 pagineTechnology Agreements in ChinaDeborah DuganNessuna valutazione finora

- Advantages of International TradeDocumento114 pagineAdvantages of International TradeMulezi Chanje100% (2)

- Chopper Regulator, DC DC Converter and Motor Drive ApplicationsDocumento6 pagineChopper Regulator, DC DC Converter and Motor Drive ApplicationsvasssNessuna valutazione finora

- CH1 IfmDocumento32 pagineCH1 IfmSaad RazaNessuna valutazione finora

- IIM-Auto Components 2Documento27 pagineIIM-Auto Components 2singhania1989nehaNessuna valutazione finora

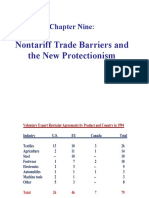

- Chapter Nine:: Nontariff Trade Barriers and The New ProtectionismDocumento26 pagineChapter Nine:: Nontariff Trade Barriers and The New ProtectionismAhmad RonyNessuna valutazione finora